July 30, 2024/Oilprice.com

Oil prices continued to fall on Tuesday morning, ignoring the rising geopolitical risk in the Middle East and the potential supply disruption in Venezuela. Concerns about global demand continue to drive bearish sentiment in oil markets.

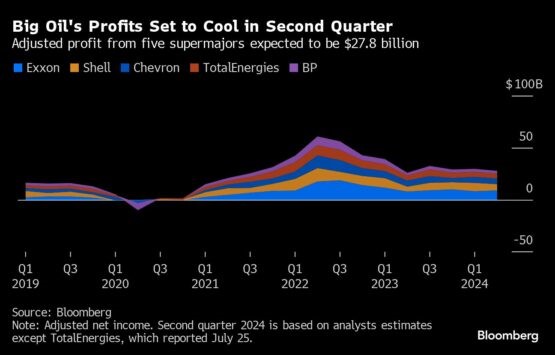

The Q2 quarterly earnings season has continued this week, with most of the oil majors reporting their performance results. TotalEnergies and BP provide no clear direction for where oil firms are headed.

– Total’s net income underperformed market expectations of $4.95 billion and came in at $4.7 billion, with the French major dragged down by a 36% year-on-year decrease in refining and chemicals revenue.

– BP, for a long time the least mouth-watering of the oil giants, posted a $2.8 billion Q2 net profit and beat analyst expectations by some 200 million, despite a hefty $1.5 billion impairment from shutting parts of the Gelsenkirchen refinery in Germany next year.

– The weaker downstream performance will also be the main drag for US majors. Chevron and ExxonMobil will both publish their results this Friday (August 2), and oil majors collectively are expected to see a 6-7% drop in net profits quarter-over-quarter.

Market Movers

– US shale producers Vital Energy (NYSE: VTLE) and Northern Oil and Gas (NYSE: NOG) agreed to jointly purchase the Permian assets of PE-owned Point Energy Partners for $1.1 billion, with Vital taking 80% and Northern buying the remaining 20%.

Chinese refining giant Sinochem (SHA: 600500) is reportedly in talks with Brazilian independent producer Prio to sell a minority stake in the giant Peregrino offshore field. In 2011, Sinochem paid $3 billion for a 40% stake.

– Italy’s oil major ENI (BIT: ENI) signed a temporary exclusivity agreement with global investment firm KKR to sell a 20% to 25% stake in its biofuel and mobility unit Enilive for up to $13.5 billion.

Tuesday, July 30, 2024

For the first time since the post-OPEC+ meeting selloff, ICE Brent futures dipped below $80 per barrel, driven lower by disappointing global demand as Chinese imports in July are set to hit the lowest level in two years. Considering the geopolitical risk upside, the decline might be somewhat overdone, with Israel-Lebanon flaring up over the weekend and Venezuela’s highly contested election lifting the risk of operations in the Latin American nation.

With No Mandate for Change, OPEC+ Meets Again. OPEC+ oil ministers will hold an online joint ministerial monitoring committee meeting (JMMC) on August 1 to review the effects of decisions taken two months ago, but the market expects no changes, only internal discussions.

Labour Government Hikes UK Windfall Tax. This week, the new Labour government confirmed that it would raise the windfall profit tax rate by 3% to 38% and increase overall taxation to a punitive 78% whilst extending the measure (called Energy Profits Levy) by another year to 31 March 2030.

Uranium Prices Soar to 16-Year Highs. Long-term uranium prices have hit 16-year highs, trading as high as $79 per pound lately. Demand for radioactive fuel is soaring due to new power generation buildouts expected to double global consumption by 2050.

King Coal Defies Calls for Global Decline. The International Energy Agency believes that global coal consumption will remain stable in 2024, rising marginally to 8.74 billion tonnes, postponing its forecast for peak coal to 2025 when it sees a slight downslide, citing declining Chinese appetite for coal.