March 25, 2024/CSL Research

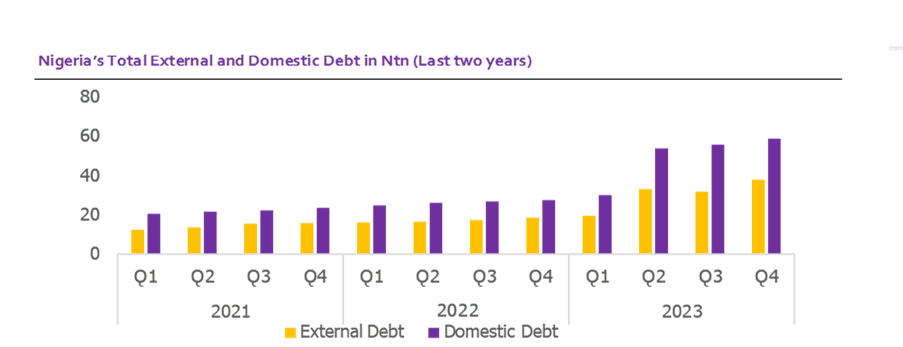

Nigeria’s public debt has been growing steadily in recent years, reaching a significant level of N97.34tn (US$108.23bn pegged at N899.39/$) as of 31 December 2023, according to the Debt Management Office (DMO). The total public debt stock includes the combined domestic and external borrowings of the Federal Government of Nigeria (FGN), state governments, and the Federal Capital Territory (FCT). The public debt reported in Q4 2023 is 110.46% y/y and

10.73% q/q higher than N46.25tn (US$103.11bn at N448.08/$) and N87.91tn (US$114.35bn at N768.76/$) reported in Q4 2022 and Q3 2023 respectively. The significantly higher debt level reflects the securitization of the Ways and Means facility and the impact of the currency devaluation on external debt. At current levels, the country’s debt-to-GDP ratio comes to 41.5% in 2023 from 22.9% in 2022 and higher than the 40.0% benchmark set by the DMO.

The total domestic debt of N59.12tn in Q4 2023 (vs N55.93tn and N27.55tn in Q3 2023 and Q4 2022 respectively) made up 60.74% of the nation’s total debt while the total external debt of N38.22tn (vs N31.98tn in Q3 2023 and N18.70tn in Q4 2022) made up 39.26%. The nation’s 2024 budget deficit of N9.18tn is expected to increase the country’s borrowings further in 2024. The expected Eurobond issuance in June 2024 is expected to add another layer of

pressure in 2024. On the revenue front, the government is pushing for higher oil revenue, with the budget premised on a 1.78mbpd oil output and oil price benchmark of US$77.96/barrel. We believe the oil estimate is ambitious, given that oil production remains constrained by theft and Nigeria might not be able to pump oil beyond 1.56mbpd in 2024.

Though the IMF still views Nigeria’s debt as sustainable, with minimal risk of default, debt servicing cost continues to rise, partly due to the weaker currency on external debt financing and the still elevated interest rate environment, indicating that the country continues to spend a significant portion of its revenue on debt servicing, limiting its fiscal space. We believe that, while the country’s revenues remain constrained, the elimination of fuel subsidies, which accounted for more than 75% of gross oil revenue in 2022, will free up additional revenues in 2024.

Click here to read full PDF copy of report