October 4, 2022/FBNQuest

The Debt Management Office’s (DMO) quarterly release on public debt, shows that the FGN’s total external debt obligations increased by c.USD96m relative to the prior quarter to USD40.1bn in Q2 ’22. This is roughly equivalent to 9.6% of 2021 GDP. On a y/y basis, the rise is more pronounced at c.USD6.6bn (+19.7% y/y).

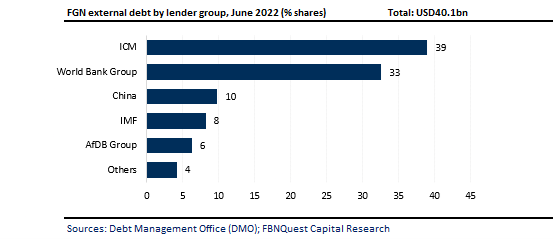

The debt stock also consists of state government external borrowings, totalling USD 4.6bn that are guaranteed by the FGN and owed to multilateral and bilateral lenders in a 93% to 7% split. The marginal rise in the FGN’s external borrowing q/q is explained by increases in the debt obligations to the World Bank Group and Exim Bank of China of USD340m and USD261m, respectively.

These increases were partially offset by the redemption of a USD300m Diaspora Bond which matured in June, a reduction of USD123m in IMF debt, and lesser reductions totalling USD82m in debt obligations to the AfDB and some bilateral lenders.

Since it raised USD1.25bn in seven-year Eurobonds on the international capital market (ICM) in March of this year, the FGN has been unable to re-enter the Eurobond market because of stringent credit conditions brought on by tightening monetary policy.

Consequently, the stock of debt owed to multilateral and bilateral lenders increased to 59.6% from 58.7% in the previous quarter.

The FGN’s preferred source of external borrowings are loans from concessional sources such as the World Bank and the AfDB, due to their lower financing cost relative to commercial debt. However, such funding sources are typically limited with respect to value and are often subject to conditions.

The 2022 budget projects a fiscal deficit of NGN7.4trn, which is to be partly financed by external borrowings of NGN2.6trn (c.USD6.2bn). However, external borrowings year-to-date have fallen short of the target at just USD1.6bn.

The Medium-Term Expenditure Framework (MTEF) for 2023-2025 forecasts external borrowings of between USD1.9bn to USD2.1bn in 2023. However, raising funds externally is anticipated to remain challenging in the short–to–medium term due to constraints to accessing funds on the ICM.