![]()

Culled—Proshare

October 28, 2019

By CardinalStone Research

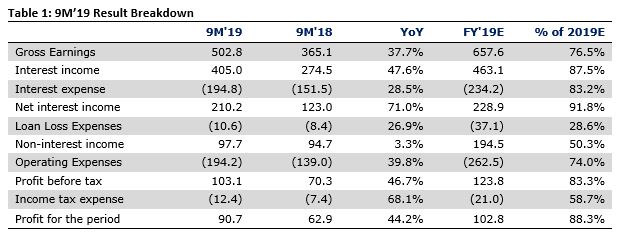

Access Bank Plc (ACCESS: TP 8.74 – BUY) reported a 28.0% YoY increase in EPS to N2.74 for 9M’19 in its latest filing with the Nigerian Stock Exchange (NSE). The growth in earnings was supported by a 71.0% YoY jump in net interest income.

**Earlier today, ACCESS disclosed to the Nigerian Stock exchange its proposed acquisition of controlling equity interest in Transnational Bank of Kenya (TNB) Plc**

Some Positives:

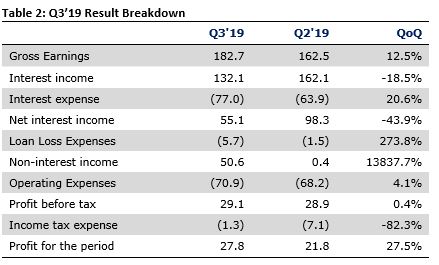

- Non-interest income came in strongly during the quarter at N50.6 billion compared to N363 million in Q2’19. The jump largely reflects strong FX gains (N24.1 billion in Q3’19 vs FX losses of N25.2 billion in Q2’19)

- Gross loans grew 3.8% during the quarter from the level as at Q2’19 to c. N3.0 trillion. We note that ACCESS was one of the few banks that met the CBN’s loan to funding requirement as at September 2019.

- Notwithstanding the 4.7% QoQ increase in operating costs, we note the improvement in efficiency as cost to income moderated by 200 bps during the quarter. Year-to-date, cost to income has declined by 80 bps to 63.1% despite the one-off integration costs incurred. We believe the moderation in cost to income ratio suggests that the bank is already reaping synergies from its merger with Diamond.

Some Concerns:

- Despite the combination of Diamond Bank’s huge retail deposits, cost of funds (at 5.2%) remains relatively high compared to an average of c.3.1% for the other Tier 1 banks. This may be due to the 15.0% growth in expensive term deposits from the post-combination level in Q1’19. While deposits have grown 8.1% since the business integration, over 79.0% have come from expensive deposits. In contrast, low cost deposits account for just 54.4% of total deposits, 2.7ppts lower than the post-combination level in Q1’19

- Likewise, net interest margin weakened to 6.8% during the period compared to 7.6% in H1’19. This possibly reflects the impact of funding cost pressure (9M’19: 5.2%; H1’19: 4.8%) previously highlighted

- Net impairment charges rose more than 3-fold to N5.7 billion during the quarter, though cost of risk moderated 20bps QoQ, supported by the 3.8% growth in gross loans