July 29, 2024/CSL Research

In 2024, the interplay between supply constraints, demand recovery, and broader economic and geopolitical trends continues to shape the global oil landscape. Notably, the ongoing conflict in Eastern Europe has disrupted supply chains, pushing prices higher. However, this upward pressure has been tempered by a slower-than-expected economic recovery in China, the world’s largest oil importer, which has dampened demand forecasts.

The Organization of the Petroleum Exporting Countries (OPEC), the alliance of major oil producers, has attempted to stabilize prices through production cuts. While these measures have offered some support, their effectiveness has been limited by increased production from other sources, particularly the United States.

The ongoing global shift towards renewable energy sources and stricter environmental regulations have also played a role. While this transition is expected to reduce long-term demand for fossil fuels, in the short term, it has led to investments in more sustainable energy infrastructure, influencing market expectations and prices.

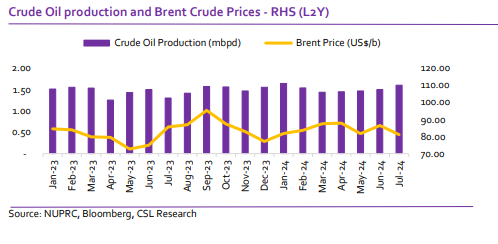

Price of Brent crude has averaged US$83.51/bbl year to date, which exceed Nigeria’s budgeted benchmark of US$77.96 per barrel, and has positioned the country to potentially benefit from increased government revenue through taxes, royalties, and dividends from the oil sector. However, Nigeria’s ability to fully capitalize on these higher prices is limited by production shortfalls.

This situation is significantly affecting foreign exchange earnings, and overall economic stability. To address these challenges, a comprehensive approach is required. This includes substantial investments in infrastructure to improve operational efficiency and increase output. Additionally, implementing robust security measures is crucial to curb oil theft and pipeline vandalism, which have been significant obstacles to maximizing production.

Click here to read full PDF copy of report