April 23, 2025/S & P Global

- Global Risk Watch.

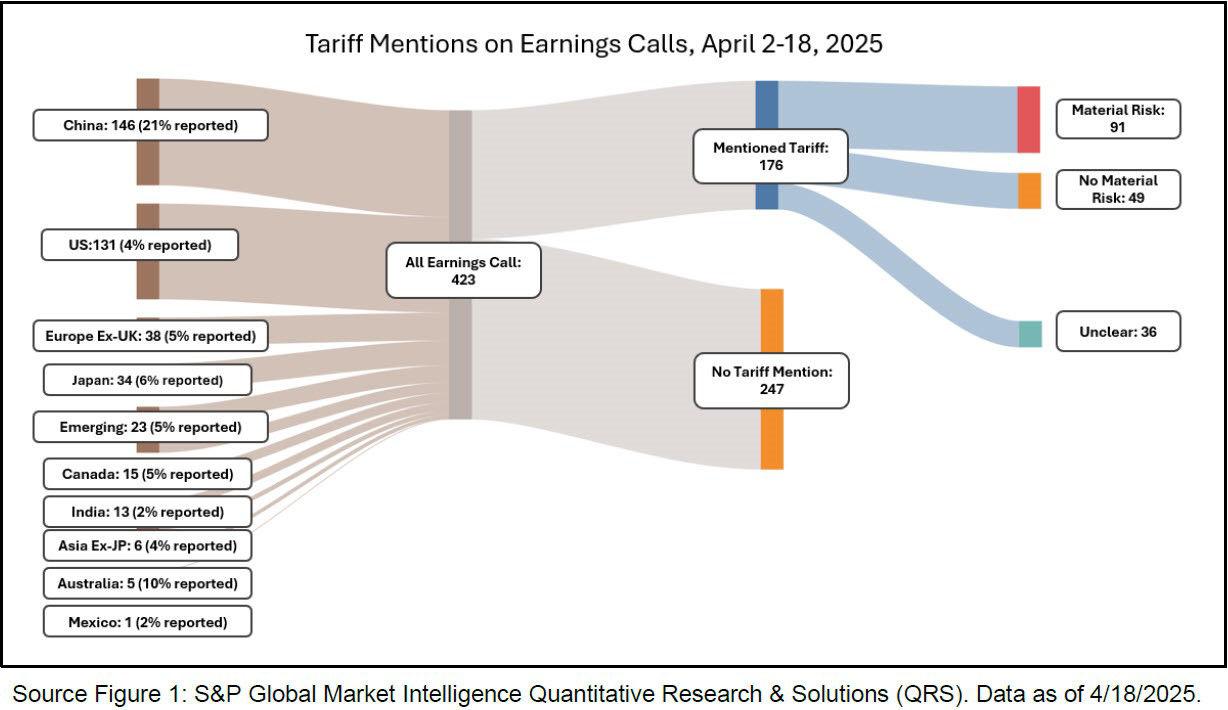

- Since April 2, 42% of earnings calls have included a discussion of tariffs, with 22% citing material risks.

- Consensus revenue estimates for 40% of companies worldwide have now been revised lower and short interest is 46% higher.

- Credit spreads are off the April 9 high but remain ~20 bps higher than the pre-April 2 baseline.

- Geographical Differences.

- Earnings call sentiment on tariffs has been varied, with Japan’s sentiment most negative and China’s least negative (but not positive).

- Downward revenue revisions from sell side analysts are most notable in the U.S., Europe, and the U.K., while institutional buyside short interest has increased the most in Asia and Europe.

- Tariff Contagion to Other Market Segments.

- Private equity is facing liquidity challenges, with segment revenue forecasts for publicly-traded PE firms revised sharply lower for 2025.

- Financials and energy sectors have the highest percentage of downward revenue revisions and short interest increases, alongside widening credit spreads, likely due to expectations of lower global economic and industrial activity.

##

Full report attached or click here – Tariff Tools in Action: Tracking Impact with Data.

For more information, visit S&P Global Market Intelligence