February 21, 2024/FBNQuest Research

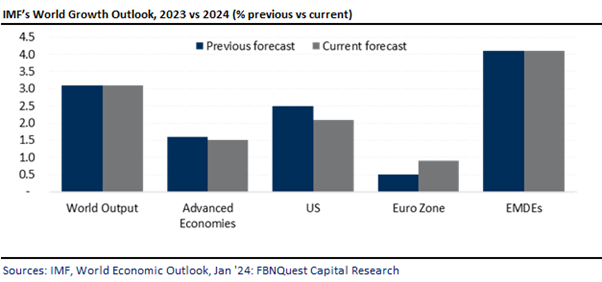

The IMF, in its most recent edition of the World Economic Outlook (WEO), retained its baseline growth forecast for the global economy at 3.1% in 2024, but improved its 2025 growth expectations to 3.2%. The fund noted the continuing threats to the recovery of the global economy. These threats include tightened global financial conditions aimed at combating inflation, weaker productivity growth, and reduction in fiscal support in the face of high debt burdens.

The Fund sees growth for the broad group of advanced economies declining to 1.5% in 2024 from 1.6% in 2023. However, the group’s outlook for 2025 was more favourable, with the Fund expecting growth to rise by 30bps to 1.8%.

Specifically, within the group, output growth for the US was lowered to 2.1% in 2024, from 2.5% in 2023 reflecting a restrictive monetary stance by the US Federal Reserve, gradual fiscal tightening and aggregate demand being weighed down by loosening US labour markets.

For the Euro zone, the region’s outlook was much better compared to the US. The FY’24 growth forecast was raised to 0.9% in 2024, from 0.5% in 2023.

For emerging and developing economies (EMDEs), the growth outlook was unchanged at 4.1% in 2024, before rising to 4.2% in 2025. However, expectations are divergent across regions. Compared with the Oct ’23 WEO update, the region’s projection was upgraded by +10bps.

Within EMDEs, China is projected to grow by 4.6% and 4.1% in 2024 and 2025 respectively, (vs 5.2% in FY ‘22).

Global inflation is projected to fall to 5.8% in 2024, down from 6.8% in 2023, before further slowing to 4.4% in 2024. The lower inflation projection is expected to be driven by reduction in core inflation due to tighter monetary conditions, softening labour markets and transmission effects of previous and current decline in energy prices.

The Fund noted that risks to global growth remain broadly on the balance, including lingering geopolitical and climate shocks, high food and commodity costs, persistent inflation which could trigger a further rise in monetary policy rates and sluggish recovery of China’s economy.

However, it pointed out the upside risks to stronger global growth, including faster decline in global inflation, quicker recovery of China’s economy and slower-than-anticipated withdrawal of fiscal support.