May 2, 2023/Fitch Ratings

German banks have the ratings headroom to withstand the likely deterioration of their commercial real estate (CRE) loan books, Fitch Ratings says. Fitch’s assessment of the banks’ asset quality is adjusted downwards for cyclical performance and already reflects CRE sector and single-borrower concentration.

German banks’ exposure to CRE, both domestic and foreign, is high by European standards, and refinancing risks are increasing due to rising interest rates and falling market valuations. However, this should not result in outsized credit losses, at least in the near term, due to adequate collateralisation, long average maturities and predominantly fixed-rate loans in domestic CRE portfolios.

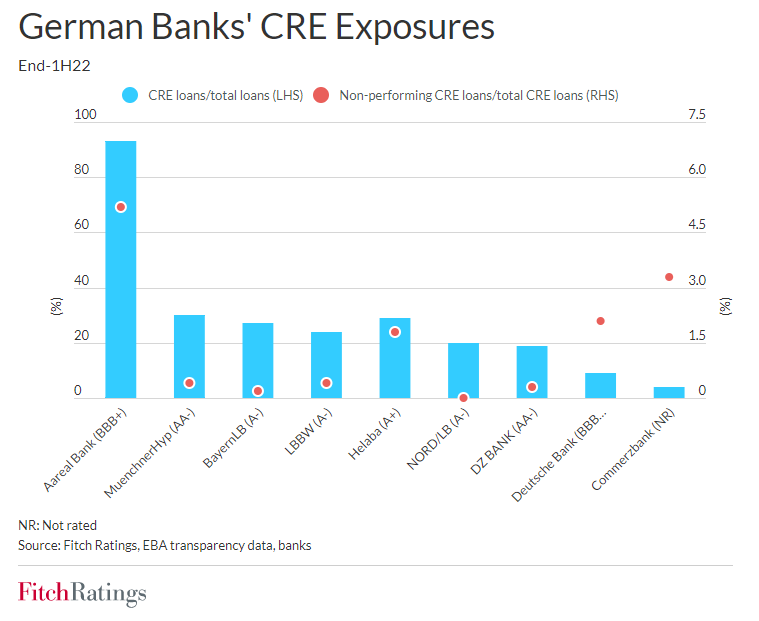

Loans backed by CRE collateral, including secured corporate lending, represent 7% of German banks’ assets and 19% of total loans, according to Bundesbank data, plus about a third of corporate loans, which is high compared to other large European economies (France: 15%, Italy: 20%, Spain: 16%). The nine largest German CRE lenders had about EUR290 billion CRE exposure at end-1H22, according to EBA data, primarily backed by residential properties and offices.

About 17% of German banks’ CRE exposure is international, mainly on prime assets and held by large banks. Most of this is in the US, led by Deutsche Bank (EUR17 billion at end-2022; 36% of common equity Tier 1 (CET1) capital), Landesbank Hessen-Thueringen (EUR11 billion; 106% of CET1 capital), Aareal Bank (EUR8 billion; 320% of CET1 capital) and Landesbank Baden-Wuerttemberg. The banks mostly finance properties in large cities and metropolitan regions, where they have extensive local market knowledge and established records.

German banks have increased their CRE lending significantly since 2015, using the opportunity to compensate for declining net interest margins, with covered bonds providing cheap funding and internal models keeping regulatory capital consumption low. Increasing market valuations have kept impaired CRE loan ratios at most large banks below 2%.

Although German real estate valuations have steadily increased since 2010, market values started declining in 2022. Residential CRE and office values declined by 4% in 2H22, and retail property values fell by 8%, according to the Association of German Pfandbrief Banks. Fitch believes prices could fall significantly further given the increase in interest rates.

Most German banks, unlike those in many other jurisdictions, adjust valuations downward to the ‘mortgage lending value’ at origination so as to strip out cyclical valuation swings for assets to be eligible for covered bond financing. The adjustments can be material and a reason why German banks often report higher loan-to-value (LTV) ratios.

CRE loans with higher LTV ratios will typically be amortising, recourse, or both, mitigating the risk to loan quality. Only a third of German banks’ CRE loans are non-recourse, on average, and these will typically be better-collateralised to mitigate the lack of a guarantor, particularly if they are also exposed to refinancing risk.

Higher interest rates are pressuring debt-service coverage ratios for the small proportion of floating-rate CRE loans where borrowers did not hedge interest rate risk. However, more than 60% of German CRE loans pay fixed interest rates (France: 80%, Italy: 18%, Spain: 26%), and only about 10% of the fixed-rate loans have a residual maturity of less than two years, mitigating refinance risk.

The Negative Outlook on specialist CRE lender Aareal Bank (BBB+) reflects pressure on asset quality and profitability. In contrast, Deutsche Bank’s (BBB+/Positive) exposure to CRE is relatively low. The ratings of the Landesbanken in the graph above are based on membership of the mutual support scheme of Sparkassen-Finanzgruppe (A+/Stable). The ratings of DZ BANK AG Deutsche Zentral-Genossenschaftsbank and Muenchener Hypothekenbank (both AA-/Stable) are based on membership of the mutual support scheme of Genossenschaftliche FinanzGruppe (AA-/Stable).