July 26, 2021/CSL Research

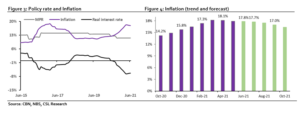

At the Monetary Policy Committee (MPC) meeting scheduled for today and tomorrow, we expect the MPC to keep the policy rate unchanged at 11.5%. Despite the growth trajectory witnessed in the first quarter of the year (Q1 2021), the economy remains fragile and significantly weaker compared with the pre-pandemic level. As such, a rate hike might worsen the fundamentals. Although, inflation retreated for the third consecutive month in June, risks are firmly tilted to the upside, a concern for the committee which should stop any consideration of a reduction in rate.

Growth expectations in 2021

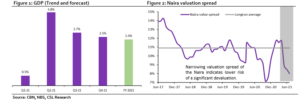

Many analysts expect that growth will increase significantly in 2021, owing to a low base in the prior year. While we acknowledge the base effect, our analysis suggests a muted/modest impact on most of the heavy-weighted sectors. To start with, output in the Agric sector (c.26 of the economy) in 2020 was largely unimpacted by the Covid-19 pandemic, with growth (2.2%) aligning with a 3-year average (2.3%). Beyond this, the 13.2% growth in the ICT sector (which accounts for 15% of the economy) in 2020 was 2x higher than the 5-year historical average, supported by work from home policy. As such, we expect a high base to result in slower output growth in 2021. We also expect output to remain depressed in both the real estate and domestic trade sectors (a total account for 22% of the economy), as the key driver of the sectors (domestic consumption) will probably not recover till 2022/2023. For the oil sector, we expect OPEC + agreement to continue to cap crude oil production. Overall, we forecast growth of 2.4% in 2021.

Though we expect the continued recovery of the economy to provide some respite for the committee, output growth remains fragile and a call for a rate hike may be considered too early.

NGN remains overvalued, but a large devaluation is unlikely

Since the last monetary policy meeting, the average parallel market premium is still elevated at 23%. This implies continued FX pressures despite the increased intervention by the CBN. In our view, the CBN’s drive towards currency unification, alongside higher oil prices, is yet to translate to tangible currency gains, with complaints of FX shortages persisting. Notably, several manufacturers and investors have continued to look to the parallel market to meet their FX needs.

NGN remains overvalued, but the recent tightened spread in Naira valuation and continued rebound in crude oil price is likely to shield a large devaluation. FX outlook appears less pessimistic in H2 2021, on the back of (1) the expected improvement in current account deficit position (1.2% of the GDP) and (2) Plans for Eurobond issuance. Also, the proposed increased SDR allocation by the IMF for its member countries could provide support for Nigeria’s external reserve accretion this year. The expectation is that Nigeria’s SDR allocation increase could be closer to US$3bn, which could prompt the government to approach the IMF for further RCF-type financing when the allocations are completed in Q3.

High base effect will likely soften the impact of security concerns on inflation

Headline inflation moderated for the third consecutive month to 17.8% y/y in June (May:17.9%), driven mainly by the high base effect from the prior year. We expect inflation to continue to moderate through H1 2021, supported by a high base and the absence of major price shocks. As such, this supports the prognosis for the MPC to retain the policy rate. Notwithstanding, we see an upside risk emerging from food inflation. Insecurity remains a bane to food production in the country. The Famine Early Warning Systems Network (FEWSNET) warns that widespread conflict arising from increased banditry, cattle rustling, kidnapping, and militancy could lead to the increased displacement of food-producing communities. Also, the Nigerian Meteorological Agency projects the likelihood of above-average rainfall (floods) affecting seasonal output towards the end of the year.

Overall, we expect the MPC to hold the MPR rate constant at 11.5%. However, the committee’s stance could become hawkish in the year’s ultimate meeting (in favour of exchange rate stability) if the trend in the global economy continues to foster economic wins for Nigeria.