October 29, 2025/Cordros Report

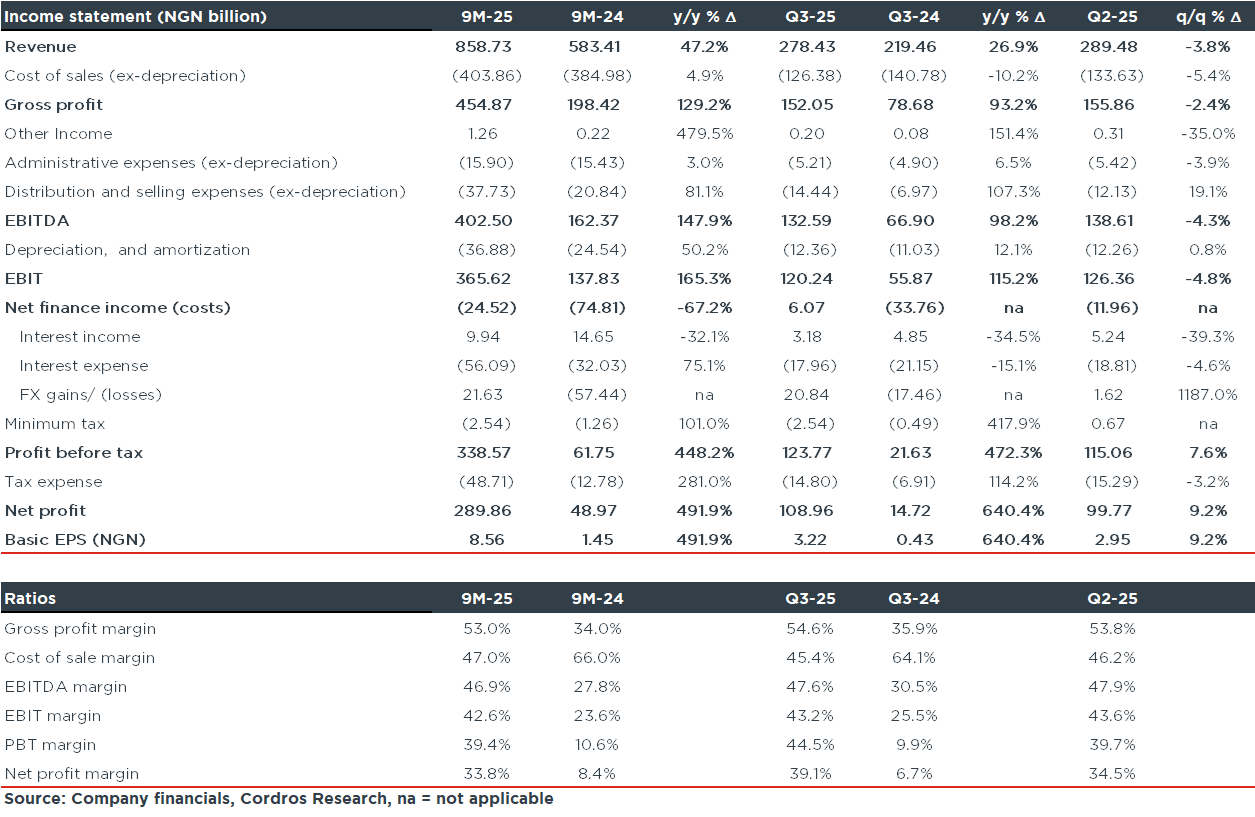

BUA Cement Plc (BUACEMENT) released its unaudited Q3-25 financial results on Monday (27 October), reporting a standalone EPS of NGN3.22 (+640.4% y/y), bringing the 9M-25 EPS to NGN8.56 (+491.9% y/y). The surge in EPS was driven by a 26.9% y/y increase in revenue and a 10.2% y/y reduction in the cost of sales (excluding depreciation).

Revenue grew by 26.9% y/y in Q3-25 (9M-25: +47.2% y/y), supported by both price and volume increases compared to the same period last year. However, revenue declined by 3.8% quarter-on-quarter, reflecting the seasonal slowdown typically seen in Q3.

Interestingly, the cost of sales (excluding depreciation) decreased by 10.2% y/y (9M-25: +4.9% y/y), largely due to a sharp reduction in manufacturing costs (-49.3% y/y) and maintenance & technical fees (-53.2% y/y). As a result, gross margin expanded substantially by 18.76ppts y/y to 54.6% (9M-25: +18.96ppts y/y to 53.0%).

Similarly, EBITDA and EBIT margins also expanded, rising by 17.14ppts y/y and 17.72ppts y/y to 47.6% and 43.2%, respectively (9M-25: +19.04ppts y/y and +18.95ppts y/y to 46.9% and 42.6%, respectively). This was achieved despite a 65.7% y/y increase in operating expenses (excluding depreciation), primarily driven by a 42.3% y/y rise in distribution costs, which accounted for 53.7% of total operating expenses.

On the finance side, the company recorded a net finance income of NGN6.07 billion in Q3-25, a significant turnaround from the net finance cost of NGN33.76 billion in Q3-24. This shift was driven by a reduction in interest expenses (-15.1% y/y) and an FX-related gain of NGN20.84 billion in Q3-25 (compared to the FX loss of NGN17.46 billion in Q3-24). In 9M-25, net finance costs decreased by 67.2% y/y to NGN24.52 billion.

Overall, profit before tax surged by 472.3% y/y to NGN123.77 billion, while profit after tax increased by 640.4% y/y to NGN108.96 billion, after accounting for a tax charge of NGN14.80 billion.

Comment: Similar to its peers, BUACEMENT carried the momentum from the first half of the year into Q3, delivering strong performance marked by sustained revenue growth, substantial margin expansion, and robust earnings growth. We expect the company’s positive trajectory to continue for the remainder of the year, supported by resilient demand, favourable pricing, and operational resilience. Our estimates are under review.