October 31, 2022/Cordros Report

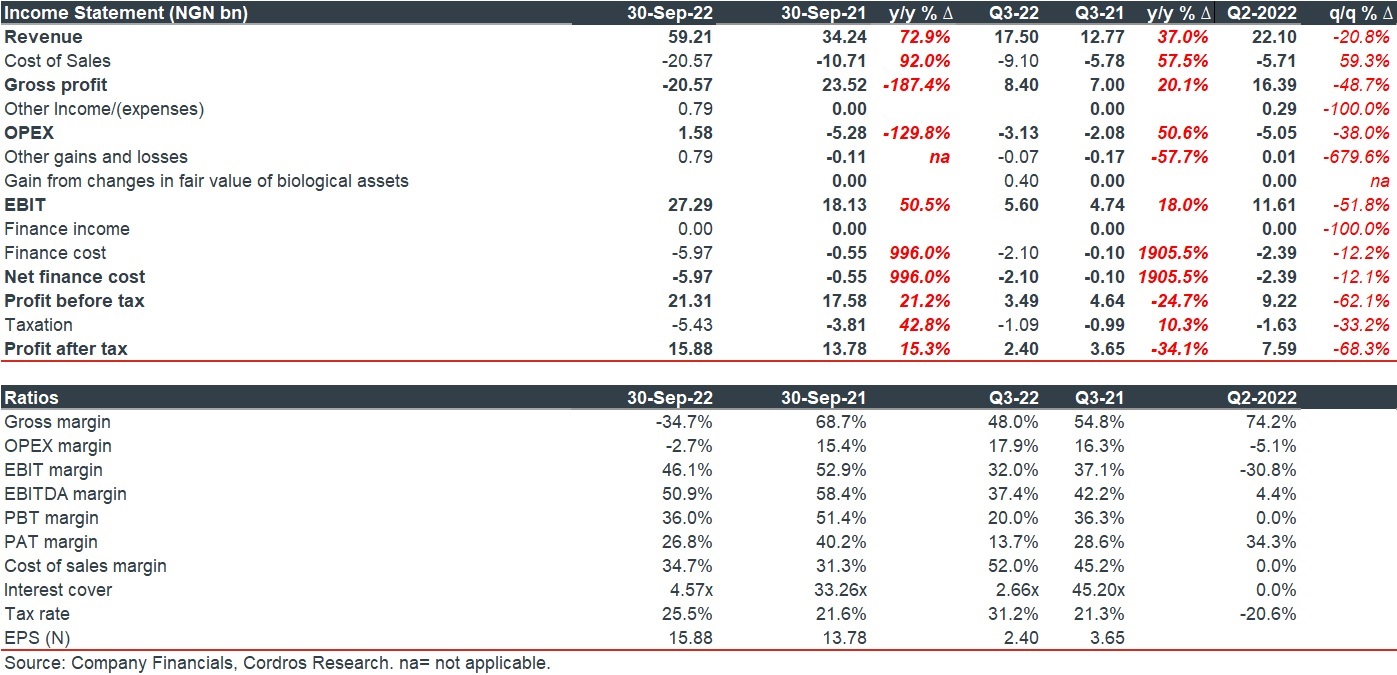

Presco Plc (PRESCO) published its Q3-22 unaudited financials over the weekend, reporting a standalone EPS of NGN2.40 in Q3-22 (Q3-21: NGN3.65). The moderation in EPS was driven by a sharp increase in net finance costs (Q3-22: NGN2.10 billion | Q3-21: NGN104.90 million). Consequently, the 9M-22 EPS settled at NGN15.88 (Q3-21: NGN13.78).

Revenue grew by 37.0% y/y in Q3-22, primarily driven by (1) increased volumes and (2) higher CPO prices. However, on a q/q basis, revenue declined by 20.8% q/q to NGN17.50 billion in Q3-22 (Q2-22: NGN12.10 billion), largely due to relatively lower volumes.

Gross margin contracted by 675bps to 48.0% in Q3-22 (Q3-21: 54.8%) following a faster rise in the cost of sales (+57.5% y/y) relative to revenue (+37.0% y/y). We attribute the higher cost to the (1) elevated energy costs and (2) increased cost of fertilizers following the surge in crude oil prices. Accordingly, EBITDA (-480bps y/y) and EBIT (-514bps y/y) margins declined to 37.4% and 32.0%, respectively, following the fall in gross margin (-675bps y/y) and a 50.6% y/y increase in operating expenses.

Net finance cost surged to NGN2.10 billion (Q3-21: NGN104.90 million) due to a higher interest expense in the absence of any finance income in the period.

Overall, profit before tax declined by 24.7% y/y to NGN3.49 billion (Q3-21: NGN4.64 billion). Following a tax expense of NGN1.09 billion (vs NGN988.36 million in Q3-21), profit after tax came in at NGN2.40 billion (Q3-21: NGN3.65 billion).

Comment: PRESCO’s overall performance remains decent, despite the dip in Q3-22 earnings following the surge in finance costs for the period. However, we are concerned about the burgeoning cost pressures following the effects on margins. Nevertheless, we remain optimistic about the company’s 2022FY performance, given the significant performance gains accumulated in H1-22. Also, we cite that upside such as tight border controls, FX liquidity challenges and the attendant impact on importers, and government support remain favourable for PRESCO’s earnings. Our estimates are under review.