October 22, 2025/FBNQuest Research

- The modest pace of private sector credit extension reflects a continued cautious lending environment, driven by elevated interest rates aimed at curbing inflationary pressures.

- Financial institutions have prioritised risk management over aggressive credit expansion due to broader macroeconomic headwinds. This conservative posture has constrained lending activity to the private sector.

- Notably, Nigeria’s headline inflation has shown sustained deceleration this year, decreasing for the sixth consecutive month to 18.02% YoY in September, down from 20.12% YoY in August.

- In response to the easing inflation trend, the Monetary Policy Committee (MPC) opted to ease monetary policy at its last meeting, ending a prolonged tightening cycle.

- Consequently, the committee reduced the Monetary Policy Rate (MPR) by 50 bps to 27.00%.

- Additionally, the MPC also adjusted the asymmetric corridor around the MPR to +250/-250 bps (from +500/-100 bps) and lowered the Cash Reserve Ratio (CRR) for commercial banks by 500 bps to 45%, signalling a broader intent to stimulate credit.

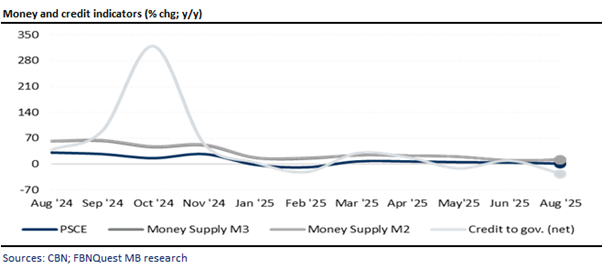

- Returning to the data, credit to the government contracted by -26% YoY to N23.1trn. However, on a m/m basis, credit extension to the government was up +7% MoM.

- Other monetary aggregates, broad money supply M3 and M2 grew by 12% YoY and 12% YoY to N119.52trn and N119.51trn, respectively.

- Looking ahead, given the softer MoM and YoY headline readings in September 2025, we anticipate that the committee will implement an additional rate cut when it meets next month.

- That said, a sustained reduction in borrowing costs could support renewed credit growth to the private sector. This is likely to have a positive impact on private sector investment, potentially boosting productivity and broader economic expansion.