July 28, 2023/Cordros Report

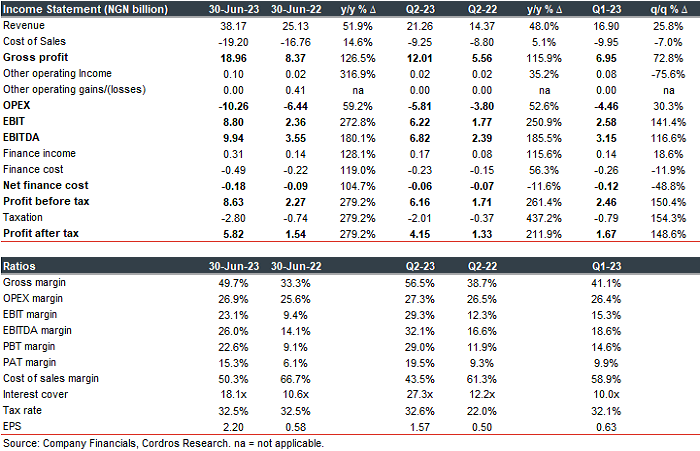

NASCON Allied Industries Plc (NASCON) published its unaudited Q2-23 financials this afternoon, reporting a standalone EPS of NGN1.57 (Q2-22: NGN0.50), bringing H1-23 EPS to NGN2.20 (H1-22: NGN0.58). The EPS increase was driven by the sturdy growth in sales (48.0% y/y) recorded in the reporting period.

Revenue for the period grew by 48.0% y/y (H1-23: 51.9% y/y), driven by price increases instituted across NASCON’s salt products and higher volumes, particularly in the Northern region. Across its business regions, revenue from the North (71.9% of revenue) continued to be the largest contributor to total sales outturn, growing by 55.4% y/y. In the same vein, revenue from the Western (+20.5% y/y | 21.5% of revenue) and Eastern (+91.4% y/y | 6.6% of revenue) regions maintained the momentum witnessed in Q1-23.

Quarterly analysis of the number highlights the stellar performance achieved in Q2-23, as revenue grew by 25.8%, following a broad-based increase across all regions – North (+26.0% q/q), West (+21.8% q/q) and East (+38.5% q/q).

Gross margin increased by 17.76 ppts to 56.5%, as the revenue growth for the period outpaced the cost of sales (+5.5% y/y). Aside from the relatively stable commodity prices and FX rate in Q1-23, we believe the higher inventory from 2022 limited the need to procure raw materials, thus shielding the company from cost pressures. On an HY basis, gross margin (+16.37 ppts) increased to 49.7%.

Consequently, EBITDA (+15.44 ppts) and EBIT (+16.92 ppts) margins increased to 32.1% and 29.3%, respectively, amid a 52.6% y/y growth in operating expenses.

Further down, net finance costs declined by 11.6% y/y, underpinned by a faster growth in finance income (+115.6% y/y) relative to finance costs (+56.3% y/y).

Overall, profit before tax grew sharply by 261.4% y/y to NGN6.16 billion (Q2-22: NGN1.71 billion). Following a tax expense of NGN2.01 billion, profit after tax printed NGN4.15 billion (Q2-22: NGN1.33 billion), translating to a growth of 211.9% y/y.

Management will hold a call on Monday (31 July) to discuss the results and the proposed merger with Dangote Sugar Refinery Plc and Dangote Rice Limited. Click here to join.

Comment: NASCON continues to outperform our expectations, as revenue growth maintained an accelerating pace amid the company’s efficient cost management. We believe that the resilience NASCON exhibited in 2022FY will be sustained in 2023E and support the company’s performance therein. However, we believe heightened cost pressures stemming from the highly inflationary environment and FX devaluation may be more evident in NASCON’s operations in the second half of the year. Our estimates are under review.