January 23, 2025/CardinalStone Research

Following extensive engagements, the Nigerian Communications Commission (NCC) has approved a maximum tariff increase of 50.0% for Mobile Network Operators (MNOs), effective January 20, 2025. This marks the first tariff adjustment since 2013 and is deemed essential by the NCC to support infrastructure investments, drive innovation, and improve service quality, network reliability, and coverage for consumers

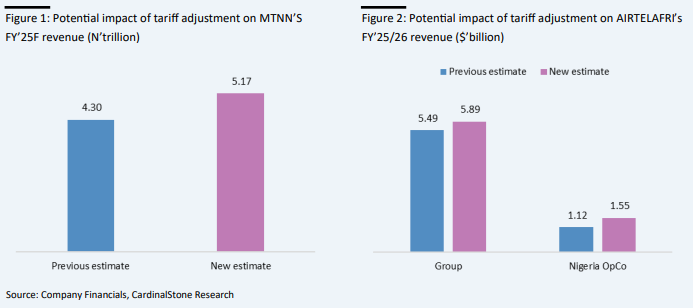

The new tariffs present a significant revenue growth opportunity for telecom operators, prompting a reevaluation of our coverage companies. MTNN stands to benefit the most, with the tariff increase expected to drive a 59.0% rise in revenue for 2025, stabilising at a medium-term compound annual growth rate (CAGR) of 26.6%.

For AIRTELAFRI, we anticipate an immediate revenue boost in the final quarter of FY 2024/2025, given its March financial year-end. By FY’25/26, the Nigerian OpCo gains and continued growth in other operating regions are projected to lift the group’s revenue by 17.0%, reaching US$5.89bn.

Some argue that higher tariffs could dampen customer demand, especially given Nigeria’s strain on consumer wallets. While this concern is valid, we believe the impact will be minimal. Data continues to drive growth in the sector, and Nigeria’s youthful, digitally inclined population (with 70% aged 15–18) is a key factor. The rise of content creation, social media management, e-commerce, and remote work has solidified data usage as a necessity, positioning it for further growth.

Additionally, we expect telecom operators to ramp up capital expenditure, reversing earlier expectations of a slowdown. With stronger revenue growth, investments in acquiring additional spectrums and upgrading telecom infrastructure are likely. These moves will improve service quality, accelerate the rollout of 5G sites, attract new customers and boost retention, strengthening the competitive edge over other internet service providers (ISPs).

Margin Recovery and Expansion

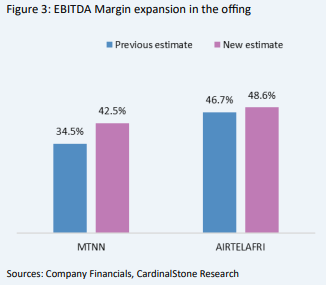

In line with our earlier views for MTNN and AIRTELAFRI, we anticipate a significant improvement in operational performances, driven by each company’s strategic initiatives to mitigate FX exposures and control rising operational costs. The impact of the new tariff increase is expected to serve as a complementary factor, bolstering margin improvements in the near term.

Specifically, MTNN’s EBITDA margin is expected to reach 42.5% in FY’25F (vs prior estimate of 34.5%). This shift also highlights the support from the ongoing benefits of the tower lease contract renegotiation. Meanwhile, for AIRTELAFRI, we expect the FY’25/26 EBITDA margin to print at 48.6% (vs prior estimate of 46.7%).

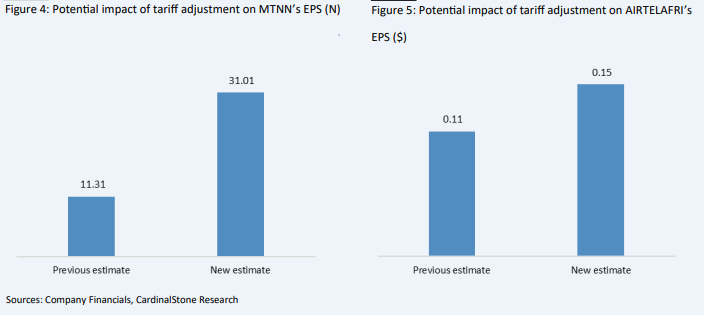

Looking further into the profitability metrics, the EPS readings for both counters showcased the positive impact of expected revenue improvements on the top-to-bottom. For context, FY’25F EPS for MTNN now prints at N31.01 (vs prior estimate of N11.31), while AIRTELAFRI’s EPS for FY25/25F is estimated at $0.15 compared to the initial forecast of $0.11.

Valuation

Given the improved revenue and EBITDA expectations driven by tariff adjustments, we anticipate a significant positive impact on valuation. After incorporating the tariff increase into our model, we have revised our 12-month target prices to N301.49 per share for MTNN and N3,209.08 per share for AIRTELAFRI. Overall, we retain our BUY recommendation on the counters.