Culled—Proshare

October 30, 2019

By CardinalStone Research

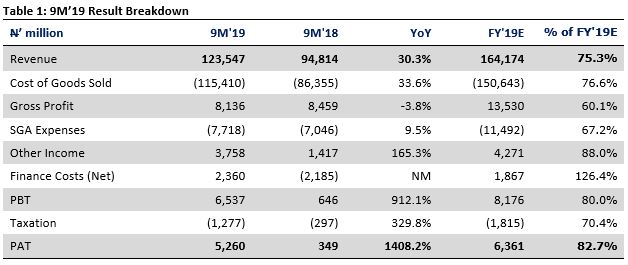

Forte Oil Plc (FO: TP N22.01 ) released its 9M’19 earnings result earlier today, announcing EPS of N4.03/share during the nine month period (FY’19E: N4.88/share). 9M’19 performance was bolstered by gains from disposal of assets and interest proceeds from longstanding PMS subsidy receivables. The company noted that proceeds from longstanding receivables was also supported by naira devaluation.

Some Positives:

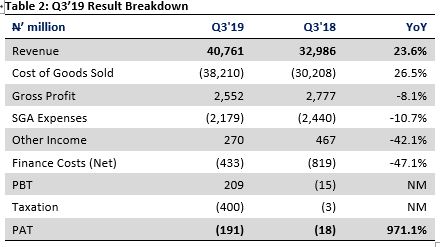

- Q3’19 turnover grew by 23.6% YoY, driven by revenue increases in fuels (+23.1% YoY) and lubricants (+29.0% YoY) segments. We attribute the sharp improvement in topline to FO’s increased retail footprint (+ 5.4% YTD increase in number of retail stations)

- Operational efficiency improved in Q3’19, evinced by the 10.7% decline in operating expenses. Contraction in personnel expenses (-23.5% YoY) as well as a significant dip in legal costs (-52.9% YoY) supported the performance on this front

- Net Interest expense also declined by 47.1% YoY in Q3’19, as drawdown on trade finance and overdrafts slowed during the period. In addition, the company paid off all its borrowings (loans and import finance facilities) bar a medium term loan which matures in 2021. Consequently, net debt contracted to N2.9 billion in 9M’19 from N6.0 billion in FY’18.

Some Concerns:

- Q3’19 gross margin declined by 2.2 ppts YoY to 6.26% in Q3’19, reflecting cost pressures in the fuels business ( cost of sales to sales ratio: 96.1% in Q3’19 vs 92.9% in Q3’18). In our view, this reflects the impact of the reported increase in PMS depot price to N117/litre from N113/litre in 2018

- Other income also declined by 42.1% YoY in Q3’19, as the firm recorded lower proceeds from freight and fuels storage service offerings. There was also no foreign exchange gain during the period (vs N92.5 million in Q3’18)