April 12, 2023/Coronation Research

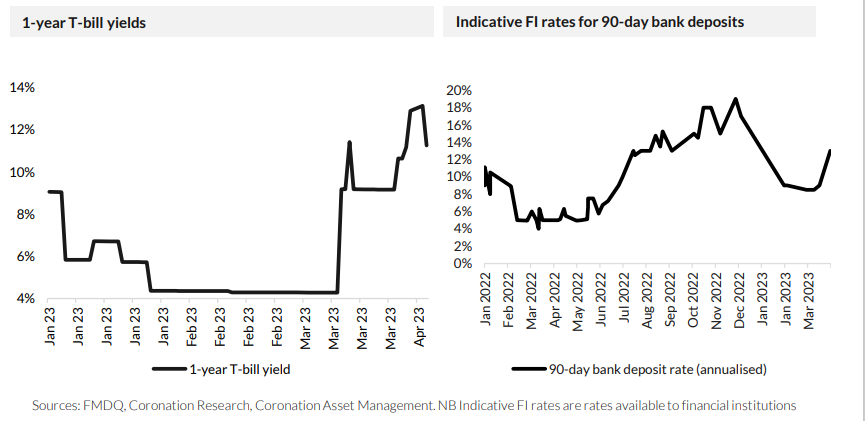

Savings rates at the moment offer returns not seen in months. We did not expect to see double digit T-bill rates until much later in the year. The Supreme Court’s reversal of the banknote replacement policy of the Central Bank of Nigeria has reduced liquidity at banks over the past few weeks. This has caused T-bill rates and certain types of deposit rate to spike.

The Big Jump in Savings Rates

This year market interest rates have been volatile, and at the moment savers have much better opportunities than they had at the beginning of the year. The explanation for these big swings in rates lies in the banknote replacement policy of the CBN, in our view, and the overruling of that policy by the Supreme Court in March.

The CBN’s policy to withdraw old Naira bank notes and reissue new ones had one clear characteristic, namely lack of new banknotes. This meant long queues at ATMs, and an observable strain on the inter-bank payment system as cashless customers attempted to transact with each other (clearly, the infrastructure cannot cope with the cashless society just yet). The other, slightly less obvious, effect was that commercial banks were suddenly liquid with their customers’ cash. When they bid at T-bill auctions they had plenty of money to spend.

This depressed rates all the way from January through to mid-March, with the 1-year T-bill rating trending as low at 3.78%. Next, and following the ruling of the Supreme Court, the CBN instructed banks to issue old notes again. This reversed the trend in their liquidity and, with less money to spend at T-bill and FGN bond actions, short-term rates moved sharply upwards again. This was also reflected in the indicative rates offered by banks to financial institutions for 90-day deposits.

Does this mean that today’s savings rates are exceptionally good, and that savers need to take advantage of them now? It is difficult to say, because we do not know the extent to which old banknotes have been reissued and the extent to which further reissues of banknotes are set to create illiquid conditions at banks, which could force rates upwards again. What is certain is that these rates are far better than what has been available for many months, although far short of the rate of inflation at 21.91% year-on-year.

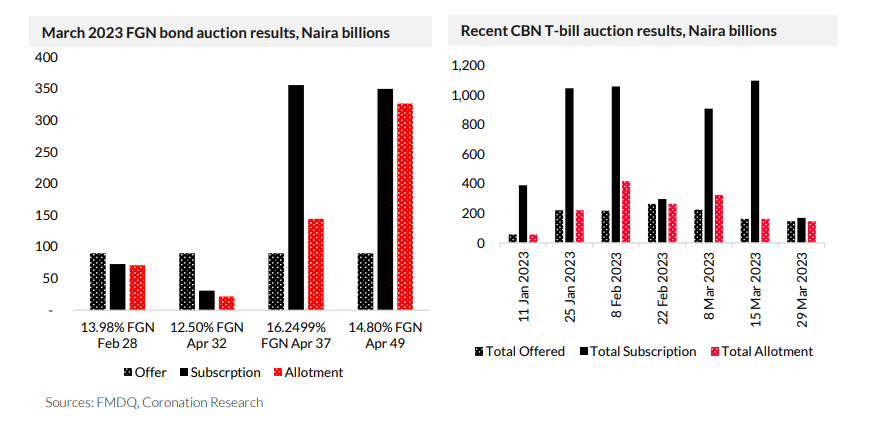

Note that the Debt Management Office (DMO), which auctions new FGN bonds, and the CBN, which auctions T-bills, have been behaving very differently from one another this year. The DMO has tended to sell at auction amounts of FGN bonds close to what bidders have subscribed.

This means it has come close to meeting investor demand for bonds, with the result that bond yields have not moved much. By contrast, the CBN has been selling amounts of T-bills close to what it offers, with allotments not reflecting the huge sums that were being bid during January, February, and early March. The result was a crash in T-bill rates while FGN bond rates did not change much at this time. Now the sums being bid at T-bill auctions are much less than before (see the results for the 29 March auction in the chart, above) and T-bill rates have risen.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) lost 0.41% to close at N463.25/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) decreased by 0.31% to US$35.39bn, as the CBN continues to intervene across the various FX windows.

This does not seem to be the time for a change in CBN policy, in our view. The CBN is likely to continue with its policy of gradually loosening the I&E Window rate while managing FX reserves close to their historic highs. We expect only small FX rate adjustments over the coming weeks and months.

Bonds & T-bills

Liquidity remained thin at the fixed income market last week, as investors sold positions across both the T-bill and Federal Government of Nigeria (FGN) bond markets.

Last week the secondary market in Federal Government of Nigeria (FGN) bonds remained bearish as the average yield closed up 49bps to 13.68%. The yield on the 3-year bond held steady at 12.03%, at 7-years rose by 23bps to 14.36%, and at 10-years rose by 48bps to 14.75%. The secondary market for T-bills was also bearish, with the average T-bill yield rising by 197bps to 7.76% and with the yield on the 336-day T-bill rising by 432bps to 12.98%.

Short-term swings in market liquidity are having profound effects on yields, which are volatile from one week to the next. The next T-bill auction is scheduled for 12 April and the next FGN bond auction is scheduled for 17 April, so the market may settle down over the coming week. Over the course of the year, we expect the overall direction of T-bill and FGN bonds to be upwards as increases in government borrowing are felt by the market.

Oil

Last week, the price of Brent gained for the third consecutive week, increasing by 6.71% to settle at US$85.12/bbl. Consequently, the year-to-date decline in Brent moderated to only – 0.92% and is trading at an average of US$82.33/bbl year-to-date, 16.92% lower than the average of US$99.09/bbl in 2022.

The increase in oil prices was supported by a surprising OPEC+ production cut in which members agreed to cut oil production by a total of 1.16 million barrels per day from May until the end of the year. Prices also drew support from a steeper-than-expected drop and a second consecutive weekly drawdown in U.S. crude inventories. We maintain that for the most part of the year, prices are likely to remain well above the US$75.00/bbl set in Nigeria’s government budget.

Equities

Last week, the NGX All-Share Index lost 2.28% to settle at 52,994.13 points. Consequently, its year-to-date return slipped to 3.40%. Airtel Africa (-10.00%), International Breweries (- 10.00%), Sterling Bank (-7.50%) and FCMB Group (-7.23%) closed negative while Oando (+34.12%), Sterling Bank (+6.67%) and United Bank of Africa (+2.40) closed positive. Performances across the NGX sub-indices were broadly negative as declines in the NGX Banking (-3.42%), NGX Pension Goods (-1.64%), NGX Consumer Goods (-0.47%), NGX Industrial Goods (-3.65%), NGX-30 (-3.42%) and NGX Oil/Gas (-0.11%) sub-indices outweighed a gain in the NGX Insurance (+2.19%) sub-index.

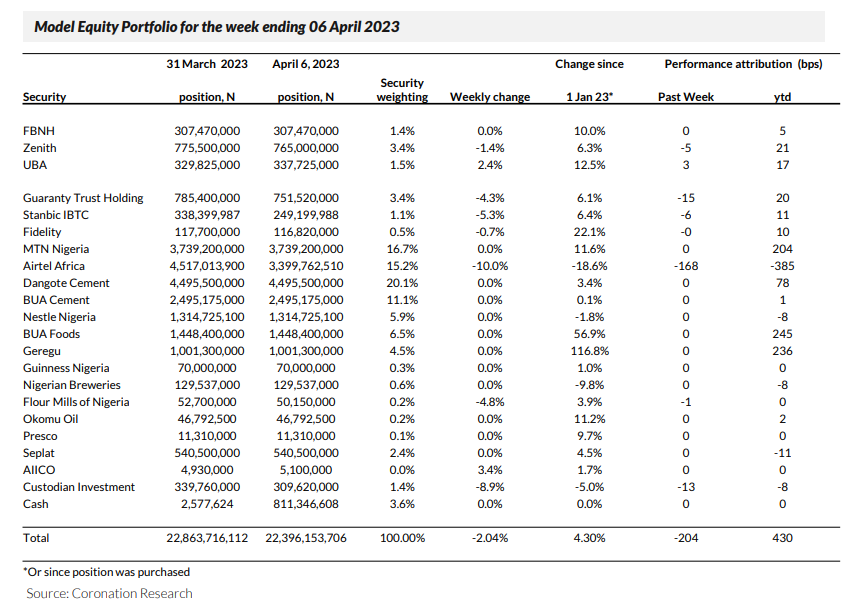

Model Equity Portfolio

Last week the Model Equity Portfolio lost 2.04% compared with a fall in the NGX All-Share Index of 2.28%, outperforming it by 24bps. Year-to-date it has risen by 4.30% compared with a rise of 3.40% in the NGX All-Share Index, outperforming it by 90bps.

As documented earlier in this report, market interest rates are rising and investors have opportunities in short-term Naira investments that were unavailable just a few weeks ago. At the same time, turnover on the NGX Exchange has been trending downwards, showing that investors are less interested in equities than they were during the run-up to February’s general elections. We still think that the equity market has the potential to deliver a positive return this year (because consensus earnings estimates point to an 18.0% advance in earnings among the top stocks) but we wish to reduce our notional equity exposure in the short term. Although we prefer to manage alpha (i.e. we like to pick stocks rather than call the market overall) we are finding this difficult this year, with not many themes to follow (and, when we do follow them, we find that that the market does not follow fundamentals). So, we are now set to work on cutting our notional equity exposure.

Our first task is to assess our notional overweight positions. These are Nestle Nigeria (272bps overweight) and Dangote Cement (327bps overweight). Nestle Nigeria reported good results at the end of February (Sales up 27% year-on-year, Net Profits up 22% year-on-year) but the market did not respond positively, even when the declared dividend was increased. Our mid-February foray into Dangote Cement has cost us 8bps to date, with the previously-announced buy-back not having had an effect yet. We intend to make notional sales in both stocks to bring our notional position in Nestle Nigeria to a 200bps underweight, likewise Dangote Cement.

Our next task is to assess whether commodity prices are likely to drive stock prices. Oil prices are rising and already we have adjusted our notional position in Seplat from an underweight to neutral; we will keep it there. International rubber and palm oil prices appear to be becalmed, so we will not adjust our underweight positions in Okomu Oil and Presco.

Next comes the question of how to position ourselves overall in a market that we suspect is due for correction. In such a correction we have found that consumer-facing industrials (such as Flour Mills of Nigeria) and brewers tend not to perform well. We will make further notional sales here in order to make our currently underweight positions more so. These adjustments, on the other hand, are unlikely to have much effect since their current weights in our Model Equity Portfolio are small.

So, we need to make adjustments among the major index weights. We intend to take our notional position in MTN Nigeria to 200bps below its index weight, likewise, Airtel Africa, while taking BUA Cement to 100bps below its index weight. Together, all these adjustments have the potential to increase our notional cash position from 3.5% to 17.5%, although we do not expect this to happen in a week (and, at that, a short week of four trading days) given that we are likely to face liquidity challenges (we take note of actual liquidity even though this is a notional portfolio). We will report back in just under a week.