June 8, 2023/Fitch Ratings

The withdrawal of Nigeria’s fuel subsidy and President Bola Tinubu’s pledge to move towards a unified exchange rate are positive developments for Nigeria’s credit profile, says Fitch Rating. However, the reform agenda continues to face execution risks, and still lacks detail, including measures that might start to address other challenges to Nigeria’s credit profile, such as structurally very low non-oil budget revenue.

Our expectation that President Tinubu’s government would be somewhat more reformist and market-friendly than that of the former President Muhammadu Buhari, with progress on subsidy and exchange-rate reform, was an important factor in our affirmation in May 2023 of Nigeria’s rating at ‘B-’ with a Stable Outlook. The withdrawal of the petroleum subsidy, which cost more than 2% of GDP last year, has been quicker than we had assumed, and provides assurance over the administration’s commitment to reform.

It is unclear whether current fuel prices reflect full subsidy withdrawal, in particular whether the Nigerian National Petroleum Corporation is still benefitting from a preferential exchange rate. The risk of backtracking also remains, particularly if public opposition increases, although we believe it is fairly low – given the political capital the president has invested in the fuel subsidy’s removal. The government is planning substantial new transfers to help cushion the social impact, but we still expect the net effect of the reform to support fiscal consolidation.

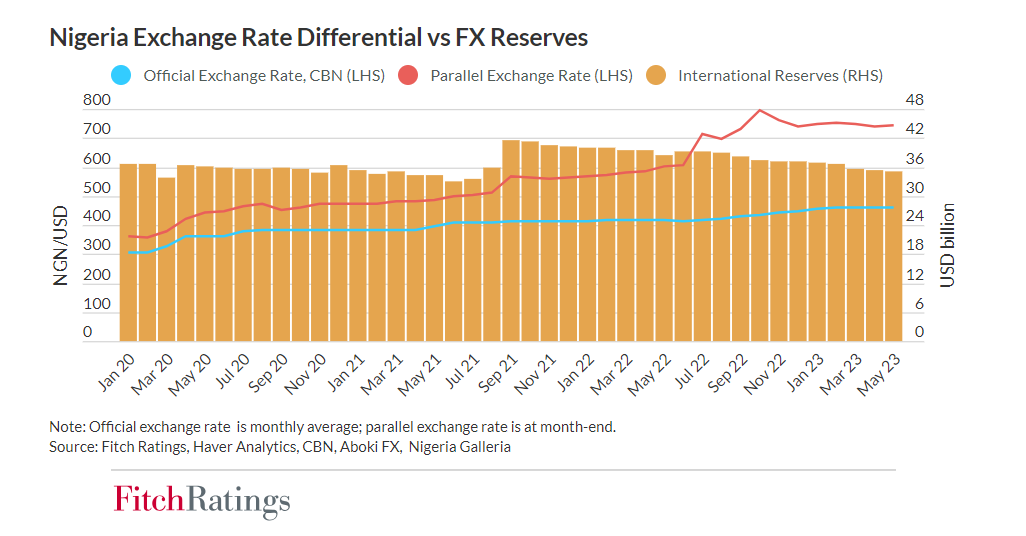

Fitch views Nigeria’s extensive use of foreign-exchange (FX) controls and import restrictions as a key credit weakness. The policies deter foreign investment and cause foreign-currency shortages for the private sector. The president has called for the Central Bank of Nigeria (CBN) to work towards a unified exchange rate, and we believe unification of the multiple official FX windows is likely but timing is uncertain, as is the scale of the depreciation of the official exchange rate that the CBN will allow. Fitch anticipates a phased exchange-rate liberalisation, moving the official rate closer to a market-clearing level.

This partly reflects our view that the CBN’s FX controls are largely aimed at managing external pressures. International reserves fell by USD3.4 billion in the year to end-May, to USD35.1 billion. We project a fall to 4.0 months of current external payments by end-2024, from 4.9 at end-2022. This is still above the projected median of 3.3 months for ‘B’ category sovereigns. However, Fitch estimates around 30% of Nigeria’s reserves are made up of FX swaps, which lowers overall quality.

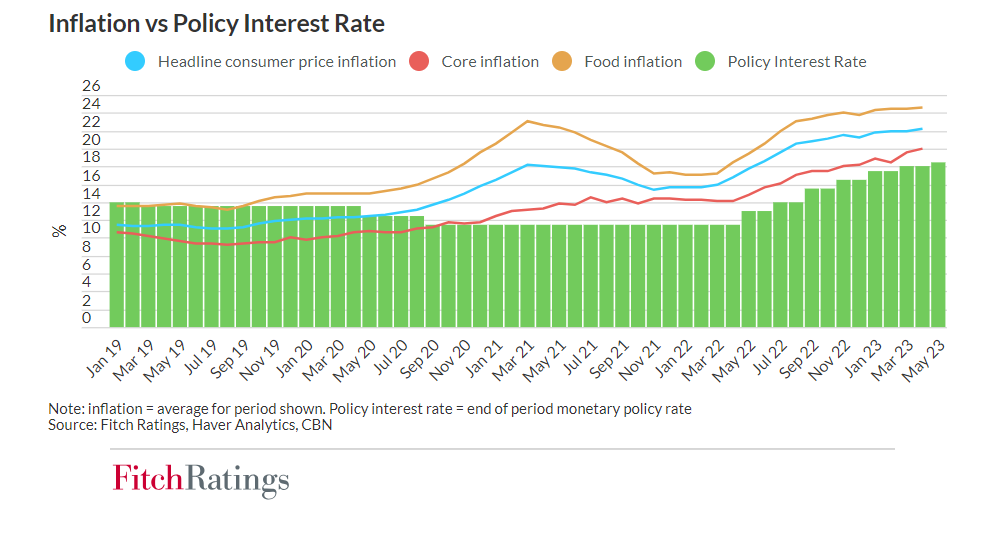

Sequencing challenges associated with the fuel subsidy’s removal also contribute to our baseline expectation for phased exchange-rate reform, partly as both reforms would add to upward pressure on consumer price inflation, which averaged a high 22% in 1-4M23.

The president stated in his inaugural address that interest rates need to fall, but the policy rate – at 18.5% – is already negative in real terms. Fitch believes the CBN’s fiscal financing is a greater contributor than interest rates to monetary policy settings that are loose. We anticipate additional central bank financing in 2H23, albeit at a lower level than over the last year. This is consistent with the recent increase in the formal limit on use of the government Ways and Means overdraft with CBN to 15% of the previous year’s fiscal revenue, from 5% – a cap that has not been followed.

The approval of measures to securitise NGN23 trillion (around 11% of GDP) of the overdraft with CBN at a lower interest rate, of 9%, will help contain debt-servicing pressures. Nigeria’s general government interest/revenue, at 42%, is among the highest of Fitch-rated sovereigns due to extremely low levels of revenue mobilisation and represents a risk to fiscal sustainability.