July 4, 2023/Coronation Report

After the drought comes plenty, or at least that is how it looks for investors in Nigeria’s listed banks. Some of the many restrictions on commercial banking activity, which were enforced over the past four years, are being eased and the result is a surge in confidence in the sector.

A Relief Rally for Banks

Just over a month into a new presidential administration and things are looking up for Nigeria’s banks. First came the removal of fuel subsidies, which makes the Federal Government of Nigeria richer by some US$8.6bn per annum (based on 2022’s budget), and which in turn implies that the FGN will be less inclined than before to see banks as a source of financing via their customers’ deposits.

Second came last month’s liberalisation of the foreign exchange market. Recall that in March 2020, and in response to a range of macroeconomic challenges stemming from the onslaught of the Covid-19 pandemic which included very depressed oil prices, the CBN reduced the flow of US dollars which it had previously made available to the I&E Window and other official FX markets. The result was a fall in the US dollar of the Naira in the parallel market.

Lack of official FX liquidity hurt the banks while the officialrate and the parallel rate diverged. And it was announced recently that the CBN will introduce Naira-settled over-the-counter FX futures for tenors of 13 to 60 months, while there will also be Naira-settled Exchange-Traded Futures traded on FMDQ. The currency markets are waking up.

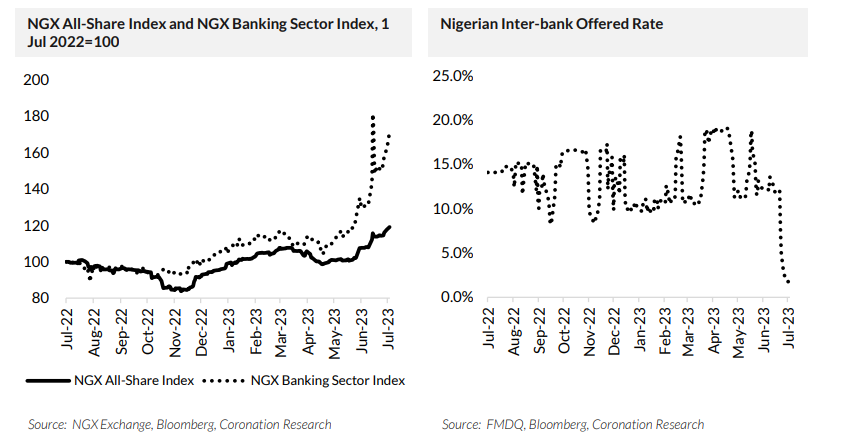

Third came a technical change to the Naira inter-bank market with potentially wide-reaching consequences. The rate at which overnight NIBOR could trade had been linked to the lower band set around the Monetary Policy Rate (MPR) at 18.5%, effectively putting an 11.5% floor to interbank rates. This was removed last week, with a resulting crash in interbank rates, an increase in bank liquidity and the enthusiastic response to Friday’s T-bill auction which we describe above.

Not surprisingly, investors in listed bank stocks are enjoying the change. For them it is case of plenty following a drought. The NGX Exchange sub-index of banks rose by just 2.8% in 2022 compared with a 19.9% return for the broad NGX All-Share Index. This year the sub-index of banks is outperforming, with a price return, year-to-date, of 65.1% compared with 20.9% for the NGX All-Share Index

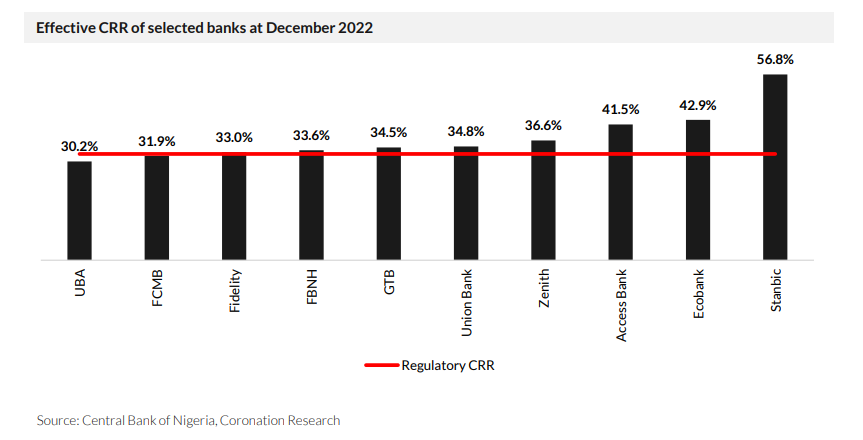

If one looks back over the accretion of bank regulations that have held banks in check over the past few years, the cash reserve requirement (CRR) would feature as the one which bank CEOs like the least. Some 32.5% (or more, in some instances) of their customers’ Naira deposits were held by the CBN to be on-lent to the FGN. We understand that there is talk of the CRR being reduced in some way. It is the early days (we are only a month into a new administration) but the portents for banks are good. As we argued in Coronation Research, Nigerian Banks: a Year of Resilience and Grit, 30 March, the valuations a few months ago were compelling. All that was needed was a catalyst.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) gained 0.12% w/w to close at N769.25/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) decreased by 0.34% to US$34.19bn.

We expect the foreign exchange market to reach a consensus over the Naira/US dollar in a matter of weeks.

Bonds & T-bills

In the secondary market for T-bills the market was slightly bullish last week with average yields declining by just 1bp. At the short end of the T-bill curve, the average yield fell by 1bp to 5.57%; at medium maturities by 1bp 5.48%; at long maturities by 18bps to 6.69%. By the end of the week the mood at the CBN’s T-bill auction was much more bullish. In Friday’s T-bill auction the CBN offered N187.1bn (US$243.1m) with a total subscription of N753.5bn. The average yields at auction fell by 159bps to 4.49% per annum.

The secondary market for bonds also was bullish last week with the average yield falling by 56bps to 12.98%. At the short end of the curve, yields fell by 107bps to 10.27%; at the medium part of the curve by 98bps to 13.17%; and at the long end by 42bps to 14.83%. There was no FGN bond auction last week.

It is clear that a change in the CBN’s rule on interbank lending, which we discussed above, is responsible for a rise in bank liquidity and declining T-bill and bond rates. In the short term we expect the effects of increased liquidity to continue to be felt, meanwhile we await the announcement of an overall strategy on market interest rates.

Oil

Last week, the price of Brent closed on a positive note, advancing higher by 1.42% to settle at US$74.90/bbl. Brent is down 12.82% year-to-date and is trading at an average of US$79.97/bbl year-to-date, 19.29% lower than the average of US$99.09/bbl in 2022.

Oil prices advanced following data which showed strengthening economic activity in the US. US Q1 2023 GDP figures were revised higher to 2.0% year-on-year (previously 1.1% year-on-year) indicating that the economy might be in a better shape than earlier thought. The US Federal Reserve’s preferred inflation gauge, core PCE inflation slowed to 3.8% year-on-year in May from 4.3% in the previous month, thus giving the Fed an added data point, which argues for holding back from raising rates again.

We maintain our view that for most of the year, prices are likely to remain above the US$75.00/bbl set in Nigeria’s government budget.

Equities

For the sixth consecutive week, the NGX All-Share Index closed higher, advancing by 2.98% to settle at 60,968.27 points. Its year-to-date return rose to 18.96%. Sterling Bank (+30.74%), PZ Cussons (+16.40%), and Guaranty Trust Holding Company (+11.29%) closed positive while Honeywell Flour Mills (-2.94%), First Bank of Nigeria Holdings (-1.45%) and Flour Mills of Nigeria (-1.16%) closed negative. Performances across the NGX sub-indices were positive as the NGX Banking (+7.78%), NGX Oil/Gas (+4.56%), NGX Pension (+4.47%), NGX-30 (+2.81%), NGX Insurance (+1.90%), NGX Consumer Goods (+1.12%) and NGX Industrial Goods (+0.63%) sub-indices all rose.

We remain optimistic about this market in view of the key fuel subsidy and foreign exchange reforms.

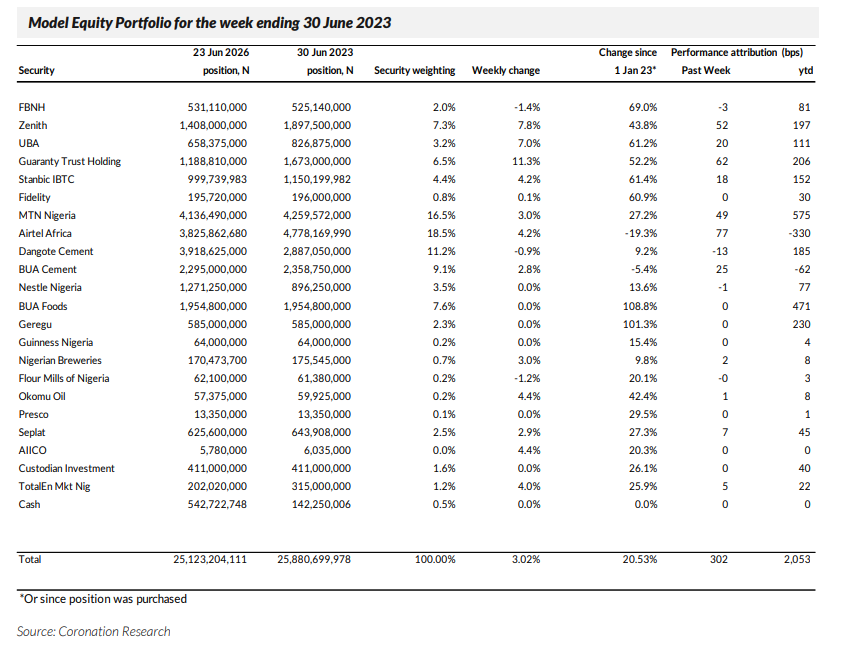

Model Equity Portfolio

Last week the Model Equity Portfolio rose by 3.02% compared with a gain in the NGX All-Share Index of 2.98%, outperforming it by 4bps. Year-to-date it has risen by 20.53% compared with a rise of 18.96% in the NGX All-Share Index, outperforming it by 157bps.

Given our commitment to overcoming the banks we are disappointed by our narrow outperformance last week. We could point to the remarkable spurt from Sterling Bank, in which we do not have a notional position, and which gained 30.74% over the week’s three trading days, but Sterling Bank accounts for just 0.29% of the NGX All-Share Index, so this omission did not count for much (9 basis points of lost performance, to be precise).

The real problem is that having stated in these pages on 13 June that we would increase our overweight position in banks (we first mooted being overweight banks at the end of May), we were then slow to build up the notional position. Our performance attribution model tells us that our sluggishness cost us an eye-watering 30bps of performance. Even now, with an aggregate 24.2% position in banks compared with a neutral position that would be 15.5%, we are not benefiting enough from our call. The lesson is, when you have a strong idea, to put on the trade (in our case the notional trade) as swiftly as possible.

Three things are required this week. First, we need to measure the neutral weights of the five main stocks in the NGX AllShare Index, which change daily (the top-five stock are MTN Nigeria, Airtel Africa, Dangote Cement, BUA Cement, and BUA Foods which together account for 63.2% of the index) and align the Model Equity Portfolio carefully. Big moves in these stocks could wreck hard-won outperformance. Second, we need to top up our overall banks’ position, again, for which we will need some notional cash. Third, and noticing that we have a notional overweight in Nestle Nigeria, we intend to trim this, releasing notional cash, and bring this position down to a neutral weight.