August 21, 2023/FBNQuest Research

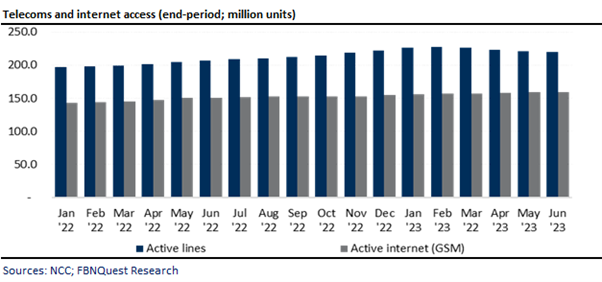

Our chart below, drawn from data provided by the Nigerian Communications Commission (NCC) on mobile subscribers, shows that the number of active mobile lines declined marginally by -0.5% m/m, (or -1.2 million lines) to 220 million in Jun ’23. The decrease marks the fourth consecutive monthly decline and brings the cumulative loss in active lines to c.7.1 million since Feb ’23. Active internet connections also decreased by 0.1 million lines to 159.5 million. As a result, the country’s teledensity dropped to 110.0% in Jun ‘23 from 110.6% in May ‘23, while internet penetration fell slightly to 79.7% from 79.8% over the same period.. .

The reduction in the number of active mobile lines is due to the directive issued by the NCC to network providers to deactivate lines that have remained idle for a duration of six months.

According to NCC’s data, almost all the major GSM network operators registered net subscribers losses in Jun ’23.

The exception was Globacom (Glo) whose active subscriber base expanded by c.180,000 to 61.3m, taking its share of mobile subscribers to 27.9% in Jun ’23 from 27.7% the previous month.

MTN Nigeria (MTNN) suffered the largest subscriber attrition, with a net subscriber loss of c.926,000 to 84.7 million. Consequently, its market share decreased to 38.5% in Jun ‘23 from 38.7% in May ’23.

Airtel Nigeria, and 9Mobile registered net subscriber losses of 337,000 and 82,000 to 60.2 million and 13.6 million, respectively.

Despite losing market share, MTNN continues to retain the largest share of active mobile subscribers, and its sector leadership based on other metrics is even more pronounced.

A 2022 report by the NCC puts MTNN’s share of total incoming and outgoing voice traffic at 63% and 59% respectively. This compares with 28% and 26% for Airtel Nigeria.

Additionally, out of the NGN3.3trn revenue generated by GSM operators in 2022, MTNN accounted for approximately NGN2.0trn, representing c.60% of total.

Despite the moderation in active subscribers, we anticipate robust sector revenue growth, primarily propelled by double-digit expansion in data and other business segments like digital and fintech.