October 31, 2024/Cordros Report

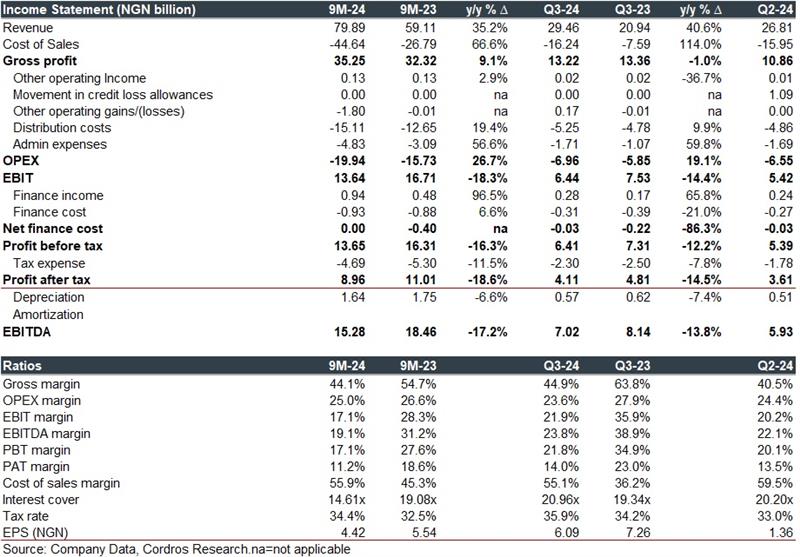

NASCON Allied Industries Plc (NASCON) published their unaudited Q3-24 financials today, in which the company reported a standalone EPS of NGN6.09 (Q3-23: NGN7.26), with 9M-24 EPS settling at NGN4.42 (9M-23: NGN5.54). The EPS decline reflects a substantial increase in cost of sales (+114.0% y/y) during the period.

NASCON’s Q3-24 revenue grew by 40.6% y/y (9M-24: +35.2% y/y). We attribute the revenue performance to strategic price increases (c.7.5%) in the salt & seasoning segments, necessitated by escalating input cost and NASCON’s aggressive volume drive in its core area of operations, the North. As such, revenue from the North grew by 40.3% y/y, contributing 71.7% of the total sales outturn. In the same vein, revenue from the Western (+41.8% y/y | 22.0% of revenue) and Eastern (+41.1% y/y | 6.3% of revenue) regions sustained strong growth momentum. Sequentially, revenue rose moderately by 9.9% q/q, driven by growth in the Northern (+9.3% q/q) and Western (+20.9% q/q) regions amid a decline in Eastern (-13.1 % q/q) region.

However, the gross margin fell by 18.89ppts y/y to 44.9% (9M-24: -10.56ppts y/y to 44.1%), following the significant increase (+114.0% y/y) in the cost of sales. We highlight that the higher cost print was driven by a 71.7% y/y (85.7% of COGS) increase in raw materials consumed and manufacturing (+125.1% y/y | 8.9% of COGS) expenses amid inflationary pressures. Consequently, EBITDA (-15.06ppts y/y) and EBIT (-14.06ppts y/y) margins declined steeply to 23.8% and 21.9%, respectively, as operating expenses rose by 19.1% y/y.

Further down, NASCON’s net finance cost declined by 86.3% y/y, underpinned by a 65.8% y/y increase in finance income due to higher interest income on short-term fixed deposits (+65.7% y/y). Meanwhile, the finance cost declined by 21.0% y/y.

Overall, profit before tax declined by 12.2% y/y to NGN6.41 billion (Q3-23: NGN7.31 billion). Following an effective tax rate of 35.9%, profit after tax printed NGN4.11 billion (Q3-23: NGN4.81 billion), translating to a decline of 14.5% y/y.

Comment: Cost pressures have remained a persistent challenge for NASCON this year, compressing margins and limiting earnings growth despite robust revenue gains. For the remainder of 2024E, we anticipate a continuation of the 9M-24 trend, with NASCON likely sustaining strong revenue momentum driven by price increases and volume growth from market penetration efforts. However, elevated input and operating costs, due to ongoing inflationary pressures and high energy prices, are expected to continue constraining margins and earnings expansion. Our estimates are under review.