July 10, 2023/Cardinalstone

H1’23 witnessed numerous twists critical to the banking sector outlook. These twists included the abolition of FX market segmentation, the entrenchment of a 2-way quote system premised on the willing buyer-seller mode and plans to normalise the use of the CRR as a monetary policy tool. The FX-linked reforms resulted in a devaluation of the naira to N769.25/$ in June 2023 from its 2022 closing rate of N461.50/$, essentially reducing the parallel market premium.

In our view, these reforms have opened up a seismic shift in the Nigerian banking sector outlook, with banks reassessing their operational capabilities to capture opportunities whilst repealing existential threats. In this report, we examine the intricacies of the banking sector as it relates to the impact of a free-float FX system vis-à-vis banks’ balance sheet exposures, asset portfolio & associated loss provisioning, statutory requirements via capital adequacy & NPL ratios, and the return of orthodox monetary policies.

Revaluation Gains to Underscore Potential EPS Growth

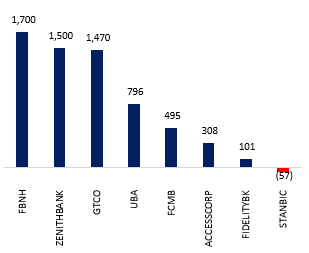

Our assessment of assets and liabilities revealed that coverage banks are more likely to report revaluation gains than losses in FY’23 due to the huge naira devaluation stoked by the FX policy changes. Specifically, given the net open position suggested by its last full-year financials, FBNH is positioned to register the highest revaluation gain among its tier-1 peers, followed by ZENITHBANK and GTCO. For our Tier-2 lenders, FCMB holds the premier position on the net-open USD-denominated exposure front, with FIDELITY closely trailing. Notably, STANBIC has a net short dollar position as at FY’22. However, conversations with management reveal that the bank is likely to report a net-long open position in H1’23.

Bank’s USD Net-Open Position ($’millions) as at FY’22