April 23, 2024/FBNQuest Research

The most recent update from the Debt Management Office (DMO) on Nigeria’s public debt shows that the FGN’s total external debt obligations increased by US$900.6m (+2% q/q) to US$42.5bn in Q4 ’23. Compared to the previous quarter, the smaller rise in the external debt stock in Q4 was mainly due to an increase of US$863.6m from the World Bank Group. Based on standardised metrics, the total external debt equals c.16.6% of 2023 GDP.

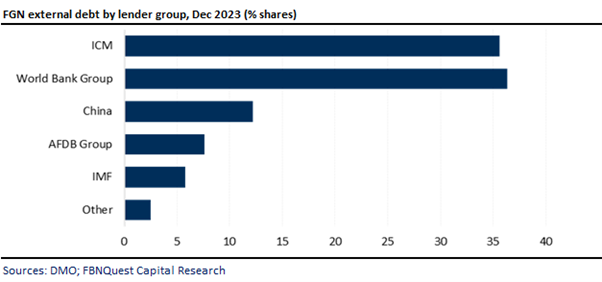

- Regarding debt split, the FGN holds 89% of the total external debt, while the balance of US$4.6bn is debt owed by state governments to multilateral and bilateral lenders, which the FGN guarantees.

- Debt obligations to multilateral lenders increased by a modest +3% q/q to about US$21.2bn, primarily due to a 6% q/q rise in loans owed to the World Bank Group.

- Due to an increase of US$516.9m q/q in loans from China, external borrowings from bilateral lenders rose by 7% q/q to US$6.0bn in Q4.

- Meanwhile, debt owed to commercial lenders remained flat q/q at US$15.1bn, reflecting more arduous global credit conditions in the international capital market.

- The 2024 budget projects a fiscal deficit of N9.2trn, which is to be partly financed by external borrowings of about N1.8trn (c.US$1.6bn).

- Regarding global monetary policy, the US Federal Reserve projections for a 75bps interest rate cut this year appear to have been dampened by downward sticky inflationary pressures and the continued resilience of the US economy.

- However, we expect the European Central Bank (ECB) and Bank of England (BOE) to reassess their monetary stances this year in alignment with the Swiss National Bank (SNB).

- As a result, we anticipate less restrictive conditions on the international capital market for the FGN to seek new loans this year, compared to the stringent conditions observed in 2023.