In a sign of the rapid comeback by Nigerian lenders from the home grown financial crisis of 2009, a new global survey reveals that Nigerian bank customers have the highest level of trust for their preferred financial services providers (PFSP).

In a sign of the rapid comeback by Nigerian lenders from the home grown financial crisis of 2009, a new global survey reveals that Nigerian bank customers have the highest level of trust for their preferred financial services providers (PFSP).

The Ernst & Young (EY) 2014 global consumer banking survey released April 28th in Lagos, showed that 69 percent of Nigerian banking customers had confidence in their banks, the highest in Africa and second highest globally, behind India.

The study, titled : ‘winning through customer experience’, which surveyed over 32,000 banking customers in 43 countries, including Nigeria, Kenya and South Africa, shows that after a number of years of sharp decline, confidence in the banking industry is on the rise.

The results are particularly striking for Nigeria, whose banking industry neared collapse in 2009 as a result of a bad debt crisis, forcing the Central Bank to fire the chief executive officers of eight lenders and bail them out with N620 billion ($4 billion).

“Despite another challenging year for banks globally, confidence in the banking industry among African customers has experienced a significant increase, most notably in Kenya and Nigeria, with South Africa tracking the global trend,” Colin Daley, EY Advisory Banking Sector Leader for Africa said.

Further insights gleaned from the report as it affects Nigerian banking customers reveal that Nigerians have the highest sensitivity to close accounts, based on poor experience, in Africa and the second highest globally.

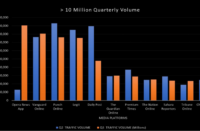

Nigerians are the heaviest users of ATMs, at 61 percent above the global average of 49 percent, although they also have a heavy preference to carry out branch transactions, which at 48 percent, represents the highest globally.

Conversely, Nigerian customers prefer to use advocates such as friends and family, when considering selecting a Financial Service provider.

At 35 percent, this represents the highest number across all countries surveyed globally.

Nigerian banking customers also feature actively online as they are among the top 3 countries that use social media when making decisions on selecting a Financial Service provider.

Nigerian customers say they are happy to build engagements with banks that help them to reach their financial goals, while 24 percent have experienced a problem with their banks that required resolution.

Seventy-two percent of customers were either very satisfied or satisfied with the response that they received, when they had a problem with their bank services. However, 28 percent were less than satisfied.

Daly said during a presentation of the results of the survey, that a bank’s ability to resolve customer problems had a substantial impact on advocacy for the bank – meaning that customers would not recommend their bank to those around them.

He said this affected advocacy, more so than satisfaction with a bank’s products, channels (including branches, online and call centres) and benefit delivery, combined.

But when advocacy does happen, the survey found that African customers expressed stronger advocacy for their primary financial service provider than globally.

Customers in Kenya (62 percent) are the strongest advocates, followed by South Africa (51 percent) and Nigeria (46 percent).

The survey finds there are three key improvement areas for banks: Making banking simple and clear, through transparency of fees, helping customers make the right financial decisions in a complex environment, through better advice and greater use of data and digital channels and working with customers when problems arise.

The return of consumer’s confidence in Nigeria’s banking system is a positive development that would help aid the sectors growth even as some analysts say banks stocks are a buy.

“Now is the time to have a strong bias towards Nigerian banks,” Kato Mukuru, an analyst at Exotix said, in a note to clients March 24. “Nigeria also offers something that few sub-Saharan African banking systems can hope to offer—scale.”

Source: Businessday (by Patrick Atuanya)