March 8, 2024/Fitch Ratings

The recent 400bp increase, to 22.75%, in Nigeria’s monetary policy rate (MPR) marks progress in the country’s efforts to contain inflation and support a more market-determined exchange rate, though real rates remain negative and the exchange rate is still subject to downward pressure, says Fitch Ratings. We highlighted low net reserves and weaknesses in the exchange-rate framework as constraints on the sovereign’s credit profile in November 2023, when we affirmed Nigeria’s rating at ‘B-’ with a Stable Outlook.

We believe the large MPR increase on 26-27 February, and accompanying moves to raise the cash reserve ratio for commercial banks to 45% from 32.5%, are steps towards containing inflation. The Central Bank of Nigeria (CBN) also widened the asymmetric corridor around the MPR, which could limit interest rate pass-through.

Fitch expects the CBN to continue tightening policy in the near term, which seems necessary to more fully control inflation as rapid credit and money-supply growth suggests a still-loose monetary context. Such a tightening will still face implementation challenges, partly due to the potential for countervailing political pressure. However, without further sizeable monetary tightening, it may be difficult to achieve macroeconomic stability – real interest rates remain negative, deterring inward portfolio investment.

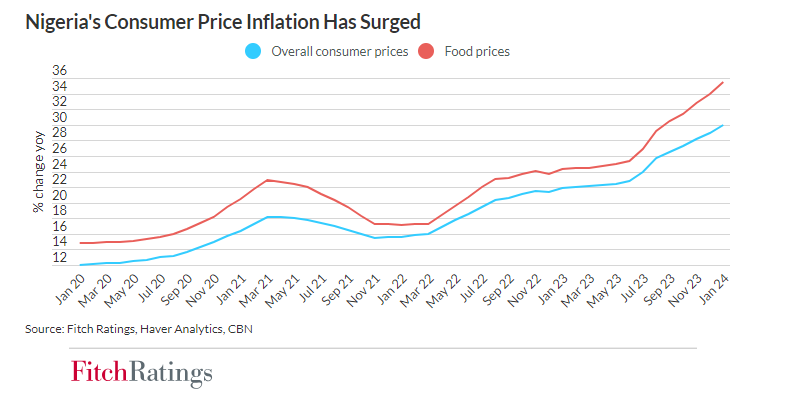

Fitch projects the rate of inflation to rise further in 1H24, before moderating in 2H24. This partly reflects base effects as well as our assumption that the naira’s depreciation will slow in 2024, compared with 2H23, before a stabilisation of the currency by year-end. We believe the currency’s sharp depreciation since mid-2023, including the large loss of value in January, and slow monetary policy response has raised inflation expectations, with security challenges in the north-east of the country and higher transport costs also adding to price pressures. We project inflation to average 26% in 2024.

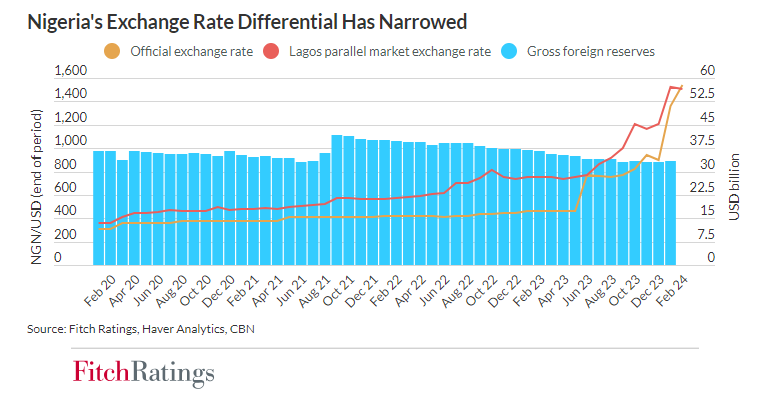

Recent CBN policy tightening, coupled with exchange-rate adjustments, signal initial efforts to address FX liquidity scarcity and restore business confidence. The CBN governor has announced plans to clear a backlog of unsettled FX forwards “in the next few days”, having settled only USD400 million of an outstanding USD2.2 billion, based on CBN estimates, as of late February. Nonetheless, the CBN’s weak net reserve position will continue to hamper liberalisation of the FX market and we expect FX scarcity to persist through 2024. Even if the authorities resolve the backlog of FX forwards, it will take time for investor confidence in the FX market to return, especially if transparency over exchange rate and monetary policy remains poor.

Recent measures, if continued, may ultimately strengthen the sovereign’s medium-term growth prospects and capacity to attract external financing. Fitch could look through short-term price volatility associated with the changes if we assess that their influence on Nigeria’s fundamental credit profile is positive. When we affirmed Nigeria’s rating in November, we stated that improved credibility and consistency in monetary policymaking and FX management, resulting in a sustained reduction of inflation and distortions in the FX market, could lead to positive rating action.

While the authorities are taking steps to address the challenges in the monetary and FX market, years of unorthodox policy approaches and financial repression under the previous government have weakened investor confidence in the economy. A lack of policy coordination remains a risk for the reform drive. Notably, Fitch expects fiscal consolidation to be limited in the near term, constrained by political pressure on the government to improve infrastructure and provide support to households amid high inflation. This could weaken the effectiveness of policies designed to curb inflation and improve FX liquidity.