October 28, 2021/Cordros Report

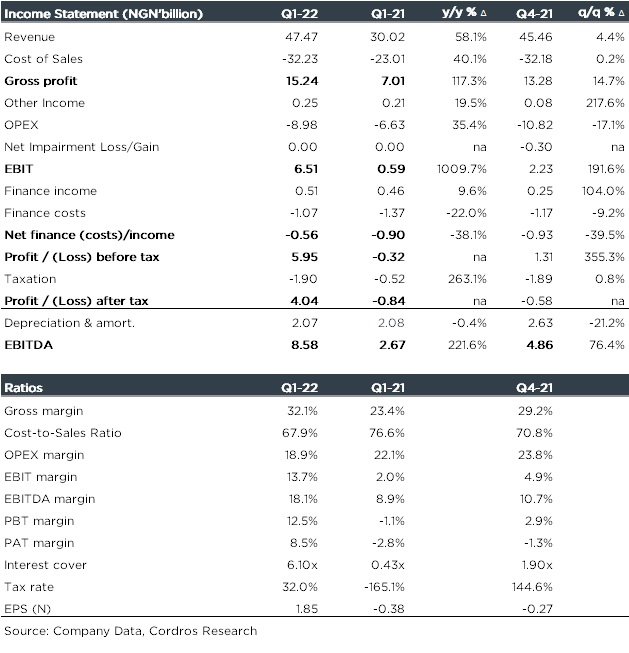

GUINNESS published its Q1-22 unaudited results after the close of market yesterday, reporting an EPS of NGN1.85 in Q1-22 vs Loss Per Share of NGN0.38 in Q1-21. The positive outturn in EPS was driven by the solid top-line growth (+58.1% y/y) amid the moderation in net finance cost (-38.1% y/y).

Revenue grew by 58.1% y/y in Q1-22 (Q1-21: 11.6% y/y) buoyed by resilient consumer demand and improved coverage of its trade outlets, as well as headline price increases in key brands. According to management, revenue grew across all key categories, driven by its strategic focus brands – Malta Guinness and Guinness – as well as double-digit growth in mainstream spirits (MSS), international premium spirits (IPS) and the ready-to-drink category (RTD’s).

Gross margin (+90bps) increased to 32.1% in Q1-22 (Q1-21: 23.4%) as revenue growth (+58.1%) outpaced the growth in cost of sales (+40.1% y/y). On the higher costs, management cited (1) the increase in sales volume, (2) a shift towards the production of more expensive can products and, (3) currency devaluation impacting the cost of imported raw materials as the drivers of the outturn.

EBIT and EBITDA margins came in higher at 13.7% (Q1-21: 2.0%) and 18.1% (Q1-21: 8.9%), respectively, reflective of the knock-on impact of the expansion in gross margin. We highlight that GUINNESS’s operating expenses were higher (+35.4% y/y) as a result of increased marketing (+49.6% y/y) and distribution (+35.6% y/y) expenses. Elsewhere, net finance costs declined by 38.1% following a 22.0% y/y decline in finance costs compared to a 9.6% y/y increase in finance income.

PBT was also higher at NGN5.95 billion compared to a pre-tax loss of NGN0.32 billion in Q1-21. Consequently, the company recorded a PAT of NGN4.04 billion (vs loss after tax of NGN0.84 billion).

Comment: We like that the company delivered a strong PAT in Q1-22, which is comparably better than the steeper loss recorded in Q1-21. This, in our view is reflective of cost minimisation efforts by the management and productivity gains evidenced in the strong top-line growth. Meanwhile, with further price increases expected in 2022FY to cover the higher costs pressures stemming from FX illiquidity challenges and inflation, we expect the top-line to maintain the growth momentum in Q2-22 and to further support earnings. On a YTD basis, GUINNESS share has rallied (+73.7%), in comparison to the Consumer Goods index (-1.7%) and the broader All-Share index (+4.2%). Our estimates are under review.