January 26, 2024/CSL Research

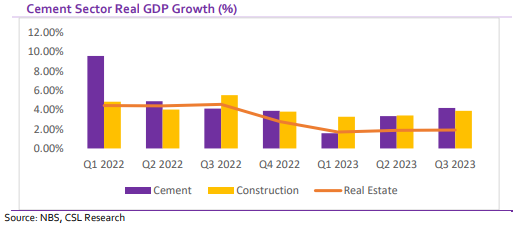

The year 2023 was fraught with several challenges for players in the cement sector. In Q1 2023, the country faced a cash shortage because of the Naira redesign program, which greatly distorted commerce. This, combined with the uncertainty surrounding the general elections, caused a pause in essential corporate and government construction projects, slowing down activities in the industry. In subsequent quarters, the country’s elevated inflationary environment, high energy costs, and most notably the devaluation of the naira in June 2023 impacted the bottom lines of cement manufacturers. Despite the several problems faced by the sector, output growth was sustained, reflected in its 4.20% y/y growth in Q3 2023. Related sectors such as real estate and construction also grew by 1.90% and 3.89% respectively.

For the cement players, price increases drove revenue growth, as the year was characterized by low demand due to constrained private consumer purchasing power and low government expenditure. As of 9M 2023, Dangote Cement, BUA Cement, and Lafarge Africa reported price hikes of 17.5%, 21.0%, and 23.0% respectively. However, while BUA Cement’s sales volume increased by 6.5% y/y, Dangote Cement and Lafarge Africa saw sales volume declines of 2.3% and 8.9% y/y respectively. Despite the price increases, cement players’ bottom lines were significantly impacted by the devaluation of the Naira in June 2023. In 9M 2023, the three major players in the industry BUA Cement, Dangote Cement, and Lafarge saw significant increases in their foreign exchange losses totalling about N135.38bn, up 441% y/y.

In 2024, we anticipate the cement sector will remain resilient, experiencing substantial year [1]on-year growth, particularly in Q1 2024, due to the favourable low base. We expect industry demand to improve as we believe consumer purchasing power will be less constrained in 2024 compared to 2023. We also believe we will see an improvement in government spending on infrastructural projects in 2024. While historical patterns suggest a potential CAPEX implementation rate of between 20% to 50%, we are optimistic there will be an improvement with the new administration. That said, challenges such as the high cost of raw materials, persistent inflationary pressures, and rising energy costs are downside risks to our expectations.