July 11, 2023/FBNQuest

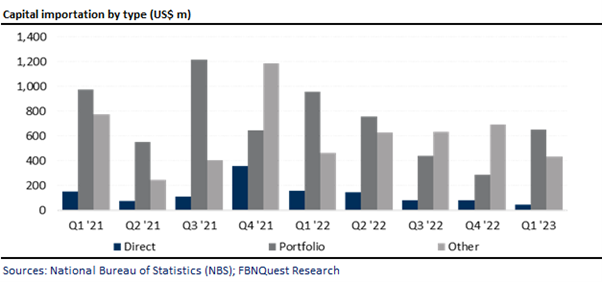

The National Bureau of Statistics’ (NBS) most recent data on capital importation show that the total value of capital imported into Nigeria improved slightly by 7% q/q to USD1.1bn in Q1 ’23. However, on a y/y basis, the value of capital declined by -28%, due to marked y/y decreases in all categories of investment inflows. The data was compiled using figures provided by the CBN obtained from banking transactions of all registered financial institutions in the country. The data are gross, and not adjusted for capital exports.

Portfolio investments contributed c.57%, or USD649m of the total capital inflow during the quarter. Although portfolio investments increased by 128% q/q due primarily to weak inflows in Q4 ‘22, they were down -32% y/y.

Fixed-income instruments (bonds) accounted for 46% of the total portfolio inflow. Surprisingly, equity-related inflow improved significantly to USD222m in Q1 ’23, surpassing the USD57m recorded for the entire year of 2022.

Other investments of USD436m were the second largest source of capital inflow into the country at 38% of the total. They consisted mostly of loans totalling USD434m.

Foreign direct investment inflow decreased by -43% q/q (and -69% y/y) to USD48m. It accounted for a paltry 4% share of total capital inflow during the quarter.

With respect to capital inflow by sectors, banking, production, and IT services were the top three sectors that attracted capital inflows during the quarter with USD305m (27%), USD256m (23%), and USD216m (19%) respectively.

In terms of destination, capital inflow remained concentrated, with Lagos and Abuja receiving around 62% and 36% of total capital inflow, compared with 57% and 40% in Q4 ’22 respectively.

The United Kingdom sustained its position as the leading source of capital inflow into Nigeria with USD674m worth of inflows. It was followed by the United Arab Emirates and the United States with USD108m and USD95m respectively.

Capital inflows into the country have been dwindling in recent years due to several reasons including fx liquidity challenges, macroeconomic uncertainty, and policy-related issues.

However, we anticipate that the removal of restrictions and policy reforms by the new administration will stimulate investor interest in the country in the medium term.