April 3, 2024/FBNQuest Research

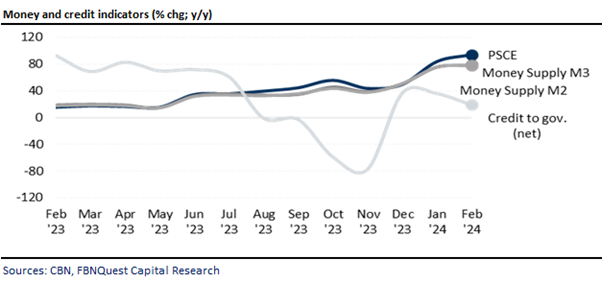

The Central Bank of Nigeria’s (CBN) latest data on monetary aggregates shows that domestic credit to the private sector almost doubled y/y to NGN80.7trn in Feb ‘24. This growth marks the fastest credit extension to the private sector in recent months. On a m/m basis, PSCE expanded by 6% m/m. The growth rate slightly outpaced the 5% m/m growth in Jan ’24. The PSCE data reflects lending from all sources, including CBN and state-owned development banks, such as the Bank of Industry, and smaller credit extensions by other banks, such as micro-finance and non-interest banks.

- Despite the CBN’s efforts to tighten monetary policy to tame rising inflationary pressures, private sector credit extension (PSCE) and other monetary aggregates have continued to expand.

- At its March’s meeting, the MPC raised the policy rate by +200bps to 24.75%. This follows a +400bps hike in January. The MPC’s aggressive stance is reflective of the committee’s resolve to address surging inflation and contain excess money supply in the system.

- Notably, the country’s rising headline inflation has been a significant concern to the monetary authorities. Nigeria’s inflation rate surged by 180bps to 31.70% y/y in February, up from 29.90% in January.

- The latest MPC communique highlighted the Naira depreciation as one of the significant drivers of inflationary pressures due to its adverse impact on domestic food prices.

- With respect to other monetary aggregates, broad money supply (M3), and M2 money supply showed similar growth of 79% y/y and 78% y/y respectively.

- The sustained rise in monetary aggregates continues to pose a major concern to the MPC, as it is viewed as one of the underlying drivers of inflation.

- Credit extension to the government increased by 19% y/y to NGN33.9trn as at end -Feb ’24, a moderation from the growth of 37% y/y registered in the previous month.

- Looking ahead, we expect to see a slowdown in credit extension to the private sector as banks tighten their risk management frameworks in response to the prevailing elevated environment.

- Additionally, the upward review of the CRR of merchant banks to l4% from 10% is expected to limit the amount of loanable funds to the real sector.