October 31, 2025/Cordros Report

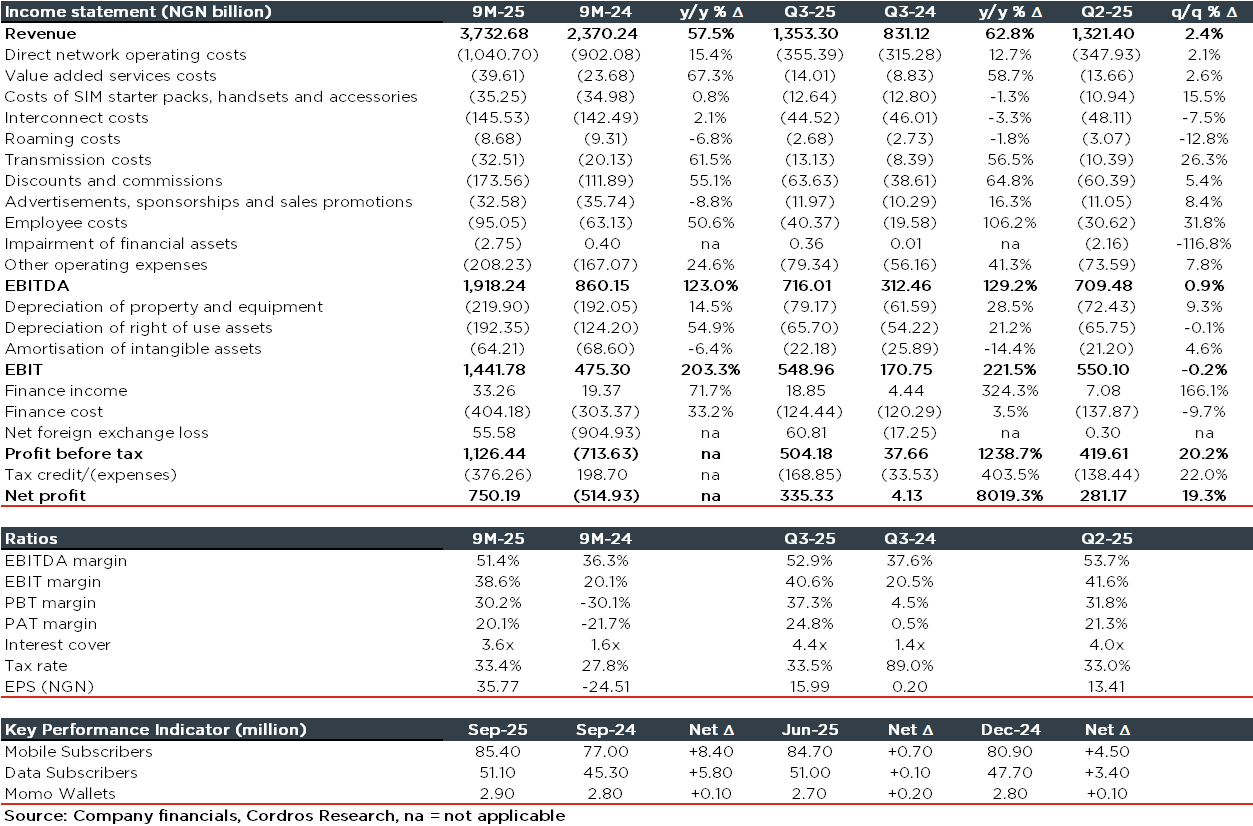

MTN Nigeria Communications Plc (MTNN) released its unaudited 9M-25 results after the close of business yesterday (30 October), reporting a standalone EPS of NGN15.99 (+80.2x y/y) in Q3-25, bringing the 9M-25 EPS to NGN35.77 (vs. 9M-24 loss per share of NGN24.51). The impressive performance was underpinned by strong topline growth (+62.8% y/y) and improved cost efficiency. Notably, the company declared a surprise interim dividend of NGN5.00/share, translating to a yield of 1.0%, based on the last closing price of NGN520.10 (30 October).

Service revenue increased by 62.9% y/y in Q3-25 (9M-25: +57.5% y/y), supported by broad-based growth across all business segments – data (+80.2% y/y; 55.5% of revenue), voice (+45.2% y/y; 34.2% of revenue), digital (+15.3% y/y; 1.7% of revenue), fintech (+73.6% y/y; 3.6% of revenue), and other service revenue (+44.0% y/y; 5.0% of revenue). In addition, non-service revenue (devices and SIM sales) grew by 44.6% y/y (9M-25: +32.1% y/y). On a q/q basis, total revenue advanced 2.4%.

Data remained the primary growth driver, supported by higher data usage, expanding user base, increased traffic, and price adjustments. Precisely, data traffic grew 36.3% y/y, while average monthly usage per user rose by 17.9% y/y to 13.2GB, reflecting sustained demand for digital connectivity. At the same time, data subscribers increased by 12.8% y/y to 51.10 million (Q3-25 net additions: +100.00 thousand).

Voice revenue growth reflected continued subscriber expansion (+10.9% y/y to 85.4 million, with +700.00 thousand net additions in Q3-25) and pricing adjustments. Also, the digital segments benefited from increased engagement and targeted content offerings, while fintech revenue was supported by higher active wallets (+3.6% y/y to 2.90 million, with +200.00 thousand net additions in Q3-25), increased customer deposits, and higher interest income.

Meanwhile, EBITDA margin expanded by 15.31ppts y/y to 52.9% in Q3-25 (9M-25: +15.10ppts y/y to 51.4%), as strong revenue growth outpaced expenses. Specifically, total expenses grew by 22.9% y/y (9M-25: +20.2% y/y), driven by increases in cost of sales (+33.3% y/y) and OPEX (+19.4% y/y). The relatively slower expense growth was aided by naira appreciation, savings from revised tower lease agreements, and ongoing cost optimization initiatives.

Below the operating line, net finance costs declined by 8.9% y/y to NGN105.59 billion in Q3-25, reflecting a 56.9% y/y drop in interest expense on borrowings and a 324.3% y/y increase in finance income, which offset a 16.8% y/y increase in lease interest. We also highlight that the company recorded a net FX gain of NGN60.81 billion (vs net FX loss of NGN17.25 billion in Q3-24) due to naira appreciation. For 9M-25, net finance costs rose by 30.6% y/y, driven by a 77.7% y/y increase in lease interest, while the company posted a net FX gain of NGN55.58 billion (vs. net FX loss of NGN904.93 billion in 9M-24).

Overall, profit before tax advanced by 12.4x y/y to NGN504.18 billion in Q3-25 (Q3-24: NGN37.66 billion), while profit after tax surged by 80.2x y/y to NGN335.33 billion (Q3-24: NGN4.13 billion).

Comment: MTNN continued its impressive performance in Q3-25, reporting robust revenue growth, expansion in EBITDA margin, and a significant increase in earnings. While we had anticipated a final dividend for the 2025 fiscal year, the interim dividend announcement, supported by the company’s return to a positive equity position (NGN293.14 billion) and positive retained earnings (NGN142.72 billion), came as a pleasant surprise. For Q4-25, we expect MTNN to maintain this strong momentum and finish the year on a high note, benefiting from continued pricing advantages and a more stable macroeconomic environment. Our estimates are under review.