September 11, 2024/NBS

In the second quarter of 2024, the National Bureau of Statistics reported that the federation’s account received almost N2.5 trillion in company income tax (CIT) receipts. This represented a significant increase compared to the N984bn and N1.5trn collected in Q1 2024 and Q2 2023, respectively. For the first half of 2024, the total CIT receipts amounted to nearly N3.5trn, indicating a 71% year-on-year (Y-o-Y) increase. These CIT receipts are mainly allocated to the federal government.

- Foreign CIT payments accounted for most of the collections during the second quarter. It accounted for N1.1trn or slightly over 45% of total CIT revenue.

- Domestic CIT collections increased by 32% y/y to N1.3trn, or almost 55% of gross receipts. On a q/q basis, collections rose by 249%, highlighting the seasonal corporate income tax collection patterns.

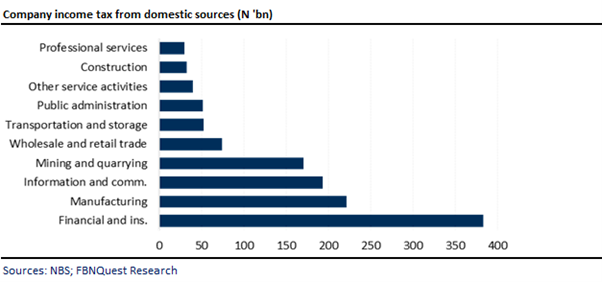

- The financial and insurance sector accounted for the largest share of domestic CIT revenues, contributing N384bn, representing 28% of domestic CIT receipts and 16% of total CIT.

- The manufacturing sector was the second largest contributor to CIT revenue, generating around N222bn in revenue and accounting for 16% and 9% of domestic and gross CIT receipts, respectively.

- Information and communications ranked third, with total collections of N194bn, representing 14% of domestic CIT receipts and 8% of overall CIT revenue.

- The rise in CIT collections can be attributed to improved tax compliance resulting from the Federal Government’s intensified efforts to boost tax generation and expand the tax base.

- Regardless, Nigeria’s tax revenue remains considerably low. As of 2023, the tax revenue-to-GDP ratio stood at approximately 2.1%.

- According to World Bank (2022) data, this figure significantly trails behind peer nations such as South Africa (26%), Kenya (13%), and Ghana (12%).

- Looking ahead, we anticipate that the proposals put forth by the Presidential Committee on Tax Reforms, if approved, will enhance tax collections and improve the tax-to-GDP ratio through measures such as streamlining tax processes and broadening the tax base.