April 26, 2023/Coronation Research

Investors have begun to raise concerns about an approaching US debt ceiling deadline. Do we see an imminent default in the US? While we do not envisage a default, investors face increasing risks in financial markets as the deadline approaches. The uncertainty created by this situation could lead to a decrease in investor confidence and a sell-off of financial assets.

An Imminent Default in the US?

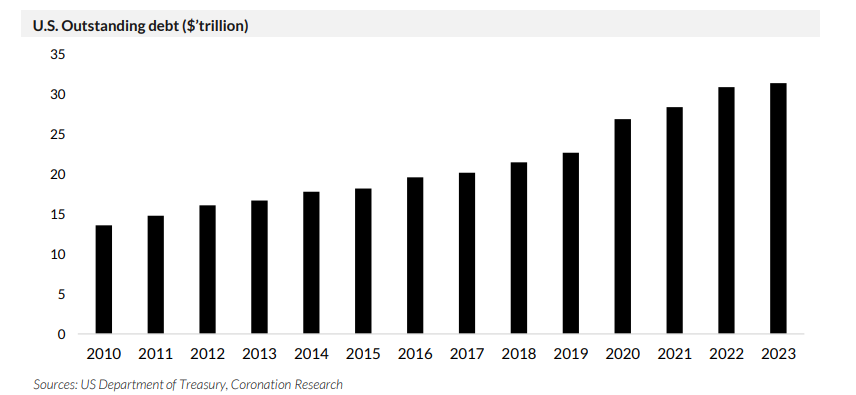

Since the Republican Party took over the House of Representatives in November 2022, the U.S. has been mired in a political impasse that threatens to cause a serious economic crisis. The debt ceiling, which is a legal cap on the sum of money the government can borrow, has been resisted due to disagreements on spending cuts and whether to reduce the national debt. The US government technically reached this ceiling in January 2023, but the US Treasury Department has utilised various means to ensure the government does not pass the ceiling. Some of these measures undertaken include suspending new investments in the Civil Service Retirement and Disability Fund and the Postal Service Retiree Health Benefits Fun. However, the country is running out of options and will default if both parties cannot reach an agreement by July. In fact, it is likely that the date will be earlier than this due to the possibility of weaker-than-expected tax receipts over the coming months.

Investors have begun to raise concerns about the approaching deadline. Do we see an imminent default in the US? While we do not envisage a default, we believe that investors face increasing risks in financial markets as the deadline approaches. The uncertainty created by this situation could lead to a decrease in investor confidence and sell-offs of financial assets. Additionally,this could pose a credit-rating downgrade which would further erode investor confidence.

The last times when we saw prolonged standoffs between the Republicans and Democrats in raising the ceiling were in 2011 and 2013. Credit agency Standard & Poor’s cut the United States’rating during the debt-ceiling crisis of 2011, which also saw a decline in global stock prices and bond prices for emerging-market nations as the government drew nearer to default. The S&P 500 lost 19.4% and 5.8% in 2011 and 2013, respectively.

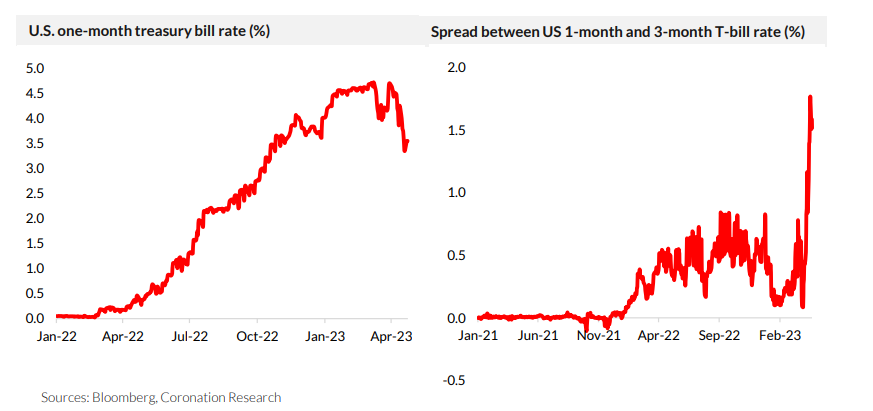

Already, some investors have started avoiding debts that mature within this timeframe. This has resulted in yields on onemonth US bills declining and the spread between the one-month and three-month bills expanding to its widest level since 2001 as investors look for safe places to put cash. Similarly, the spread on U.S. 5-year credit default swaps – market-based gauges of the risk of default – widened to 50bps in April, which is more than double what it was in January 2023.

Investors have learned from past occasions that the warring parties eventually reach agreement. However, the risk of an actual default cannot be ignored.

Once the debt ceiling is raised, the US Treasury is anticipated to increase its issue of bills. We expect investors to continue using the reverse repurchase agreement facility of the Federal Reserve until that time, which is seeing daily demand of about US$2.3 trillion

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) gained 0.07% to close at N463.67/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) reduced by 0.23% ($79.77m) to US$35.33bn, as the CBN continues to intervene across the various FX windows.

We think that the CBN is likely to continue with its policy of gradually loosening the I&E Window rate while managing FX reserves close to their historic highs. We expect only small FX rate adjustments over the coming weeks and months.

Bonds & T-bills

Last week, average yields in the secondary market for Federal Government of Nigeria (FGN) bonds closed 17bps higher at 13.85%. The yield on the 3-year bond advanced higher by 36bps to 12.39%, while the yield on the 7-years declined by 1bp to 14.35% and the 10-years declined by 5bps to 14.70%.

At the FGN bond auction, the Debt Management Office (DMO) offered N360.00bn across the February 2028 (bid-to-offer: 0.16x), April 2032 (bid-to-offer: 0.06x), April 2037 (bid-tooffer: 1.13x) and April 2049 (bid-to-offer: 3.59x) maturities with most of the demand skewing to the longer-dated bonds (20-year and 30-year bonds). Demand was lower than at the last auction in March, as reflected by a total subscription of N444.03bn (N808.61bn at the last auction) and a bid-to-offer ratio of 1.23x (vs 2.25x at the last auction). Reflecting the tight liquidity, the yields on the April 2032 (+5bps to 14.80%), April 2037 (+20bps to 15.40%) and April 2049 (+5bps to 15.80%) expanded while the yield on the February 2028 held steady at 14.00%. A total of N552.47bn was eventually allotted which included non-competitive allotments of N183.80bn.

The secondary market for T-bills closed on a bullish note, with the average T-bill yield moderating by 3bps to 8.79%. Yields declined by 1bp to 7.02% at the mid-end and lower by 4bps to 10.76% at the long end of the curve. At the T-bill primary auction holding this week, the CBN is scheduled to roll over NGN131.46 billion worth of maturities. Elsewhere, the yield on the 12-day OMO billremained unchanged at 4.01%.

We expect a liquidity surfeit over the week owing to the Apr-2023 bond maturity (N735.96bn) and FAAC disbursements (N438.49bn). Nonetheless, over the course of the year, we expect the overall direction of T-bill and FGN bonds to be upward as increases in government borrowing are felt by the market.

Oil

Last week, the price of Brent reversed gains after increasing for four consecutive weeks, declining by 6.04% to settle at US$81.10/bbl. Consequently, Brent is down 5.60% year-todate and is trading at an average of US$82.61/bbl year-to-date, 16.63% lower than the average of US$99.09/bbl in 2022.

Oil prices declined due to worrying economic data in the U.S. and the expectation of another interest rate hike. In addition, global supplies are showing signs of growth with Russia’s crude exports bouncing back above 3 million barrels per day last week We maintain that for the most part of the year, prices are likely to remain well above the US$75.00/bbl set in Nigeria’s government budget.

Equities

Last week, the NGX All-Share Index lost 1.04% to settle at 51,355.74 points. Its year-to-date return slipped to 0.20%. Zenith Bank (-12.20%), United Bank of Africa (-7.65%) and MTN Nigeria (-6.67%) closed negative while Fidelity Bank (+13.95%), Access Corporation (+11.86%) and PZ Cussons (+8.18%) closed positive.

Performances across the NGX sub-indices were broadly negative as declines in the NGX Banking (-2.54%), NGX Oil/Gas (-1.43%), NGX-30 (-0.58%) and NGX Industrial Goods (- 0.17%) sub-indices outweighed gains in the NGX Pension (+1.44%), NGX Insurance (+1.14%) and NGX Consumer Goods (+0.17%) sub-indices

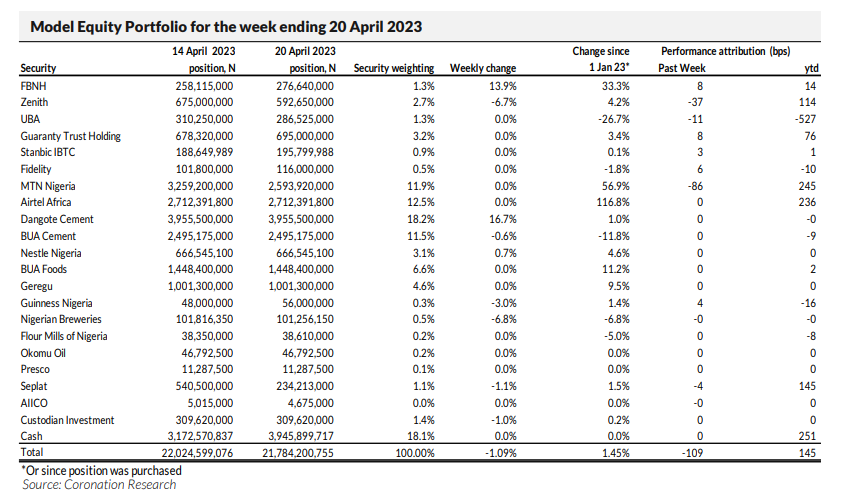

Model Equity Portfolio

Last week the Model Equity Portfolio lost 1.09% compared with a fall in the NGX All-Share Index of 1.04%, underperforming it by 5bps. Year-to-date it has risen by 1.45% compared with a rise of 0.20% in the NGX All-Share Index, outperforming it by 125bps.

We try to buy stocks which we like rather than trade the market as a whole but two weeks ago we decided to trade the market as a whole, forewarning that we would take the notional cash position up from 3.5% to 17.5% over a fortnight. We have slightly overshot our target, the notional cash position now standing at 18.1% (as we sell and the value of the portfolio reduces the cash percentage increases slightly unpredictably). We decided to make notional sales to bring down the equity position because we thought that the market would continue to correct in the face of high market interest rates. Our operation, with all notional commissions paid, won us 46bps of outperformance.

This is very tactical behaviour, of course, and it brings with it the following problem. As, a) the market reaches a zero return year-to-date, and b) short-term market interest rates are set to fall as liquidity enters the system (see page 1) then it becomes more likely that the market will rebound. We will therefore reverse our tactics and seek to bring the notional cash position back to 9.0% with notional purchases during the course of the week, starting with notional purchases in MTN Nigeria and our six bank names (with a view to bringing up the bank exposure to a neutral weight) and later moving on to make neutral our other key underweights.