July 25, 2023/Coronation Research

With the NGX All-Share Index up 26.8% year-to-date, and key reforms on fuel subsidy and foreign exchange enacted, will the foreign portfolio investor stage a return? Our view is that, following many disappointments in the equity market and a significant rearrangement of US and Nigerian market interest rates over the past two years, it is unlikely that foreign portfolio investors will come back in a meaningful way, at least not for the rest of this year.

Will Foreign Portfolio Investors Return?

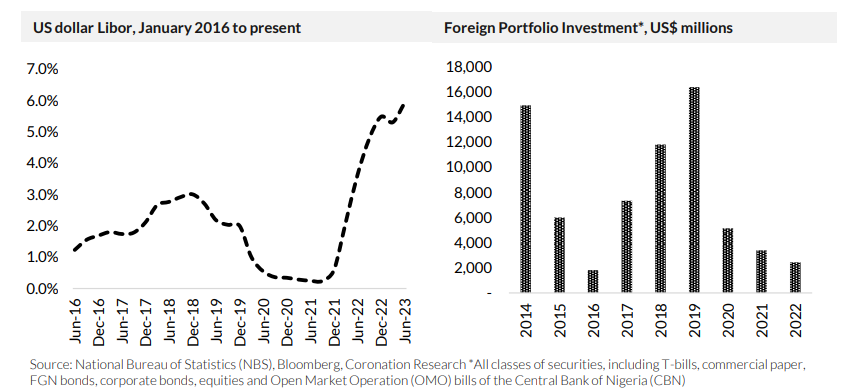

Foreign portfolio investment in Nigeria declined steeply after 2019 as risk-free yields on Nigerian Treasury Bills declined. That happened as the Covid-19 pandemic was about to sweep around the world, disrupting economies and depressing oil prices which, in turn, caused the Central Bank of Nigeria (CBN) to lessen its hitherto generous supplies of US dollars to the foreign exchange markets (from April 2020 onwards), causing the parallel market exchange rate to break away significantly from the official Naira/US dollar rate. These were dark days for foreign investors, especially those attempting to repatriate dividends, coupons or principal investments.

In 2018 and 2019 foreign portfolio investment (FPI) was at truly enormous levels, over 10 times the level of foreign direct investment (FDI). The bulk of this money was not in the equity market but in the Open Market Operation (OMO) bills of the CBN and in Treasury Bills. There were, therefore, two problems. None of these securities had a duration of more than one year, so the money would have to be paid back quickly. And the foreign investors would head to the foreign exchange market to get back their US dollars. It could only ever be a short-term measure of maintaining foreign capital in the country (unless the securities could be rolled over endlessly).

The second problem was that the fixed income trade depended on there being cheap US dollars which international funds could borrow (the US dollar Libor chart above gives an indication of these rates) and high-yielding Nigerian T-bill to invest in, at around 20.0% pa or more. Now that US dollar Libor is close to 6.0% and a 342-day Naira T-bill yields 6.27%, this trade no longer works

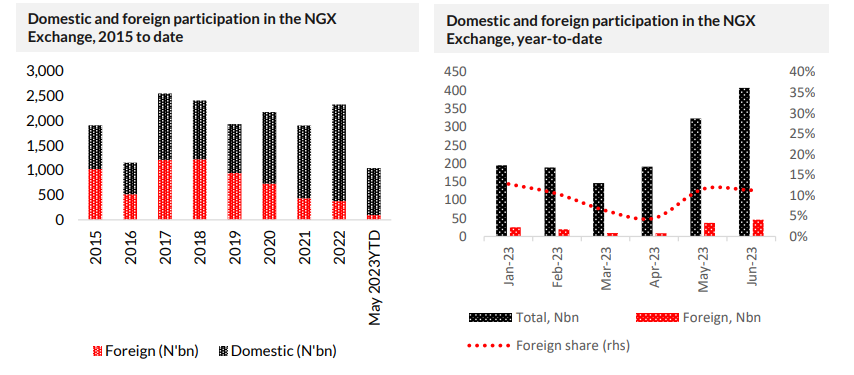

What about equities? Foreign participation in the Nigerian equity markets used to run at high levels, sometimes accounting for 50% of turnover (see 2015). But that was long ago. Successive years of negative equity market performance (2014, 2015 & 2016, followed by 2018 & 2019) were discouraging, to say the least. Problems with repatriation of dividends and principal, notably in 2016 and again in 2020, were also off-putting. Even through the NGX Exchange All-Share Index recorded three straight years of positive returns in 2020, 2021 & 2022, the share of foreign investors in trading fell during this period.

This is not to say that the foreign investor is absent from the equity market. Foreign participation jumped by 84% from January to June this year, but relative to overall turnover it only kept pace. Year-to-date it has accounted for some 10% of the market.

Following many changes in the foreign exchange and interest rate environments and following many disappointments in the equity market (and despite the last three years’ performance), we doubt that the foreign portfolio investors will return in force, and we do not expect this to change between now and the end of the year

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) lost 0.66% to close at N777.82/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) declined by 0.19% to US$33.97bn. The foreign exchange market has yet to reach a consensus on the Naira/US dollar rate, with one newspaper reporting that over the weekend US dollars were sold as high as N876/US$ in the parallel market, with other traders quoting N820/US$1 last week. Whereas we earlier expressed optimism that equilibrium would be found soon, it seems that this outcome may be several weeks away

Bonds & T-bills

The secondary market for T-bills was very bullish last week with average yields retracting by 192bps to 4.34% pa. Average yields along the T-bill curve fell sharply; at the short end (329bps to 2.39% ); mid-end (218bps to 3.29%); and long end (148bps to 5.17%). The secondary market for FGN bonds was also bullish last week, the average yield declining by 8bps to 12.73%. While average yields slipped at the short end (-4bps to 10.29%) and long end (-5bps to 14.24%) of the curve, the yield at the mid-part (+6bps to 13.05%) of the curve increased. Liquidity conditions in the market are clearly strong now that the CBN has lifted several restrictive liquidity measures earlier imposed on banks. While the effects of these changes are evident, we keenly await the conclusion of the meeting of the Monetary Policy Council tomorrow. We continue to wait for the new administration to announce an overall strategy on interest rates

Oil

Last week, the price of Brent closed on a positive note, advancing by 1.50% to settle at US$81.07/bbl. Brent is down 5.63% year-to-date and is trading at an average of US$79.83/bbl year-to-date, 19.43% lower than the average of US$99.09/bbl in 2022. For most of last week, the mood in the oil market was optimistic. Oil prices increased following China’s announcement that it will take action to stimulate economic growth. This optimism was combined with predictions of a fall in U.S. output as well as possible supply disruptions from Russia. We maintain our view that for most of the year, prices are likely to remain above the US$75.00/bbl mark set in Nigeria’s government budget.

Equities

Last week, the NGX All-Share Index closed higher, increasing by 3.89% to settle at 65,003.39 points. Its year-to-date return rose to 26.83%. Sterling Bank (+27.33%), Ecobank Transnational Incorporated (+27.17%), and FBN Holdings (+25.63%) closed positive while Guinness Nigeria (-8.75%) was the only major stock that closed in the red. Performances across the NGX sub-indices were positive as the NGX Consumer Goods (+17.99%) index topped the list, followed by NGX Banking (+15.81%), NGX Insurance (+5.65%), NGX Pension (+4.75%), NGX-30 (+3.94%,) NGX Industrial Goods (+2.80%) and NGX Oil and Gas (+0.64%) indices which all closed positive. We remain optimistic about this market following the key fuel subsidy and foreign exchange reforms.

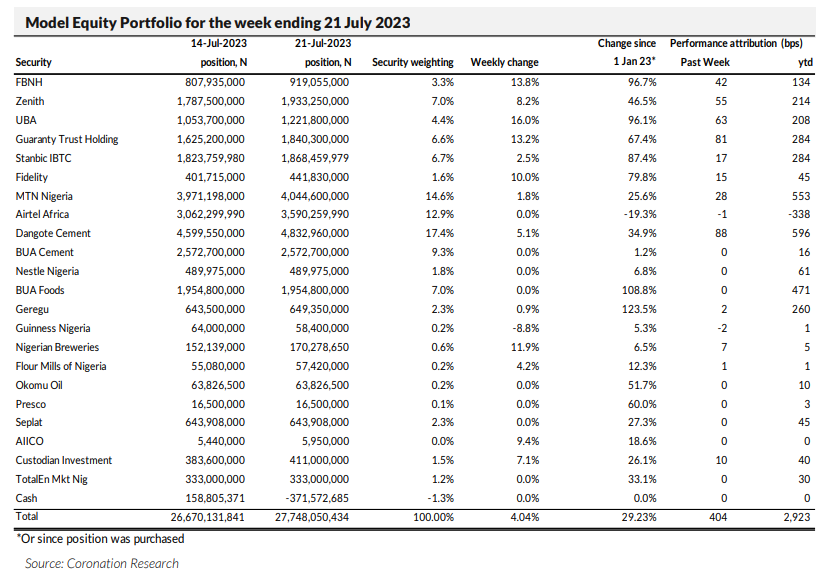

Model Equity Portfolio

Last week the Model Equity Portfolio rose by 4.04% compared with a rise in the NGX All-Share Index of 3.89%, outperforming it by 15bps. Year-to-date it has risen by 29.23% compared with a rise of 26.83% in the NGX All-Share Index, outperforming it by 240bps.

Our performance last week was due to our double overweight position (29.6% of the portfolio) in bank stocks relative to the index. Our combined notional position in six banks stocks delivered 272bps which, when combined with the 88bps earned from our neutral position in Dangote Cement, ensured outperformance. That said, our combined position in the banks rose by 9.6% when the banking sub-index rose by 15.8%. As noted last week, the banks in which we have notional positions are high-quality names (Zenith Bank, Guaranty Trust Holding Company, UBA, Stanbic IBTC, FBNH) and these shares tend to be less volatile than those of some of the smaller banks (such as FCMB Group and Sterling Bank). We have banks stocks with low volatility inside a highly volatile sector. As we set out in Coronation Research, Investment Opportunities from FX Liberalisation, 10 July, banks are clear beneficiaries from foreign currency liberalisation and we think they will continue to outperform for some time.

As explained last week, our intention is to have neutral notional positions in the top five stocks by index weight (Dangote Cement, MTN Nigeria, Airtel Africa, BUA Cement and BUA Foods) and last week we made notional purchases in Airtel Africa to bring this one up to a neutral position. We were partially successful but need to make some further notional purchases to complete this (we respect actually market liquidity even though this is a notional portfolio). We will also make small adjustments, where necessary, in these top-five stocks to maintain neutral positions in them. We plan no other changes this week.