Culled—Proshare

August 31, 2017/Vetiva Research

· Top and bottom line beat estimates, PAT doubles y/y

· Strong loan and deposit growth defies industry trend

· Board declares interim dividend of ₦0.60 per share

· TP revised upward to N28.39 (Previous: N25.74)

Top and bottom line beat estimates, higher significantly y/y

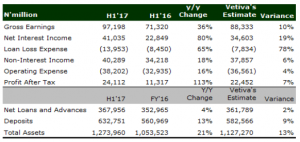

STANBIC released its H1’17 results, posting strong top and bottom line performances. Up 36% y/y, Gross Earnings came in at ₦97.2 billion – 10% better than our ₦88.3 billion estimate. Whilst Non-Interest income rose by a modest 18% y/y (flat q/q), Interest Income came in much stronger – up 55% y/y to ₦56.7 billion vs. our ₦50.5 billion estimate.

In line with general industry trend, we believe Interest Income must have been buoyed by the strong interest rate environment amidst modest 4% ytd growth in loan portfolio (coverage ytd average: -2%). However, Interest Expense came in just in line with our estimate at ₦15.7 billion, contained at a 13% y/y rise – defying the trend observed across other industry players (our coverage banks’ Interest Expense rose by 55% y/y in H1’17) and despite a strong 13% growth in customer deposit.

With this, the strong Q1’17 run rate was maintained as Net Interest Income rose 80% y/y to ₦41.0 billion (up 17% q/q) – 19% ahead of our ₦34.6 billion estimate. Asset quality was however the key pressure point for earnings as loan loss provision raced 65% y/y to ₦14.0 billion (ahead of our ₦7.8 billion estimate) – following a significant write off of ₦10.6 billion in Q2’17 standalone.

Consequently, whilst earnings maintained the strong y/y growth, performance was weaker q/q with Operating Income down 11% q/q despite rising 39% y/y and 4% above Vetiva estimate. Overall, despite a notable rise in Operating Expense, PAT rose to ₦24.1 billion (H1’16: ₦11.3 billion) – 7% ahead of our estimate.

TP revised to N28.39 (Previous: N25.74)

We revise our estimates to reflect the earnings outperformance. We raise our Interest Income estimate to ₦108 billion (Previous: ₦101 billion) given the elevated interest rate environment and strong loan growth expectation of 8% (previous: 5%). Notably, we expect the strong customer deposits growth to support credit growth.

However, in line with the trend observed in Q2’17, we raise our loan loss provision higher to ₦21.9 billion (previous: ₦15.7 billion) – translating to a Cost of Risk of 6.0%. Similarly, we raise our Operating Expense estimate to ₦76.7 billion (Previous: ₦73.1 billion). Despite raising our Target Price (TP) to ₦28.39 (Previous: ₦25.74), we maintain our SELL rating on the stock. STANBIC trades at FY’17 P/B: 2.3x and P/E: 8.8x vs. our coverage banks’ average P/B: 0.8x and P/E: 4.4x.