October 31, 2025/Cordros Report

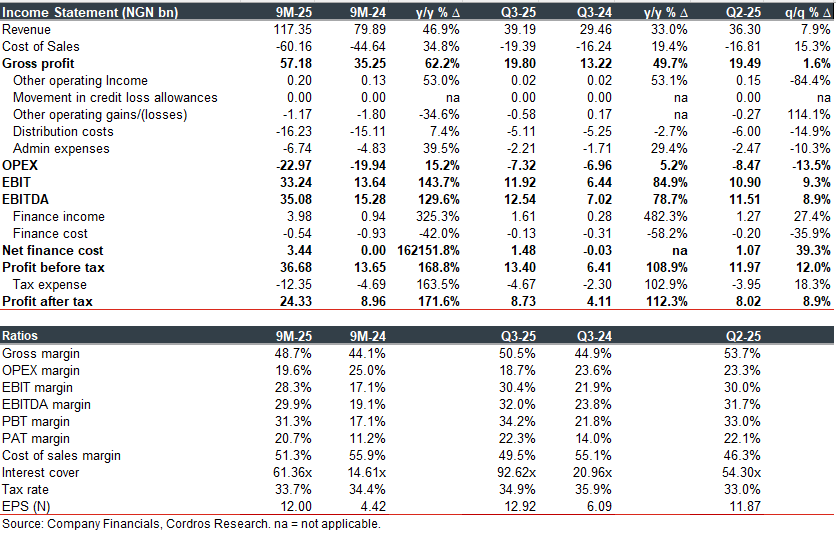

NASCON Allied Industries Plc (NASCON) published its Q3-25 unaudited financials on Thursday (30 October), reporting earnings per share (EPS) of NGN12.92 (+112.2% y/y), bringing 9M-25 EPS to NGN12.00 (+171.5% y/y). The performance was driven by a blend of strong revenue growth (+33.0% y/y) and improved cost efficiency, reflected in a 495bps y/y contraction in OPEX margin.

NASCON’s revenue rose by 33.0% y/y in Q3-25 (9M-25: +46.9% y/y), driven by effective pricing and moderate volume growth across all regional markets. The Northern region remained the dominant contributor (+40.6% y/y | 75.7% of revenue), while the Western (+11.6% y/y | 18.5%) and Eastern (+22.0% y/y | 5.8%) regions delivered modest gains.

The company maintained strong operating leverage in the period, as cost of sales grew at a modest pace (+19.4% y/y), significantly lagging topline expansion. This supported a robust improvement in gross margin, which expanded by 563bps y/y to 44.9% (9M-25: +461bps y/y to 48.7%). Operating efficiency bolstered profitability, as EBITDA margin expanded by 817bps y/y to 32.0% (9M-25: +1077bps to 29.9%), supported by a modest OPEX uptick (+5.2% y/y).

NASCON’s net finance income surged (+50.8x y/y) to NGN1.48 billion, driven by higher yields on short-term deposits (+482.7% y/y to NGN1.61 billion) amid elevated interest rates. Effective liquidity management further reinforced earnings quality and supported pre-tax profit growth (+108.9% y/y) during the period.

Ultimately, NASCON delivered a solid earnings performance, with profit after tax rising by 112.3% y/y to NGN8.73 billion in Q3-25, despite a relatively high effective tax rate of 34.9% (Q3-24: 35.9%). This reflected the company’s robust operating momentum, as post-tax profit advanced by 171.6% y/y to NGN24.33 billion in 9M-25, underscoring sustained margin expansion and improved cost efficiency across core operations.

Comment: We like NASCON’s continued focus on disciplined cost management, which has been instrumental in sustaining margin expansion through 9M-25. Looking ahead, we expect the company to maintain this positive trajectory through 2025FY, supported by strong operational efficiency, gradual volume recovery, festive-season demand tailwinds, and improving FX conditions. Our estimates are under review.