August 15, 2023/Coronation Research

Last week was a stormy one for Nigeria’s financial markets, with extreme weakness in the parallel exchange rate of the Naira, the publication of the CBN’s audited accounts for the first time in several years (accompanied by reports of collateralised lending against the nation’s reserves), a correction in FGN Eurobonds and the reintroduction of the Open Market Operation (OMO) auction by the CBN. Is it all bad news? Good mariners reset their bearings during storms, and we sense that things are changing for the better.

Savings Rates Moving Up?

For several weeks we have been describing how we await definitive guidance on the direction of Naira market interest rates, notably Treasury bill rates. The reforms of the new administration of President Bola Ahmed Tinubu earlier gave us clear guidance on fuel subsidy removal (which made us bullish on FGN Eurobonds) and FX liberalisation (which made us bullish on bank stocks) but until last week we knew little about its approach to market interest rates.

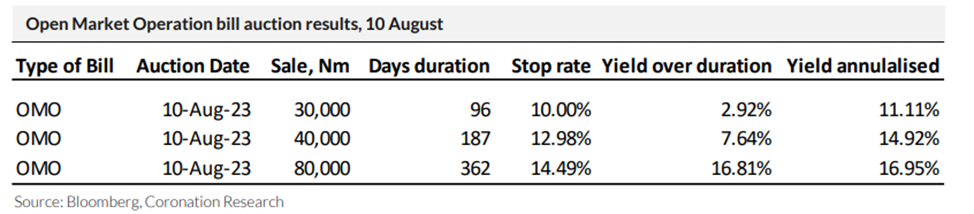

Now we know more. Last week CBN held an auction of Open Market Operation (OMO) bills, its first this year. Granted, the auction was not large (a total of N150.0bn) and the target market did not include institutions like pension funds (which have been excluded from OMO auctions since late 2019), but the rates were radically different from T-bill rates. The 362-day paper achieved an annualised yield close of 16.95%, far above equivalent T-bill yields. T-bill yields themselves began to move upwards at the end of the week, albeit slightly. If the auction had been larger and achieved the same rates, T-billrates undoubtedly would have risen more in the secondary market.

Is this truly a sign of things to come? Naira market interest rates are one of the last pieces in the jigsaw of government economic and monetary policy to fall into place. The fact that the Naira has been extremely weak in the foreign exchange market provides an argument for raising rates. Last week the International Monetary Fund published a paper which was featured by the Bloomberg news service with the headline ‘Nigeria’s economic policies too loose to support Naira, IMF says’. The IMF does not often make its criticisms public.

Clearly, there are those who would prefer low interest rates and in particular low interest rates on loans to industry: but it seems that the argument is moving in favour of creating interest rates high enough to encourage savers to hold Naira and high enough to tackle inflation in a meaningful way. Again, we will watch this space closely. Now we are much more optimistic for savers than we were previously.

Federal Government of Nigeria Eurobonds

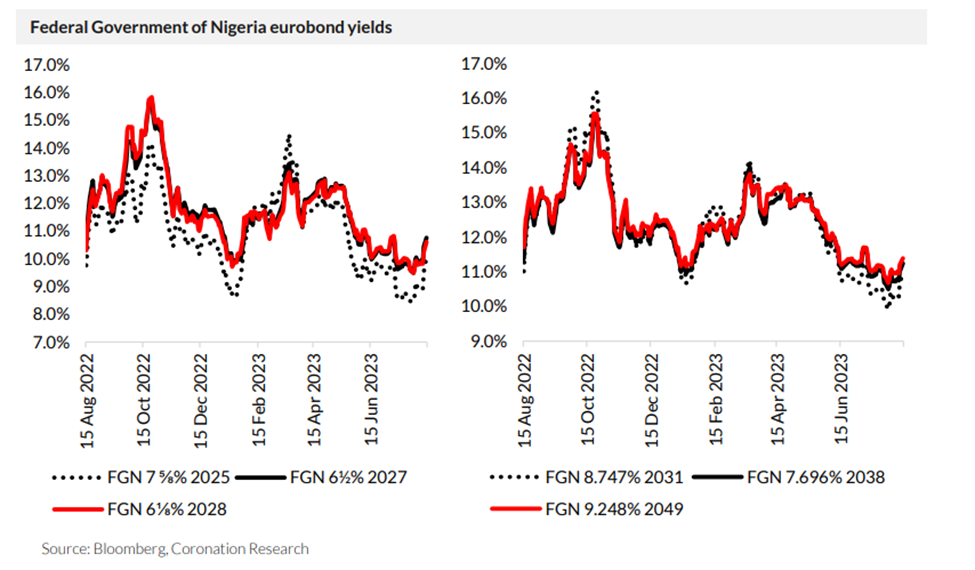

Last week Bloomberg carried another influential report, relating to the publication, on 9 August, of the CBN’s audited annual accounts on its website, for the first time in several years. The theme of the story was that the CBN had taken loans from investment bank JP Morgan for US$7.0bn, using its portfolio of US dollar-denominated securities as collateral. The report disclosed another loan, of US$0.5bn, from Goldman Sachs. The market reacted negatively, with a sell-off in FGN eurobonds towards the end of the week, yields moving up.

This market correction needs a little context. Nigeria’s sovereign eurobonds had been rallying for some time, in particular since the announcement of the removal of fuel subsidies at the end of May (see Coronation Research, Investment Opportunities from Fuel Subsidy Removal, 9 June). So, profit-taking was not wholly surprising. The net foreign exchange reserves of the CBN are, as is the case with most central banks, below the published gross level of reserves (which we feature on page 1 every week). It is still not exactly clear to us what the net figure is, but clearly most market participants have their own notions and estimates. And, quite recently, the rating agency Standard & Poor’s upgraded the outlook for Nigeria’s credit rating from negative to stable (B-/B long and short-term foreign and local currency). Once again, it is a situation we will watch closely.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) gained 0.33% to close at N740.60/US$1. In the parallel (or street) market, the Naira weakened by 6.81% to close at N955.00/US$1. Currently, the gap between the I&E Window and the parallel market stands at 22.00%. Elsewhere, the gross foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) slipped by 0.13% to US$33.88bn. There is some debate as to the net position.

Buyers are increasingly turning to the parallel market as banks struggle to supply demand, hence increasing the difference between the official and the parallel prices. In the medium term we maintain that the reforms in the foreign currency market will lead to improvements

Bonds & T-bills

Last week, the secondary market for T-bills was bearish with average yields increasing by 37bps to 7.33% pa. Average yields along the T-bill curve increased: at the short end (60bps to 4.69%); mid-end (45bps to 6.35%); and long end (36bps to 8.76%). In the T-bill auction which took place mid-week, the CBN offered N114.04bn (US$153.99m) with a total subscription of N836.29bn. The bid to offer ratio was 5.43x compared with 1.51x for the auction held at the end of July. The average yield at auction fell by 182bps to 6.90per annum.

The secondary market for FGN bonds moved in the same direction as the secondary market for T-bills. The average yield increased by 21bps to 13.52%. Average yields along the FGN bond yield curve rose at the short end (31bps to 11.54%); mid-end (15bps to 13.60%); and long end (19bps to 14.92%).

After a long wait for a steer on where market interest rates are going, we have evidence that they are going up, in particular the results of the OMO auction.

Oil

Last week, the price of Brent closed on a positive note, advancing by 0.66% to settle at US$86.81/bbl. Brent is down by 1.05% year-to-date and is trading at an average of US$80.33/bbl year-to-date, 18.94% lower than the average of US$99.09/bbl in 2022.

While major producers Saudi Arabia and Russia extended output caps, Iran has increased the rate at which it is pumping exports and even surpassed the government’s expectation of 1.4 million oil barrels per day.

We maintain our view that, for most of the year, prices are likely to remain above the US$75.00/bbl mark set in Nigeria’s government budget.

Equities

Last week, the NGX All-Share Index closed higher, increasing by 0.20% to settle at 65,325.37 points. Its year-to-date return rose to 27.46%. Guinness Nigeria (+10.00%), Honeywell Flour Mills (+6.92%), and Oando (+6.18%) closed positive while Dangote Sugar (-12.00%), PZ Cussons (-5.56%), and Fidelity Bank (-4.40%) closed negative. Performances across the NGX sub-indices were mostly positive as the NGX Banking (+1.26%) topped the list, followed by, NGX Insurance (+0.73%) and NGX 30 (+0.27%) indices closing green. On the other hand, the NGX Consumer Goods (-0.92%) index, NGX Industrial Goods (-0.39%), and NGX Oil/Gas (- 0.32%) indices closed in the red.

Model Equity Portfolio

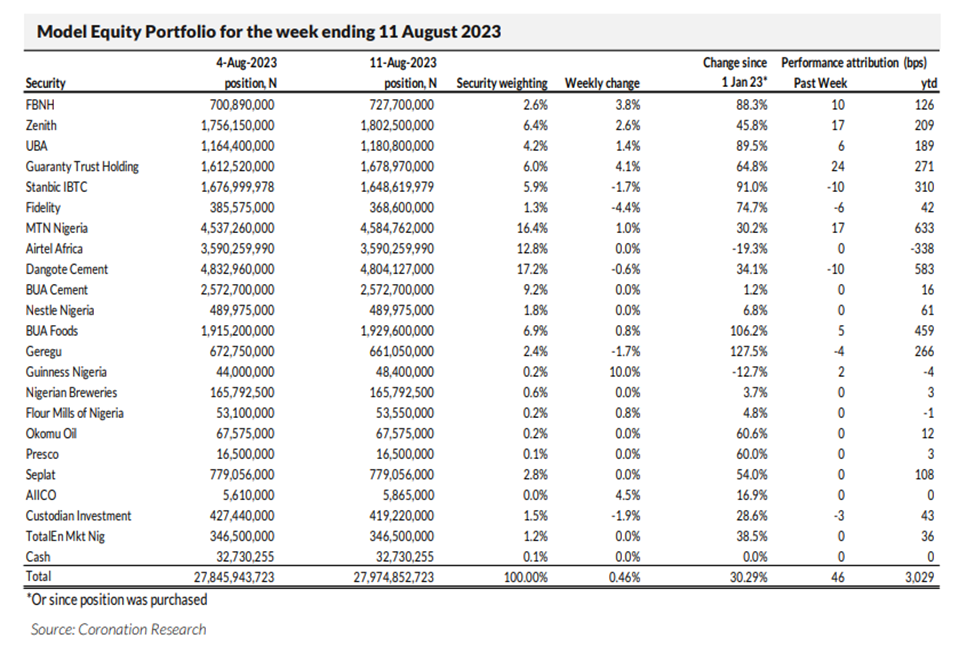

Last week the Model Equity Portfolio rose by 0.46% compared with a rise in the NGX All-Share Index of 0.20%, outperforming it by 26bps. Year-to-date it has risen by 30.29% compared with a rise of 27.46% in the NGX All-Share Index, outperforming it by 283bps.

Last week we were again grateful for our double overweight position in the banks. The NGX Banking Index rose by 1.26% last week, and the Model Equity Portfolio’s combined position in banks rose by 1.52%, contributing 40bps to our overall performance.

Last week we wrote: “We are becoming concerned with the lack of an overall policy direction with regard to market interest rates.” We are much less concerned about this problem now (see page 2) and this gives us a degree of confidence in the market. However, we still have some concerns.

We also wrote, last week: “We understand that the relaxation in the cash reserve requirement (CRR) is, to a degree, linked to banks fulfilling their obligations under the loan-to-deposit ratio (LDR) requirement. We may need to assess again how free the banks are to act in their own best interests.”

In other words, currency liberablisation is a good thing for banks (see Coronation Research, Investment Opportunities from Currency Liberalisation, 11 July), but we are not sure that banks will escape from the raft of operating restrictions imposed on them from mid-2019 onwards. In short, we are reconsidering our double overweight position in the banks. We do not doubt that they are set to report great Q3 results, come October, and great full-year 2023 results (not least because of revaluation gains on their US dollar loans). But a lot of this upside has been priced in. Over the past eight weeks the NGX Banking Index has risen by 15.1%; 30.4% since the beginning of June; 55.6% since the beginning of May; 63.6% year-to-date. This compares with its 73.3% gain in 2017, the last transformative year when the dual-exchange rate problem was brought to heel.

Therefore, we question how much more upside potential there is in the banks sector, at least in the short term. Over the coming weeks we intend to make notional sales in our bank positions with a view to bringing our overall banks position to below a neutral weight relative to the index