February 28, 2023/Coronation Research

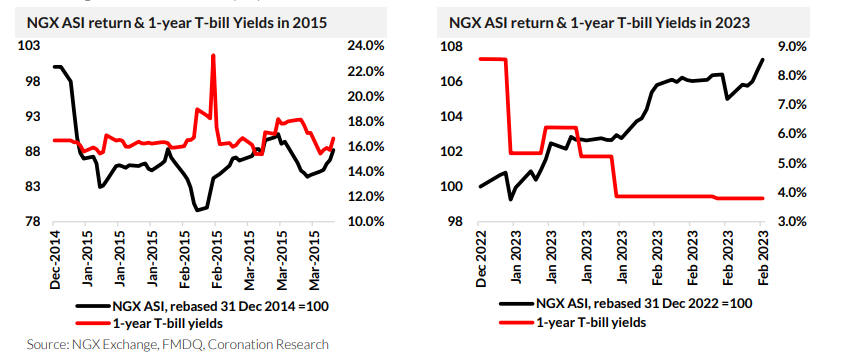

The equity market in 2023 differs from that of 2015. General elections typically bring about uncertainty and markets do not like uncertainty. In the run-up to the elections, the equity market declined 11.81% from the beginning of the year to March 28th, 2015. This year, however, the market has gained 7.96% year-to-date. What factors have changed since 2015 that may explain this difference?

Changing Dynamics: A Tale of Two Equity Markets

The equity market in 2023 differs from that of 2015. In January, we highlighted in our investment strategy outlook (see: Coronation Research, Better times in 2023, 11 January 2023) that the impending 2023 General Elections could affect the market similarly to how they did in 2015. Back then, the elections involved high levels of uncertainty as the newly emerging All Progressives Congress (APC) threatened the long-standing Peoples Democratic Party (PDP). Similarly, with three major parties (APC, PDP, and the Nigeria Labour Party) vying for the presidency in 2023, it’s hard to predict the outcome, and this could drive a risk-off sentiment in the equity market as it did in 2015.

However, this year, the equity market has defied expectations. In 2015, the general elections were originally slated for February 14th, but they were postponed to March 28th due to issues with Permanent Voters Card (PVC) distribution and insurgent activity in various North-Eastern states. In the run-up to the elections, the equity market declined 11.81% from the beginning of the year to March 28th, 2015. This year, however, the market has gained 7.96% year-to-date. What factors have changed since 2015 that may explain this difference?

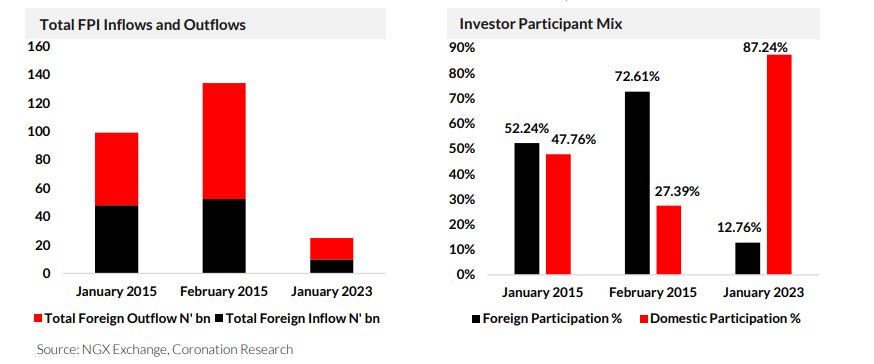

We believe that a change in the composition of market participants in the Nigerian equity market is a significant factor in the market’s bullish trend. According to the Domestic and Foreign Portfolio Participation report of the NGX Exchange Group, total transactions on the local stock exchange amounted to N189.72bn (US$958.18m) in January 2015. Monthly Foreign Portfolio Investment (FPI) transactions declined to N99.11 billion, down by 20.39% from December 2014. Domestic transactions fell from 51.76% in December 2014 to 47.76%, while FPI transactions increased from 48.24% to 52.24% over the same period. As foreign investors drove most of the total transactions on the exchange at the time, the market saw FPI outflows (26.92% of total transactions) outpace inflows (25.32%) in the run-up to the elections.

In February 2015, total transactions on the local stock exchange fell by 2.76% to N184.49 billion. The postponement of the elections further alarmed foreign investors, as monthly FPI transactions rose to N133.95 billion, up by 35.15%, driven by even higher FPI outflows (44.32%) than inflows (28.38%). Domestic investors were also worried, conceding approximately 45% of trading to foreign investors and causing domestic transactions to decrease from 47.76% in January to 27.39%, while FPI transactions increased from 52.24% to 72.61% overthe same period.

Since 2015, the number of foreign investors leaving the Nigerian stock market has been increasing due to several challenges, including the existence of multiple exchange rates that affect credible price discovery, and FX scarcity, which impedes repatriation of funds. As of January 2023, the total value of transactions in the nation’s stock market rose by 38.66% to N195.10bn (US$422.94m) from N140.70bn in December 2022. Although monthly FPI transactions increased by 63.71% m/m to N24.9bn, with FPI outflows (7.72%) still exceeding inflows (5.04%), the total value of transactions executed by domestic investors outperformed those executed by foreign investors by about 74%. As a result, the share of domestic investor participation rose to about 87%, while that of foreign investors dropped to about 13%.

The increased percentage participation by domestic investors in the local stock market is due to several factors: firstly, the limited investment opportunities in Nigeria’s money and capital markets; secondly, the expanded system liquidity, making riskfree assets such as treasury bills less attractive (see Coronation Research, ‘Why have savings ratesfallen?’, 13 February 2022); and thirdly, bargain-hunting investors holding positions to qualify for the upcoming FY 2022 dividend season. Although the reduction in foreign investor participation has short-term benefits in shielding Nigerian markets from global economic downturns that drive capital flight across global markets, the long-term consequences are far-reaching. We do not expect a recovery in foreign participation in our markets until a solution to the issues of multiple exchange rates and FX shortages is found.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) gained 0.02% w/w to close at N461.17/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) decreased by 0.15% to US$36.71bn, a 3-week high, as the CBN continues interventions across the various FX windows. The FX reserve position remains close to its historic high, and we doubt that the CBN wishes to see the exchange rate slip this year. Therefore, we believe that the current I&E Window rate, or something very close to it, can be maintained for at least several months.

Bonds & T-bills

Last week, the Federal Government of Nigeria (FGN) bond secondary market was bullish as the average benchmark yield for bonds fell by 12bps to close at 13.14%. Across the curve, the yields on the 7-year (-17bps to 13.94%), 10-year (-8bps to 14.31%) bonds declined, while the yield on the 3-year bond gained 13bps to settle at 11.51%. Our view remains that elevated Federal Government domestic borrowing will continue to drive yields upwards over the course of the year.

Activity in the Treasury Bill (T-Bill) secondary market was bullish as the average yield for Tbills fell by 2bps to 4.00%. However, the yield on the 349-day T-bill closed flat at 3.79%. At the T-bill primary auction, the DMO offered and allotted N263.50bn (US$571.38m) worth of bills. Demand was weak relative to past auctions this year. The auction recorded a total subscription of N296.75bn, implying a bid-to-cover ratio of 1.13x (vs 2.53x in the last auction). Consequently, stop rates expanded across the 91-day (+290bps to 3.00%), 182-day (+294bps to 3.24%) and the 364-day (+766bps to 9.90%, implying a 10.98% yield) bills. Elsewhere, the average yield for secondary market OMO bills remained unchanged at 3.77%, while the yield on the 67-day OMO bill closed flat at 3.02%.

Oil

Last week, the price of Brent rebounded, up 0.19% to settle at US$83.16/bbl. Nevertheless, Brent is down 3.20% year-to-date and is trading at an average of US$83.81/bbl, 15.42% lower than the average of US$99.09/bbl in 2022. Oil prices recovered slightly as speculation of further Russian production cuts and a rebound in Chinese demand offset inflation fears and continued inventory builds in the United States. Elsewhere, Russia signed a law that capped the maximum possible discounts on its Urals crude set at $34 per barrel in April and gradually declining to $25 per barrel in July. Hence, we maintain that prices are likely to remain well above the US$75.00/bbl set in Nigeria’s government budget.

Equities

Last week, the NGX All-Share Index gained 2.13% w/w to settle at 54,949.21 points. Consequently, its year-to-date return stood at 7.22%. BUA Foods (+15.59% w/w), Geregu Power (+13.84% w/w) and Fidelity Bank (+6.09% w/w) closed positive while Sterling Bank (- 1.31% w/w), Lafarge Africa (-0.58% w/w) and PZ Cussons (-0.49% w/w) closed negative. Performances across the NGX sub-indices were broadly positive as the NGX Consumer Goods (+6.30% w/w) led the gainers log, followed by NGX Oil/Gas (+2.73% w/w), NGX Banking (+2.21% w/w), NGX-30 (+1.92% w/w), NGX Pension (+1.31% w/w) and NGX Industrial (+0.34% w/w) while NGX Insurance (_+0.00% w/w) closed flat.

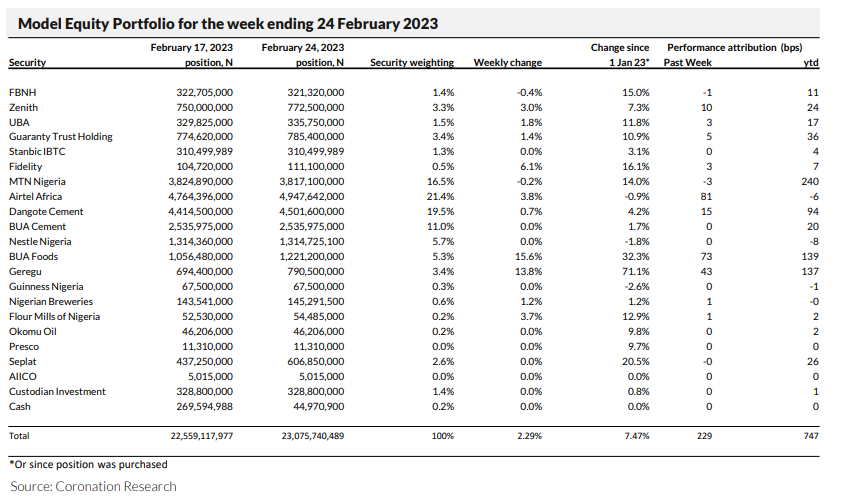

Model Equity Portfolio

Last week the Model Equity Portfolio gained 2.29% compared with a rise in the NGX All-Share Index of 2.13%, outperforming it by 16bps. Year-to-date it has risen by 7.47% compared with a rise of 7.22% in the NGX All-Share Index, outperforming it by 25bps.

Last week, and as earlier advised, we planned to continue to build our overweight positions in Dangote Cement, ahead of a positive market response to its upcoming Q4 and full-year 2022 results which we expect this week. We have maintained the overweight position in Dangote Cement at four percentage points above its index-neutral weight, after some additional notional purchases. In addition, we planned to increase notional positions in Seplat in a bid to bring our exposure in it up to a neutral weight. We have increased the notional purchases in Seplat, and our exposure is now in line with the index. We expect some volatility in global oil prices over the coming month reflective of Russia’s supply cut from March 1. We will press on with these changes this week and review them next week.