September 13, 2023/Cordros Report

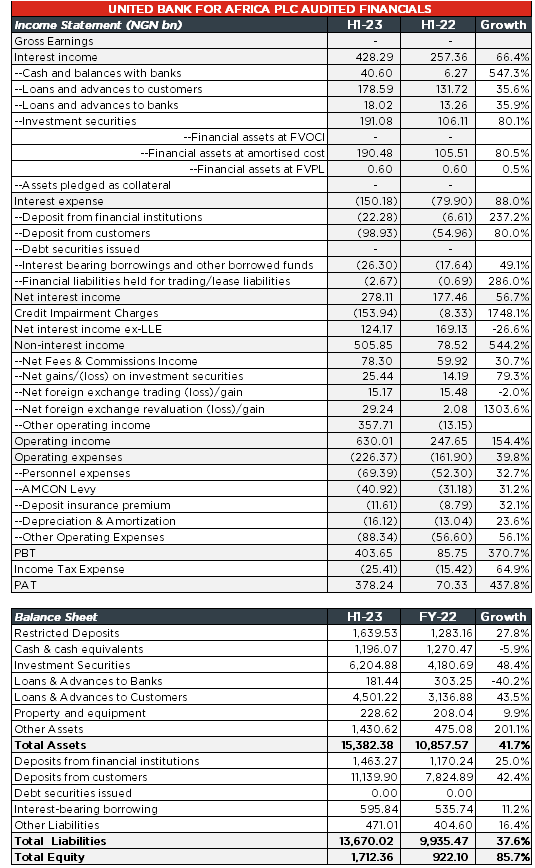

United Bank for Africa Plc (UBA) released its H1-23 audited financials after trading yesterday, showing a significant growth in EPS (+453.0% y/y) to NGN10.95/s (H1-22: NGN1.98/s). This impressive financial performance was supported majorly by the sturdy growth in the group’s non-funded (+544.2% y/y) income. The board proposed an interim dividend of NGN0.50/share (vs. NGN0.20/share in the corresponding period last year), representing a dividend yield of 3.6% based on the last closing price of NGN0.50 (12 September).

UBA recorded a 66.4% y/y increase in funded income to NGN428.29 billion driven by the elevated yield in the fixed income market and increase in key earning assets. Thus, income from investment securities grew by 80.1% y/y to NGN191.08 billion while income from loans and advances improved by 35.6% y/y to NGN178.59 billion. Elsewhere, the group recorded higher income from cash and balances with banks (+547.3% y/y to NGN40.60 billion) and loans and advances to banks (+35.9% y/y to NGN18.02 billion).

Interest expenses grew by 88.0% y/y to NGN150.18 billion following the increase in costs across the group’s funding base – deposits from banks (+237.2% y/y to NGN22.28 billion) and customers (+80.0% y/y to NGN98.93 billion), and borrowing (+49.1% y/y to NGN26.30 billion) – reflecting the higher interest rate environment. In addition, we also cite the rise in its deposits (+42.4% YTD to NGN11.14 trillion) amid the deteriorating CASA mix in the period (83.6% vs 2022FY: 85.1%) as another cost pressure point. After taking account of the credit impairment charges (+1748.1% y/y), the group recorded a decline in net interest income ex-LLE (-26.6% y/y) to NGN124.17 billion.

The group’s non-interest income grew markedly by 544.2% y/y to NGN505.85 billion, driven by the higher income generated from (1) FX revaluation gains (+1303.6ppts to NGN29.24 billion) induced by the naira devaluation, (2) net fees and commission (+30.7% y/y to NGN78.30 billion), and (3) investment securities trading (+79.3% y/y to NGN25.44 billion). In addition, the group recorded a substantial gain in its other operating income (NGN357.71 billion vs loss of NGN13.15 billion in H1-22) triggered primarily by the NGN348.43 billion net fair value gain generated on the group’s derivatives holdings relative to the NGN22.61 billion loss recorded in H1-22.

Operating expenses increased by 39.8% y/y in H1-23 following the higher costs incurred on personnel expenses (+32.7% to NGN69.39 billion), AMCON levy (+31.2% y/y to NGN40.92 billion), NDIC premium (+32.1% y/y to NG11.61 billion), and depreciation and amortization (+23.6% to NGN16.12 billion). Notwithstanding, UBA’s operational efficiency improved – cost-to-income ratio (H1-23: 35.9% | H1-22: 65.4%) – as the group’s operating income (+154.4% y/y) grew faster than OPEX.

To sum up, the group recorded a triple-digit growth in profitability as profit before tax grew by 370.7% y/y to NGN403.65 billion. Likewise, PAT grew faster by 437.8% y/y to NGN378.24 billion amid a higher income tax expense (+64.9% y/y).

Comment: The group’s H1-23 result mirrored the earnings growth across its tier 1 peers, supported primarily by the FX liberalisation implemented during the period. We envisage this strong earnings growth to remain by year-end, driven by the combined impact of the elevated interest rates and naira devaluation in the period. Our estimates are under review.