May 31, 2024/CardinalStone Research

Elevated Interest Expense May Limit NIM Expansion

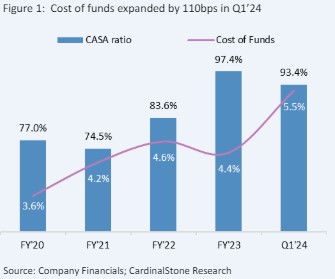

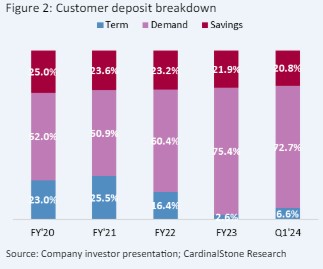

In FY 2024, management plans to maximise its net interest margin (NIM) by optimally pricing its credit assets in line with the interest rate environment and reducing its cost of funds. However, due to increased pressure from funding sources, we expect NIM to rise slightly in FY 2024. This view is consistent with the 4ppts contraction in the CASA ratio in Q1 2024, which was linked to the 3x surge in term deposits (6.6% of deposits). Therefore, given the 750bps increase in MPR to 26.25%, we see scope for a limited expansion in NIMs in the current financial year (+20bps to 8.3%, consistent with management’s guidance of 8.0% – 8.5%).

Waning NIR in FY 2024

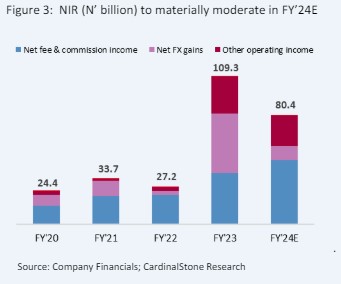

Excluding revaluation gains, we expect FIDELITYBK to report a 53.8% growth in NIR (vs 54.8% in FY 2023). We believe this growth will be driven by higher net fee & commission income (+25.0% YoY in FY 2024) and supported by expansion in the number of customers and activities on digital and electronic banking platforms. For context, over the last four years, net fee & commission income have contributed an average of 88.9% to NIR (ex. revaluation gains), underscoring its importance. Management desired to maintain the strong fee & commission income contribution pattern by boosting activities on its electronic banking platform (E-banking income has a 4-year mean contribution to NIR of 36.2%).

Meanwhile, based on CBN’s directive for the Net Open Position (NOP) limit, we estimate a moderation in FX revaluation gain. In Q1 2024, the bank recorded N3.3bn in revaluation gains, likely linked to the unwinding of its FY 2023 NOP of N16.8bn. Over the coming quarters, we forecast a significant decline in income from FX movements and project a lower unadjusted NIR.

Cost Pressures to Nudge CIR Higher

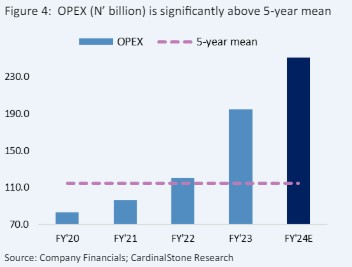

In Q1 2024, FIDELITYBK recorded an OPEX surge of 62.0% YoY (vs 61.4% in FY 2023), driven by higher regulatory charges, computer expenses, and personnel expenses. Management noted that its computer expenses included the cost of operating software priced in USD. Hence, Naira depreciation bloated this cost item. Additionally, regulatory charges, particularly AMCON charges, increased due to the bank’s growing total assets (+12.7% YTD).

Given the mentioned increase in the bank’s assets, we see latitude for sustained pressures from regulatory charges over the current full year. Hence, we project a 39.1% rise in OPEX and a 55.0% CIR in FY 2024 (vs 50.4% in FY 2023). This CIR projection remains within management’s guidance of below 65.0%. With the anticipated moderation of unadjusted NIR, we expect operating income to grow by 27.5% to N492.9bn (vs the stronger increase in OPEX), thereby pushing the cost-to-income ratio higher.

Subsidiary Expansion in the Offing

In the near term, management intends to grow the contribution from its London subsidiary to between 2.0% and 5.0% of group earnings, with a strategic intent to reach c.10.0% in the long term. Effective risk management practices, synergies, and strong corporate governance should enable this drive.

Additionally, management expressed strong interest in expanding its Pan-African presence, aiming to establish business exposures across West Africa, Southern Africa, and East Africa in the coming years. This commitment is expected to give the bank geographical diversification advantages such as relatively lower earnings volatility.

Shoring Up Capital to Meet N370bn Shortfall

In August 2023, the bank resolved to issue 13.2 billion new shares through a public offer and rights issue. Thus, it quickly communicated a three-stage capital raise plan to cover its shortfall of N370bn after the CBN’s new regulation on banks’ capital base. The plan will begin in June 2024 and run through Q1 2026.

In its first phase, the bank intends to raise between N120bn and N150bn and make up the shortfall in the subsequent phases of the exercise.

Valuation and Rating

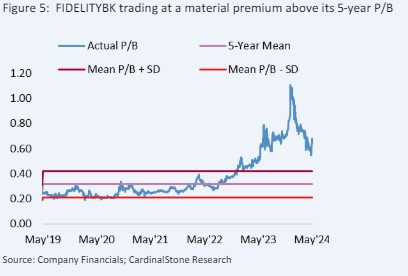

The net impact of our model adjustment translates to a downward revision of our 12-month TP to N14.80 (previously N15.67). This TP implies an exit P/B of 0.9x (vs. the 5-year average of 0.4x and the EMEA average of 1.1x). Our TP guidance is also 45.1% higher than the stock’s last market close price. We have a BUY recommendation on the counter.