February 1, 2024/FBNQuest Research

According to the CBN’s most recent Quarterly Statistical Bulletin (QSB) for Q3 ’22, deposit money banks (DMB) aggregate credit extension to the economy increased by 4% q/q to NGN39.1trn. This growth rate was notably lower than the sector’s loan growth of 24% q/q in Q2 ’23. The significant credit growth during Q2 ’23 was primarily driven by the c.40% devaluation of the naira following the CBN’s decision to float the currency in June 2023.

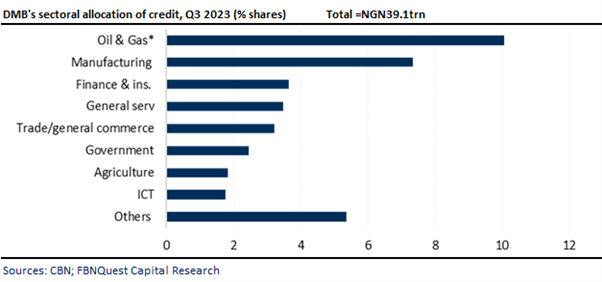

The oil and gas (O&G) sector, which accounted for the largest share of DMBs’ credit allocation at 26%, delivered a loan growth of 4% q/q.

Loans within the O&G sector, especially those allocated to industry, contribute significantly to the overall increase in loan expansion attributed to foreign exchange.

The manufacturing sector, with a total share of around 18.8% of DMB’s loan portfolio, saw a loan book growth of around 5% q/q.

Relative to Q2 ’23, the share of credit for manufacturing sectors remained steady at 18.6%.

Agriculture has failed to attract a meaningful proportion of the loan book. Credit extension to the sector was flat q/q, while its share of the loan book was a paltry 4%.

Beyond DMBs’ historical reluctance to lend to the sector due to inherent risks from sector counterparties and structural deficiencies, the prevalence of insecurity in food-growing regions further diminishes the sector’s appeal.

Despite the expansion of the loan book, DMBs managed to maintain their asset quality ratios below the regulatory threshold of 5%. The CBN reported a modest 10bps q/q increase in DMBs’ non-performing loans (NPL) to 4.2%

We expect the monetary authorities to maintain a tight monetary stance this year because of the issues with inflationary pressure and demand pressure on the naira.

As such, we expect Nigerian Banks to continue to benefit from the high interest rate environment. However, the potential downside risk lies in asset quality deterioration amid challenging economic conditions.