October 31, 2024/Cordros Report

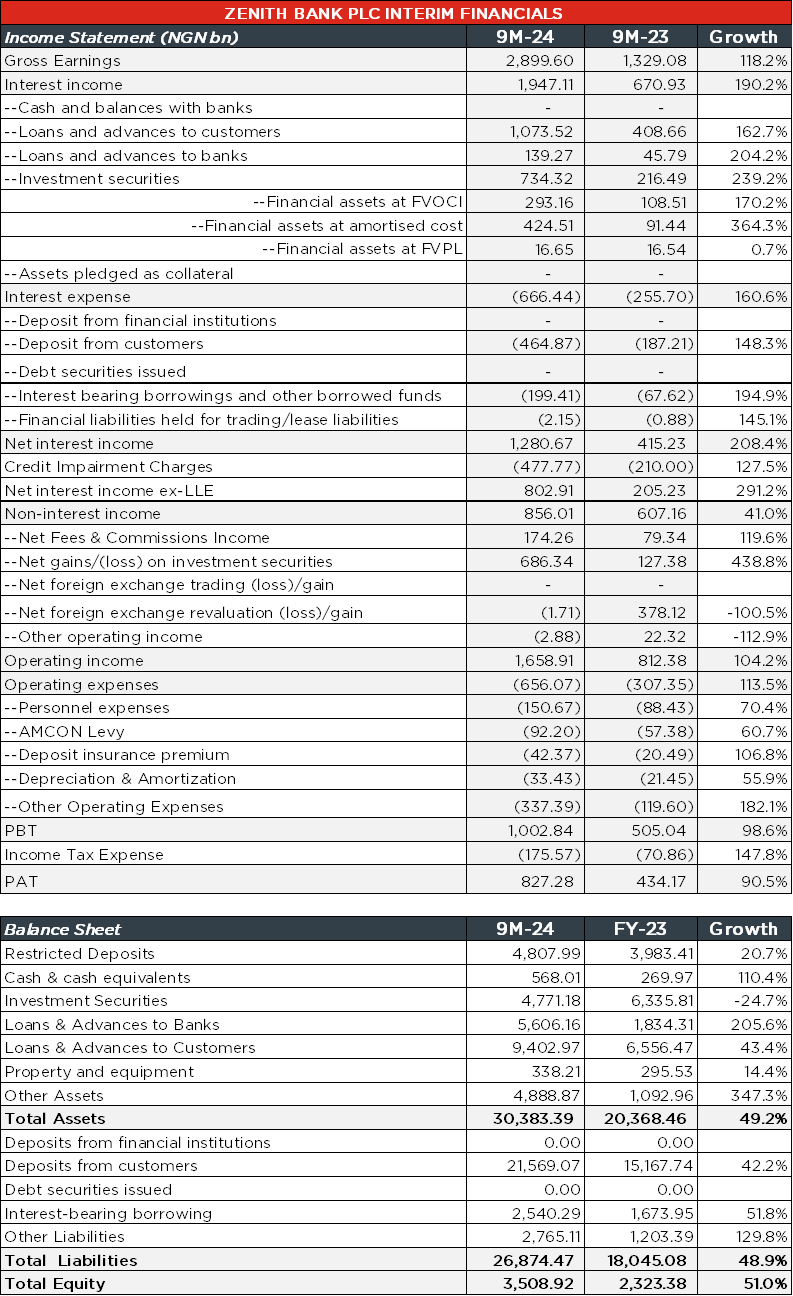

Zenith Bank Plc (ZENITHBANK) released their 9M-24 unaudited financials at the close of business yesterday (30 October), reporting a 90.6% y/y growth in EPS to NGN26.34 (9M-23: NGN13.82), driven by the expansion across the funded (+190.2% y/y) and non-funded (+41.0% y/y) income lines.

Interest income advanced significantly by 190.2% y/y to NGN1.95 trillion, mirroring the elevated interest rate in the debt market. Parsing through the contributory lines, the bank generated higher income from loans and advances to customers (+162.7% y/y to NGN1.07 trillion), investment securities (+239.2% y/y to NGN734.32 billion), and loans and advances to banks (+204.2% y/y to NGN139.27 billion) in the review period.

Similarly, the elevated interest rate environment pushed the bank’s funding costs higher as interest expense increased by 160.6% y/y to NGN666.44 billion. For clarity, ZENITHBANK incurred higher costs on customer deposits (+148.3% y/y to NGN464.87 billion) despite the improvement in the bank’s CASA mix in 9M-24 (83.2%| FY-23: 78.6%). Likewise, borrowing costs (+194.9% y/y to NGN199.41 billion) came in higher in the period under review, following the accretion in the bank’s interest-bearing borrowings (+51.8% YTD to NGN2.54 trillion). Accordingly, the bank’s net Interest income (ex-LLE) settled higher by 291.2% y/y at NGN802.91 billion after accounting for higher loan impairment charges (+127.5% y/y).

Further in, the bank reported a 41.0% y/y increase in non-interest income to NGN856.01 billion, as the higher gains from investment securities (+438.8% y/y to NGN686.34 billion) and net fees and commission income (+119.6% y/y to NGN174.26 billion) outstripped the FX revaluation loss (NGN1.71 billion) recorded in the period. Thus, the bank’s operating income edged higher by 104.2% y/y to NGN1.66 trillion.

Operating expenses increased by 113.5% y/y to NGN656.07 billion, following the higher costs incurred on personnel expenses (+70.4% y/y to NGN150.67 billion) and regulatory fees – AMCON levy (+60.7% y/y to NGN92.20 billion) and deposit insurance premium (+106.8% y/y to NGN42.37 billion) – in 9M-24. Given that OPEX grew faster than operating income, the bank’s operational efficiency waned as the cost-to-income ratio (ex-LLE) settled at 39.5% (9M-23: 37.8%).

Eventually, ZENITHBANK’s profit before tax expanded by 98.6% y/y to NGN1.00 trillion. Similarly, PAT grew by 90.5% y/y to NGN827.28 billion after accounting for income tax expenses (NGN175.57 billion).

Comment: ZENITHBANK delivered yet again a sturdy growth in interest income underpinned by the prevailing interest rate environment and the expansion of the bank’s earning assets (+35.7% YTD to NGN20.35 trillion). We like the bank’s positive traction in growing core banking activities, particularly in credit creation. For 2024E, we expect the bank to close the year positively, as the improved earning assets, higher yields in the fixed-income market, and stronger e-banking income remain upside factors. Our estimates are under review.