May 15, 2023/FBNQuest

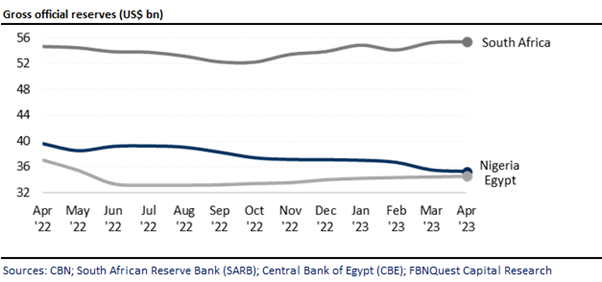

According to the CBN’s most recent data, Nigeria’s gross external reserves fell by a smaller margin of -USD246m m/m to USD35.3bn in Apr ’23, compared with -USD1.2bn in Mar ’23. The decline represents the ninth consecutive m/m decrease in the official reserves and is broadly consistent with the overall pattern observed since late 2021.

The decreasing trend of the gross official reserves can primarily attributed to minimal accretion to the reserves from crude oil sales due to ballooning payments for fuel subsidies. A secondary contributing factor is the limited inflow of foreign capital resulting from inherent weaknesses in Nigeria’s fx policy.

Although oil’s share of GDP is relatively small at around 5.7% (2022 GDP), it is by far the country’s largest source of fx, accounting for c.87% of merchandise export earnings in 2022.

According to data from the National Bureau of Statistics, total capital imported into the country plummeted by -20% y/y to a paltry USD5.3bn, the lowest amount recorded since 2016.

Total reserves as at end-Apr ’23 covered 7.3 months of merchandise imports on the basis of the balance of payments for the 12 months to Dec ‘22 and 5.5 months when we add services.

However, for a more accurate picture, we must adjust the gross reserve figure (and the import cover) for the pipeline of delayed external payments.

Conversely, the external reserves for South Africa and Egypt, the two other markets that we track across the continent, showed modest m/m increases in Apr ’23.

Egypt’s external reserves increased by slightly over USD100m m/m to USD34.6bn in Apr ’23.

Likewise, South Africa’s international liquidity position, a comparable figure to Nigeria’s gross external reserves, increased by USD141m during the month to USD55.4bn.

On a ytd basis, Nigeria’s gross external reserves experienced a sharp decrease of USD1.8bn, in stark contrast to increases of USD1.5bn and USD548m observed in Egypt’s external reserves and South Africa’s international liquidity position respectively.

It was widely anticipated that the planned removal of petrol subsidies, initially scheduled for June this year, would provide some respite to the gross official reserves.

However, the delayed implementation of the subsidies will have a negative impact on the short-term prospects of the gross official reserves.