Culled—Proshare

September 6, 2019/by CardinalStone Research

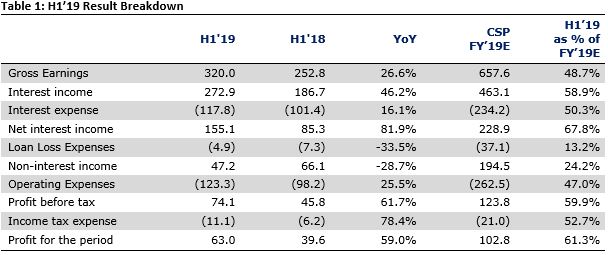

Access Bank Plc (ACCESS TP: N8.74 – BUY) has reported a 40.7% YoY increase in EPS to N1.90 in its audited H1’19 results. The company also proposed an interim dividend of N0.25 per share which translates to a dividend yield of 3.9% on current market price. Below are some of the highlights from the result:

Some positives:

Interest income grew 46.2% YoY, supported by a 138.2% YoY increase in interest income from investment securities. Interest income from loans and advances also advanced 14.9% YoY during the period

Net interest income rose 81.9% YoY as net interest margin improved to 7.4% from 6.2% in FY’18. This also reflects the impact of the integration of cheaper deposits on overall interest expenses as cost of funds declined to 4.8% in H1’19 from 5.5% in FY’18

Net fees and commission income improved 24.8% YoY, supported by a 119.2% increase in transaction and e-business related fees and commissions, as well as a 96.5% increase in account maintenance charges

Despite the 25.5% YoY increase in operating expenses, cost-to-income ratio improved to 61.0% from 64.9% in H1’18

Impairment charges declined 33.5% YoY during the review period, supported by credit writebacks which amounted to N4.9 billion (H1’18 writebacks: N450.0 million). Consequently, cost of risk improved to 0.3% in H1’19 from 0.7% in FY’18

Credit quality also improved during period as NPL ratio declined to 6.4% from 10.0% as at Q1’19. This reflects a 34.1% decline in absolute NPLs to N196.3 billion from N297.7 billion following the integration Diamond Bank’s assets. We believe that a majority of these loans were likely restructured given flattish gross loan growth post integration

Capital adequacy at 20.8% (reflecting full IFRS 9 impact), liquidity ratio at 49.7% and loan-to-deposit ratio at 65.6% (Bank only: 61.4%) are in line with the relevant regulatory guidelines.

Some concerns:

Notwithstanding the improvement in fee income, overall non-interest income weakened (28.7% YoY) owing to much lower gains on investment securities (H1’19: N4.1 billion; H1’18: N59.6 billion). Key drivers were derivative losses of N1.8 billion (vs H1’18 gain of N33.4 billion) and much lower gain of equity investments of N5.9 billion (vs H1’18 gain of N25.7 billion).