Culled—Proshare

Culled—Proshare

May 24, 2020

By CardinalStone Research

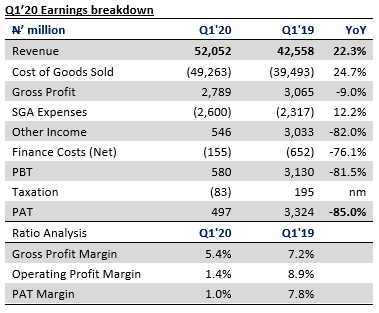

Ardova Plc (NGSE: ARDOVA) has announced an 85.0% YoY decline in EPS to N0.38/share in its unaudited Q1’20 results. The decline in earnings was magnified by a base effect driven by the huge one-off disposal gain of N2.7 billion recorded in Q1’19. On adjusting for the one-off gain, normalised EPS would be lower by 24.0% YoY.

Key Highlights:

- ARDOVA grew turnover by 22.3% YoY to N52.1 billion in Q1’20, mainly supported by a 24.6% increase in Fuel revenue to N47.8 billion and a marginal increase in lubricant sales. Revenue growth was driven by improved product supply and greater market penetration for white products. Notably, revenue rose across PMS (+34.0% YoY), ATK (+276.0% YoY), and Lubricants (+0.1% YoY) sub-segments in Q1’20

- Growth in PMS volumes reflected greater retail presence while the traction in ATK was driven by recent partnerships with international aviation lines

- The company reported a 1.8ppts contraction in gross margin to 5.4% in Q1’20 that was driven by cost pressures in the Fuels segment

- Interest expense declined by 76.1% YoY in Q1’20 due to past deleveraging efforts and overall moderation in yields in Nigeria. Total borrowings stood at N5.5 billion (vs. N19.8 billion in Q1’19) while normalised interest cover printed at 4.7x (vs. 1.7x in Q1’19) at the end of the review period

- Excluding the one-off disposal gain of N2.7 billion recorded in Q1’19, profit before tax would be 27.6% higher YoY at N580.3 million. Unadjusted pretax earnings is 81.5% lower YoY

- Net cash from operations increased to N6.4 billion in Q1’20, driven by improved liquidity management

- As part of its long term strategy, management restated plans to continue investing in non-fuel revenue initiatives while working with right-fit partners to achieve a 20% revenue contribution from renewables and higher-margin products by 2024