September 30, 2024/Cordros Report

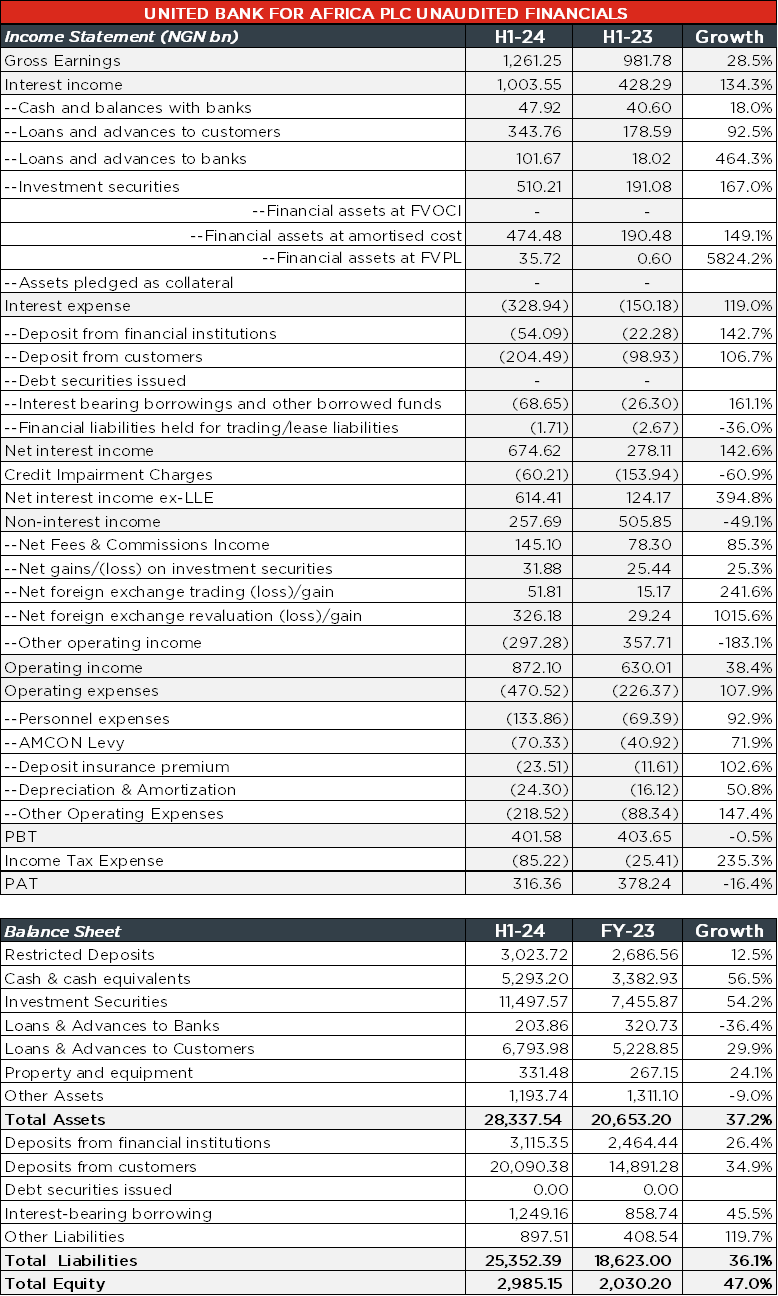

United Bank for Africa (UBA) released their H1-24 interim financials today (30 September), showing an 18.7% y/y decline in EPS to NGN8.90 (H1-23: NGN10.95). The decrease in the group’s EPS is attributable to the lower non-core income (-43.1% y/y) recorded, undermining the growth in the group’s core (+134.3% y/y) income. Notably, UBA is the only tier 1 bank to report a decline in EPS – ACCESSCORP (+103.5% y/y), FBNH (+94.7% y/y), GTCO (+223.1% y/y), and ZENITHBANK (+98.2% y/y). Meanwhile, the Board proposed an interim dividend of NGN2.00/share (H1-23: NGN0.50/share), translating to a dividend yield of 7.8% based on the last closing price of NGN25.75/share (27 September).

Interest income grew by 134.3% y/y to NGN1.00 trillion, driven by gains recorded across all the major lines. Specifically, the group generated higher income from investment securities (+167.0% y/y to NGN510.21 billion), loans and advances to customers (+92.5% y/y to NGN343.76 billion), loans and advances to banks (+464.3% y/y to NGN101.67 billion), and cash & bank balances (+18.0% y/y to NGN47.92 billion). Expectedly, the growth in these income lines was induced by a combination of the higher yield environment and the rise in the group’s interest-earning assets (+45.2% YTD to NGN23.79 trillion).

UBA recorded a 119.0% y/y growth in interest expense to NGN328.94 billion due to the higher cost incurred on deposits from customers (+106.7% y/y to NGN204.49 billion), borrowings (+161.1% y/y to NGN68.65 billion) and deposits from financial institutions (+142.7% y/y to NGN54.09 billion). We attribute the higher expense incurred on deposits from customers to the increase in the bank’s deposits (+33.7% YTD to NGN23.21 trillion) despite a slight improvement in the group’s CASA mix (H1-24: 87.5% vs Q1-24: 87.0%). Consequent to the faster growth in interest income than interest expenses, the group recorded a 142.6% y/y expansion in net interest income to NGN674.62 billion. Eventually, net interest income ex-LLE closed higher at NGN614.41 billion (+394.8% y/y) after factoring the 60.9% y/y decline in the group’s impairment charges in H1-24.

Non-interest income declined during the period by 49.1% y/y to NGN257.69 billion as the fair value loss on derivatives (NGN311.70 billion) compromised the gains from foreign exchange revaluation (+1,015.6% to NGN326.18 billion), net fees and commission income (+85.3% y/y to NGN145.10 billion), FX trading (+241.6% y/y to NGN51.81 billion), and investment securities (+25.3% y/y to NGN31.88 billion). However, the stellar growth in interest income was sufficient to offset the decrease in non-interest income, causing operating income to rise by 38.4% y/y to NGN872.10 billion.

Further out, operating expenses closed higher by 107.9% y/y to NGN470.52 billion, triggered by the increasing regulatory costs and persistent inflationary pressures. Precisely, the group incurred higher costs on personnel expenses (+92.9% y/y to NGN133.86 billion); AMCON levy (+71.9% y/y to NGN70.33 billion); fuel, repairs and maintenance (+218.7% y/y to NGN47.85 billion); and NDIC premium (+102.6% y/y to NGN23.51 billion) during the period. Accordingly, the group’s operational efficiency deteriorated as the cost-to-income ratio (ex-LLE) settled at 54.0% (H1-23: 35.9%).

Overall, profit before tax declined by 0.5% y/y to NGN401.58 billion. Eventually, the group’s profit after tax settled at NGN316.36 billion (-16.4% y/y), amid the higher income tax expense (+235.3% y/y to NGN85.22 billion).

Comment: We like the sturdy growth in the group’s core income line, as the elevated interest rate environment underpinned interest income growth. The preceding was enough to offset the lower non-funded income and surge in operating expenses amid the 60.9% decline in loan impairment charges. Looking ahead, we expect the group to close the year positively, as the high-interest rate environment and improved risky asset creation will remain a catalyst for earnings growth. Investors have reacted very positively to the result, with the stock currently trading at limit up. YTD, UBA is up +10.0%, compared to the NGX Banking index (+4.1%) and the broader All-Share index (+31.7%). Our estimates are under review.