July 4, 2023/FBNQuest

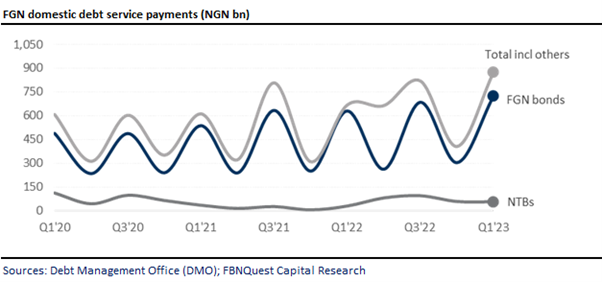

The Debt Management Office’s (DMO) latest quarterly release on public debt shows that the FGN’s domestic debt service increased by slightly over NGN205bn, or 31% y/y to NGN874bn as at the end of Q1 ’23. The figure represents the highest debt service payments for as far back as we can track. Consequently, the major driver behind the rising debt service burden is the 23% y/y increase in FGN’s domestic debt stock to NGN24.7trn as at Q1 ’23. Additionally, the escalating debt burden is compounded by the elevated cost of new debt issuance and higher effective yields on re-opened issues.

When annualised and adjusting for seasonality, the total debt service cost for Q1 ’23 implies an estimated interest rate of c.14.4% compared with around 12.4% for FY ‘22, and 12.2% (annualised) for Q1 ’22.

Interest payments on FGN bonds accounted for 83% of total debt service cost during the quarter, down from 94% in Q1 ‘22. Interest payments, however, grew 15% y/y to NGN724bn.

The increase is mostly explained by a 29% y/y rise in the value of FGN bonds in the overall debt portfolio to NGN18.4trn. As such, the share of FGN bonds increased to 74.5% from 70.7% in Q1 ’22.

A combination of factors including revenue underperformance, escalating expenditures, persistent fiscal deficits, and a tighter external credit environment has led to the FGN’s significant reliance on domestic debt to cover the fiscal shortfall.

Interest payments on Nigerian Treasury Bills (NTBs) which are the second most significant component of debt service surged by 91% y/y NGN56bn.

The debt service figures provided by the DMO exclude the interest on the FGN’s ways and means (W&M) financing. These are typically provided in the more comprehensive report from the finance ministry.

Looking ahead, the interest on W&M will now be included in the DMO’s debt publication for Q2 ’23, following the approval to securitise the W&M. As such, we expect a y/y increase in the debt service cost for Q2 ’23.

That said, once the W&M has been fully securitised, the FG’s overall debt service burden should be a bit lighter due to the lower interest rate on the W&M of 9% per annum compared with interest rate of MPR (18.5%) +3% previously.