May 31, 2023/Coronation Research

President Bola Ahmed Tinubu’s inaugural address was given yesterday, and it sparked the equity market’s imagination, with a rally of 5.23% today. The announcement of key market reforms, including phasing out fuel subsidies and unifying foreign exchange rates, shows that pro-market policies were not just items in the manifesto but issues which he is setting out to fix. If they are fixed, we expect much more from the equity market.

The President and the Equity Market

The equity market has been electrified by President Bola Ahmed Tinubu’s inaugural address, with a rise in the NGX AllShare Index of 5.23% today. Although there is little in the address that was not in the All Progressives Congress’s (APC) presidential manifesto, which has been available for five months, his statement of key pro-investment themes has persuaded the market that reform is on the way.

As we wrote earlier, see Nigerian Weekly Update, Nigerian markets post-election, 7 March 2023, the key potential beneficiaries of increased expenditure on infrastructure, proposed by the APC, are cement companies (our top pick being Dangote Cement) and the principal listed banks. What has set the market alight is the fact that manifesto pledges which are several months old have made it through into the President’s inaugural address, which was delivered yesterday.

The President’s speech has several specific messages for investors, namely, to tackle multiple taxation and other anti-investment inhibitions, and to ensure that foreign investors are able to repatriate dividends and profits (something which has been difficult in recent years due to low liquidity in the official foreign exchange markets).

The President also applauds the outgoing administration’s plan to phase out the fuel subsidy, pointedly remarking that it has “favoured the rich more than the poor.” Elimination of fuel subsidies, of course, is a key demand of foreign investors, particularly multi-lateral institutions and donors. According to the address, infrastructure, education, healthcare, and jobs will be the beneficiaries of the funds saved.

Next in the Presidential speech comes the issue closest to investors’ hearts, foreign exchange, the President stating: “The Central Bank must work towards a unified exchange rate. This will direct funds away from arbitrage…”

The first step, in our view, might be a merging of the various official exchange rates sanctioned by the CBN: the bigger step would be to fluctuate the exchange rate entirely, thereby making the parallel exchange rate redundant. Whether this will be done is open to question, though we note that there was a small (2.7%) rise in the value of the Naira against the US dollar in the parallel exchange rate market today.

Aside from matters directly affecting markets, the three main points of the address are to: a) use the budget to stimulate the economy in a non-inflationary way; b) use fiscal measures to promote domestic manufacturing; c) increase the level of electricity production. Another key aim is to reduce interest rates.

Without wanting to rain on the parade, it seems prudent to ask whether all these aims are compatible with each other. The most recent print for year-on-year inflation is 22.22% and the CBN’s policy rate is 18.50% while market interest rates (see page 1) are well below this. So, we would ask how increased budget expenditure will be funded, and if it is not funded then how inflation can be contained at the same time. We would also ask how the phasing out of fuel subsidy can be done without adding to inflation. We might even model a future in which inflation is rising while interest rates are held low – as was the case from the beginning of 2020 until May 2023 – and ask how the economy will fare under these conditions.

These difficult-to-assess questions make us focus on the two key reforms for investors: fuel subsidy removal and foreign exchange rate unification; and how soon the new administration will get these done. We expect this equity market rally to last a week or two, but if these two key reforms are achieved, then we would expect it to continue for much longer.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) lost 0.33% to close at N464.51/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) decreased by 0.05% ($16.25m) to US$35.18bn, as the CBN continues to intervene across the various FX windows.

The FX reserves of the CBN have slipped from N37.1bn to N35.18bn this year and are below their 10-year average of N37.0bn. Although the FX position is not as strong as it was, we do not think that the I&E Window rate is vulnerable, and that the CBN retains the ability to make small devaluations of the official rate over the coming months. However, as we show on page 2, changes in the FX regime may be afoot

Bonds & T-bills

Last week, average yields in the secondary market for Federal Government of Nigeria (FGN) bonds traded on a bullish note with average yields declining by 8bps to 13.98%. Yields moderated at the short end (-31bps to 10.84%), mid-end (-1bp to 14.36%) and long-end of the curve (-3bps to 15.33%).

The secondary market for T-bills also closed on a bullish note with average T-bill yields declining by 18bps to 6.80% as investors sought to make up for lost bids at the NTB auction held during the week. At the longest available maturity, the yield on a 335-day T-bill fell to 8.75% compared with a yield on a 342-day T-bill of 8.77% a week earlier. At the T-bill primary auction, the CBN allotted N180.45bn (US$392.28m) worth of bills, the same as the amount maturing. Demand was strong but slightly lower relative to the last auction. The auction recorded a total subscription of N811.40bn (N820.85bn at the last auction), implying a bidto-cover ratio of 4.50x (vs 5.70x at the last auction). Reflecting the elevated liquidity in the market, stop rates declined across the board; the 91-day bill declined by 221bps to 2.29%, the 182-day declined by 145bps to 4.99% and the stop rate on the 364-day declined by 100bps to 7.99%

Over the course of the year, we expect the overall direction of T-bill and FGN bond yields to be upward as increases in government borrowing are felt by the market.

Oil

Last week, the price of Brent extended gains for the second consecutive week, rising by 1.81% to settle at US$76.95/bbl. Brent is down 10.43% year-to-date and is trading at an average of US$81.19/bbl year-to-date, 18.06% lower than the average of US$99.09/bbl in 2022.

Oil prices rallied following a report from the International Energy Administration (IEA) in which it expects oil demand to outstrip supply by some 2 million barrels a day during the second half of 2023. Recent wildfires in Canada over the past week negatively impacted production and supply from the country. Lastly, Saudi Arabia’s oil minister hinted at a possible oil production cut at the OPEC+ meeting holding later this week, as he warned short sellers.

We maintain that for the most part of the year, prices are likely to remain well above the US$75.00/bbl set in Nigeria’s government budget.

Equities

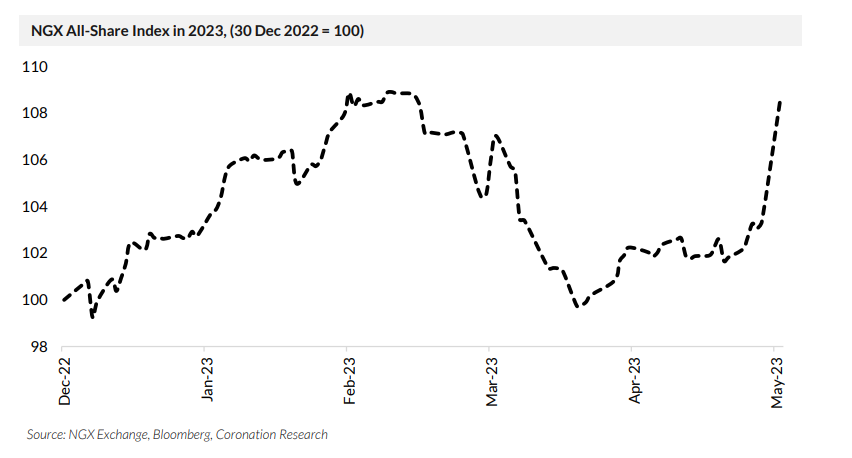

Last week, the NGX All-Share Index gained 1.51% to settle at 52,973.88 points. Its year-to-date return rose to 3.36%. Honeywell Flour Mills (+12.18%), Access Holdings (+11.76%) and United Bank for Africa (+11.38%) closed positive while Ardova (-13.90%), Oando (-5.08%), and Ecobank Transnational Incorporation (-2.44%) closed negative.

Performances across the NGX sub-indices were broadly positive as gains in the NGX Banking (+5.63%), NGX Pension (+4.55%), NGX Insurance (+3.59%), NGX Oil/Gas (+3.24%), NGX Consumer Goods (+3.10%) and NGX-30 (+1.85%) sub-indices outnumbered the loss in NGX Industrial Goods (-0.70%) sub-index.

Model Equity Portfolio

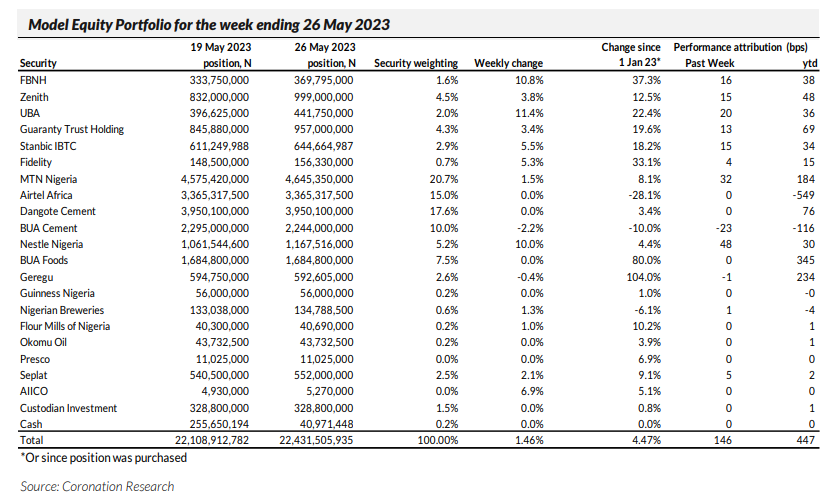

Last week the Model Equity Portfolio rose by 1.46% compared with a gain in the NGX All-Share Index of 1.51%, underperforming it by 5bps. Year-to-date it has risen by 4.47% compared with a rise of 3.36%% in the NGX All-Share Index, outperforming it by 111bps.

At the end of last week, we had a broadly neutral position in the main stocks on the market, though with a four-percentage point overweight notional position in MTN Nigeria, having announced our intention to build this notional position three weeks ago.

Looking at the significant market rally following the President’s inaugural address, we think there could be a rally in selected mid-caps, notably Nigerian Breweries, Guinness Nigeria, and Flour Mills of Nigeria. Being underweight in these stocks has proven to be an Achilles’ heel during past rallies, so for purely tactical reasons we intend to build these up towards notional neutral positions over the coming week, with the meager cash resource at our disposal.

From a fundamental point of view, and as described in Nigerian Weekly Update, Nigerian markets post-election, 7 March 2023, we think Dangote Cement, as well as other cement stocks, and banking stocks, will benefit from an increase in infrastructure expenditure. Therefore, we will look at ways of increasing our exposure here, and report back.