February 29, 2024/Cordros Report

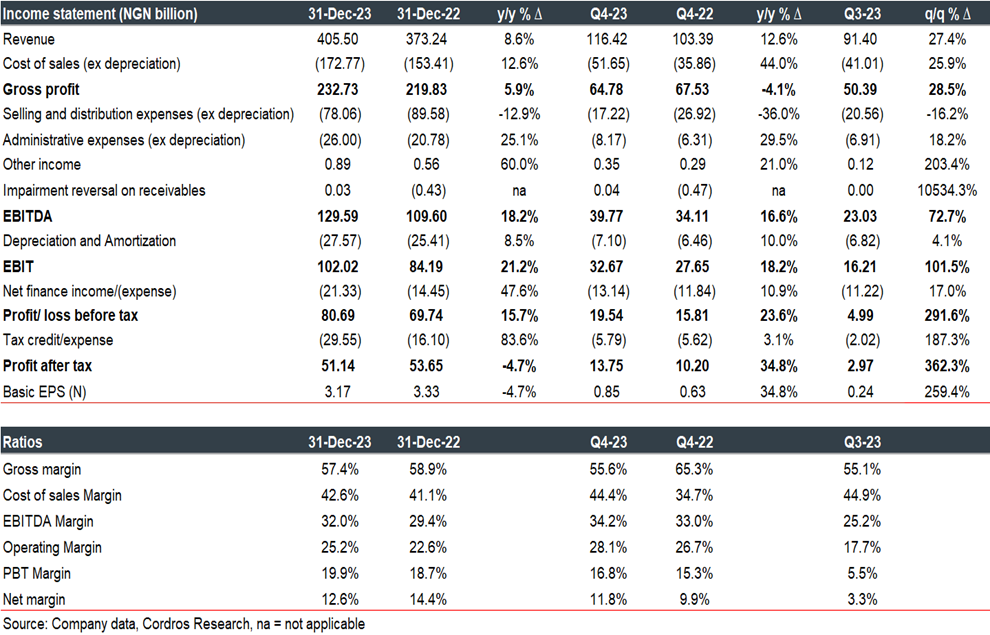

Lafarge Africa Plc (WAPCO) released its 2023FY audited financials today, reporting an EPS of NGN3.17 (2022FY: NGN3.33). The decline in the company’s EPS is attributable to the higher net FX losses (+84.0% y/y) and tax payments (+83.6% y/y) for the year, majorly due to its expired pioneer tax incentive. WAPCO’s board has proposed a final dividend of NGN1.90/s, translating to a dividend yield of 5.9% based on the closing price of NGN31.95/s (29 February).

Revenue grew by 8.6% y/y in 2023FY (2022FY: +27.3% y/y), reflective of the broad economic headwinds that slowed sales within the year and shutdown of the Mfamosing plant (which accounts for c.50.0% of production volume) for maintenance in Q3-23. Across its product segments, WAPCO saw improvement in sale of cement (+8.5% y/y | 96.8% share of revenue) and readymix and other product (+14.6% y/y | 3.2% share of revenue). Although management is yet to provide details on the breakdown, we posit that revenue was buoyed by upward adjustment of cement prices which as of 9M-23 was hiked by 23.0% y/y.

Gross margin weakened by 150bps to 57.4% in 2023FY, as the cost of sales ex-depreciation grew by 12.6% y/y, owing to higher cost of fuel and power (+21.6% y/y), production (+20.4% y/y) and maintenance (+21.8% y/y). The cost pressure was driven by the high inflationary environment and naira depreciation effect on the company’s FX-linked gas contracts.

Notwithstanding, EBITDA margin strengthened by 259bps to 32.0% y/y in 2023FY (2022FY: 29.4%) supported by a moderation in selling and distribution costs (-12.9% y/y) amid increased administrative expenses (+25.1% y/y) during the period. Consequently, the OPEX/sales ratio declined by 400bps to 26.0% in 2023FY (2022FY: 30.0%).

Following the devaluation of the naira in 2023, net finance cost spiked by 47.6% y/y as the group recorded net FX losses of NGN21.04 billion (+84.0% y/y) amid a 73.0% y/y rise in interest expenses, majorly from bank charges and other interest costs. Elsewhere, we highlight that the group’s finance income grew by 213.0% y/y.

Notably, PBT increased by 15.7% y/y to NGN80.69 billion in 2023FY. However, due to the expiration of the group’s pioneer status incentive in 2022FY, tax expense for the review period surged by 83.6% y/y to NGN29.55 billion. Sequel to this, PAT declined by 4.7% y/y to NGN51.14 billion in 2023FY.

Comment: WAPCO’s 2023FY performance highlighted challenges from economic headwinds within the cement industry, particularly stemming from reduced demand and local currency depreciation. Additionally, the shutdown of its major plant further hindered sales volume amid the group’s elevated tax expense in the year. In our view, we like that WAPCO remained resilient, as it curtailed operating cost pressures and remained profitable. Further out, we anticipate the group would deliver a stellar performance underpinned by our expectation of strong public and private sector demand coupled with management’s strategic focus on cost management and unlocking more capacity utilisation from its plants. Our estimates are under review.