April 30, 2025/Corodros Report

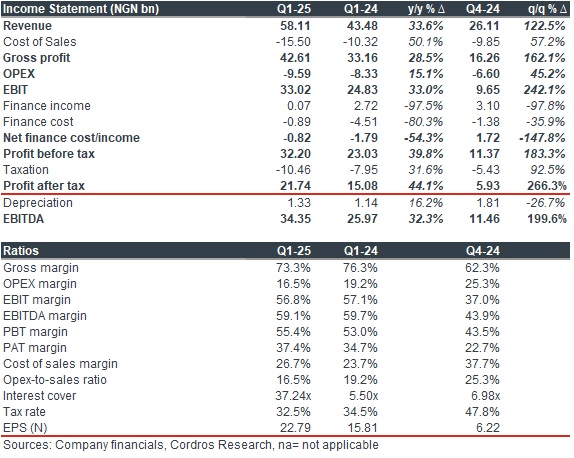

OKOMU Oil Palm Plc (OKOMUOIL) published its Q1-25 unaudited results today. The company reported a PAT growth of 44.1% y/y to NGN21.74 billion (Q1-24: NGN15.08 billion), translating to an EPS of NGN22.79 (Q1-24: NGN15.81) owing to the increased revenue growth (+33.6% y/y) in the period.

Revenue grew by 33.6% y/y in Q1-25 primarily driven by solid growth in sales – local (+29.1% y/y | 87.3% of revenue) and export (+75.9% y/y | 12.7% of revenue). The higher revenue mostly reflected higher Crude Palm Oil (CPO) prices in the period (Average CIF Rotterdam CPO price: USD1,050.45/mt in Q1-24 vs USD846.59/mt in Q1-24). Sequentially, revenue increased markedly by 122.5% q/q, most likely driven by higher volumes, given that H1 (Q1 and Q2) is typically the peak period for oil palm sales.

Gross margin contracted by 292bps to 73.3% in Q1-25 (Q1-24: 76.3%) due to heightened cost pressures – cost of sales increased by 50.1% y/y. The cost pressures likely reflect the spike in fertilizer costs, due to the impact of high production costs and supply shortages following export restrictions in China. Consequently, EBITDA (-61bps y/y) and EBIT (-27bps y/y) margins declined to 59.1% and 56.8%, respectively, amid an increase in net operating expenses (+15.1% y/y).

Net finance cost fell by 54.3% y/y to NGN820.08 million (Q1-24: NGN1.79 billion), primarily due to a sharp decline in finance costs (-80.3% y/y), reflecting a significant reduction in exchange losses during the period – NGN675.88 million vs NGN4.29 billion in Q1-24.

Overall, the company recorded a PBT growth of 39.8% y/y to NGN32.20 billion in Q1-25 (Q1-24: NGN23.03 billion). Following a tax expense of NGN10.46 billion, profit after tax grew by 44.1% y/y to NGN21.74 billion (Q1-24: NGN15.08 billion).

Comment: OKOMUOIL delivered a strong Q1-25 performance, driven by favourable pricing conditions amid steady volumes. Looking ahead, we expect OKOMUOIL to remain resilient through the year, even as global CPO prices face downward pressure due to recovering production in Southeast Asia and weakening import demand. Our estimates are under review.