July 28, 2021/NBS

by FBNQuest Research

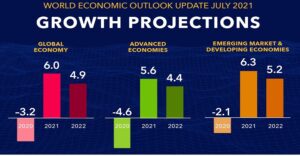

This week’s update to the World Economic Outlook from the IMF has higher expectations for next year than three months ago. Projected global growth for 2021 is unchanged at 6.0% but the forecast for 2022 has been raised from 4.4% to 4.9%. Confining ourselves of adjustments of +/- 50bps, we note increases for next year for India, the US, the Eurozone and Japan, and a decline for Brazil. For the US the adjustment is as much as 140bps, the result of the substantial fiscal stimulus both in place and proposed under the Biden administration. In aggregate, emerging market and developing economies (EMDEs) are seen as posting growth of 5.2% next year, compared with 4.4% for advanced economies. This update is entitled ‘Fault lines widen in the global recovery’ because of the uneven pace of vaccine rollout: the Fund estimates that almost 40% of the population has been fully vaccinated in advanced economies, less than half that level in EMs and a tiny fraction of the latter in low-income countries.

Within the debate around the current pick-up in inflation in advanced economies, the Fund’s central view is that it is likely to return to its pre-pandemic range in most countries in 2022. The spike has probably been the consequence of “unusual pandemic-related developments and transitory supply-demand mismatches”.

On a related matter, the update feels that major central banks will leave their policy rates unchanged through to end-2022.

As a mark of the improved global picture, close to an additional 80 million people are seen as falling into extreme poverty in 2020-21 compared with pre-pandemic projections. The figure was 95 million three months ago.

The update’s forecast for Nigerian growth this year is unchanged at 2.5%. It has been raised from 2.3% to 2.6% for 2022.

The update’s assumptions, based on the futures markets, for the Fund’s basket of three crude blends (including UK Brent) are now a rebound of 56.6% this year to USD64.7/b and a modest 2.6% decline in 2022 to USD63.1/b.

The narrative on the COVID-19 virus is that local transmission is expected to be at a low level globally by end-2022. A USD50bn IMF staff proposal, endorsed by the WHO, the WTO and the World Bank is designed to smooth this process. In this context, the update also highlights the Fund’s proposed general allocation of SDRs totalling the equivalent of USD650bn (Good Morning Nigeria, 08 July 2021).

| Trends in world output growth (% chg y/y) | ||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||

| Sources: IMF, World Economic Outlook update, Jul ’21; FBNQuest Capital Research |