August 8, 2023/Coronation Research

What lessons can we draw from commodity markets this year? Global equity markets have been hot (particularly in the US), but commodity markets have been cold, with key soft commodities like wheat, maize, palm oil and rubber trending down. Oil has recovered in recent weeks, but US dollar inflation means that Nigeria’s oil earnings are no longer what they once were. It is folly to rely on crude oil revenues.

The Lesson of Weak Commodities

The first seven months of 2023 have seen strong rallies in global equity markets and in the NGX All-Share Index. Investment conditions have been favourable, even if consensus forecasts for global growth are regularly toned down. What has been remarkable, in our view, is the weakness of commodities.

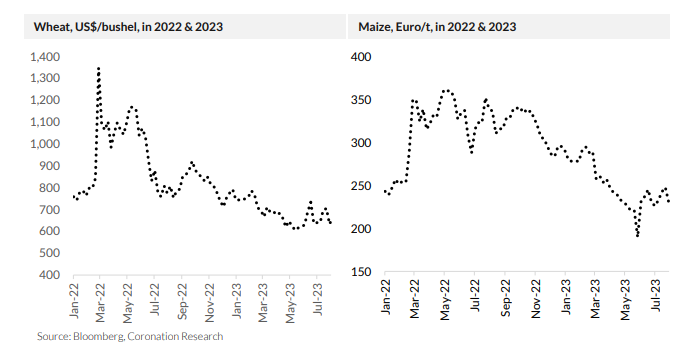

Commodity markets are clearly not looking forward to a bright future in the same way that equity markets are. Starting with the staples of the soft commodity market, wheat and maize, these are having a dull year in 2023, with prices trending down.

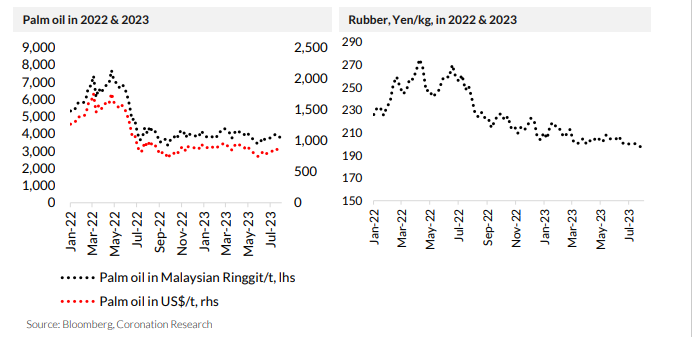

These are beneficial movements for Nigeria, which is an importer of wheat and which imports many items whose base lies in maize. However, the weakness of the soft commodity complex extends to palm oil and rubber, which is unfortunate because Nigeria is a producer of both.

To a degree, Naira depreciation against the US dollar helps Nigerian producers of palm oil and rubber, though this depends whether they are actually exporting their products (in which case the amount of money they receive increases in proportion to the change in the official exchange rate quoted in the I&E Window) or whether they merely substitute products otherwise imported (for which the parallel market rate was, in all likelihood, already setting the price).

There are some exceptions to this bleak picture, though not many. The international price of cocoa is up 41% year-to-date, for example.

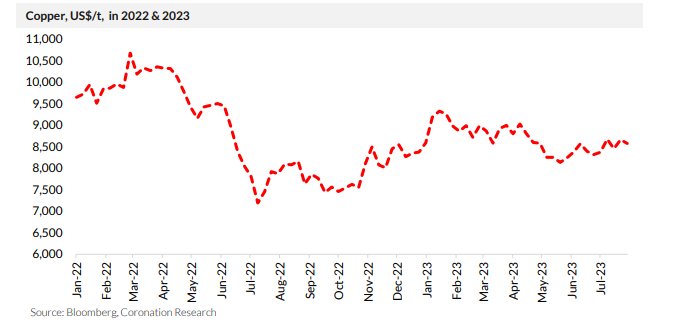

For a measure of how global commodity markets view global growth prospects, we look across to the copper price, and we find copper has been more-or-less flat all year. The much-discussed stimulus package to reinvigorate Chinse growth does not seem to be having much effect here

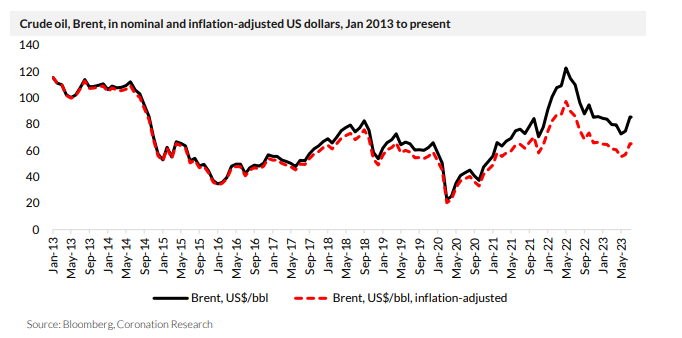

For Nigeria, of course, the most important commodity is crude oil. And oil prices are only slightly down this year, at least in nominal terms. But should we actually think in nominal terms? After all, oil is priced in US dollars and US dollar inflation has been quite high, reaching at much as 9.1% year-on-year in June 2022 (since when it has trended down). Granted, we have been thinking of all other commodities in terms of their US dollar nominal prices in this article but given oil’s peculiar importance to Nigeria perhaps we need to think of its inflation-adjusted price as well.

Adjusting the price of oil for US dollar inflation means that, even though we may think of the price of Brent being US$86.24/bbl, this is not the whole picture. If we re-base for US dollar inflation, starting in January 2013, then today’s Brent price is an inflation-adjusted US$65.20/bbl, 24% lower than the nominal price.

The difference between the nominal and US dollarinflation-adjusted oil price starts to make a meaningful difference over the past two years (when US inflation picked up). So the price of Brent crude year-to-date is some 22% lower, inflation-adjusted, than the inflation-adjusted average for 2022. That makes a big difference when it comes to the purchasing power of Nigeria’s petro-dollars.

In conclusion, 2023 so far has been a year of remarkably dull, if not weak, global commodities. It has benefits (lower import bills for some foodstuffs) and drawbacks. Perhaps the biggest lesson is not to rely on earnings from commodities, crude oil in particular.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) gained 4.40% to close at N743.07/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) slipped by 0.04% to US$33.97bn.

Though for the time being it appears that there is a sizable backlog of demand for US dollars to be processed, in the medium term we think that the reforms in the foreign currency market will lead to improvements in FX liquidity.

Bonds & T-bills

Last week, the secondary market for T-bills was bullish with average yields retracting by 15bps to 6.96% pa. Average yields along the T-bill curve declined: at the short end (26bps to 4.09%); mid-end (1bp to 5.91%); and long end (17bps to 8.39%).

On the other hand, the secondary market for FGN bonds was bearish, the average yield increased by 18bps to 13.31%. Average yields along the FGN bond yield curve rose: at the short end (22bps to 11.23%); mid-end (22bps to 13.45%); and long end (10bps to 14.73%).

We continue to wait for the new administration to announce an overall strategy on market interest rates.

Oil

Last week, the price of Brent closed on a positive note, advancing by 1.47% to settle at US$86.24/bbl. Brent is down 0.38% year-to-date and is trading at an average of US$80.13/bbl year-to-date, 19.14% lower than the average of US$99.09/bbl in 2022.

After major producers Saudi Arabia and Russia extended output curbs through to the end of September, adding to fears over undersupply, oil prices increased by more than a dollar a barrel on Friday to mark a sixth straight week of gains.

US West Texas Intermediate crude increased $1.27/bbl, or 1.6%, to close at $82.82/bbl, while Brent crude futures increased $1.10/bbl, or 1.3%, to close at $86.24/bbl on Friday. At that point both benchmarks reached their highestlevels since the middle of April.

We maintain our view that, for most of the year, prices are likely to remain above the US$75.00/bbl mark set in Nigeria’s government budget though, as we note on Page 4, the purchasing power of those US dollars has slipped meaningfully over the past two years.

Equities

Last week, the NGX All-Share Index closed higher, increasing by 0.22% to settle at 65,198.98 points. Its year-to-date return rose to 27.21%. Dangote Sugar (+25.00%), Nigerian Breweries (+16.44%), and Cadbury Nigeria (+12.05%) closed positive while Guinness Nigeria (-17.42%), Ecobank Transnational Inc (-7.94%), and Stanbic IBTC Holdings (-6.47%) closed negative. Performances across the NGX sub-indices were mostly positive as the NGX Insurance (+5.88%) index topped the list, followed by NGX Consumer Goods (+2.27%), NGX Pension (+0.43%) and NGX Industrial Goods (+0.23%) indices closing green. On the other hand, the NGX Banking (-2.13%), and NGX Oil/Gas (-0.68%) indices closed in the red. We remain optimistic about this market following the key fuel subsidy and foreign exchange reforms.

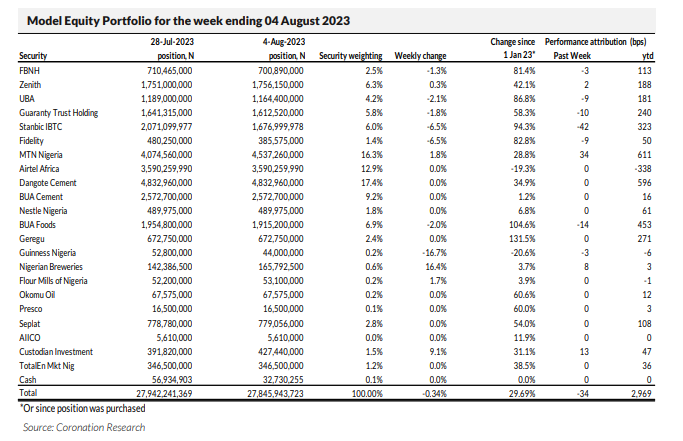

Model Equity Portfolio

Last week the Model Equity Portfolio fell by 0.34% compared with a rise in the NGX All-Share Index of 0.22%, underperforming it by 56bps. Year-to-date it has risen by 29.69% compared with a rise of 27.21% in the NGX All-Share Index, outperforming it by 247bps.

Note that two weeks ago the Model Equity Portfolio had risen by 0.70% when the NGX All-Share Index had risen by 0.08%, outperforming it by 62bps. That was due to the performance of two stocks, Stanbic IBTC and Fidelity Bank. Last week they both corrected, and we lost the outperformance we had earlier gained. Meanwhile, our notional position in Custodian Insurance earned a useful 13bps last week.

Note, too, that the equity market is substantially interested in trading banks at the moment. Some of the heaviest weights in the NGX All-Share Index (notably Airtel Africa, Dangote Cement and BUA Cement) did not experience much stock turnover last week and their prices did not change. By contrast, turnover in the banks was high, and having hit lows mid-week, some bank stocks (e.g. FBNH, Zenith Bank, UBA and GTCO) rallied on Thursday and Friday.

As explained last week, we remain committed to an overweight in banks (a near-double overweight) as this is based on our fundamental view that they are beneficiaries from currency liberalisation and the return of liquidity to the banking sector at the instigation of the CBN, as we explained in Coronation Research, Investment Opportunities from FX Liberalisation, 11 July. At the same time, we are becoming concerned with the lack of an overall policy direction with regards to market interest rates. And we understand that the relaxation in the cash reserve requirement (CRR) is, to a degree, linked to banks fulfilling their obligations to the loan-to-deposit ratio (LDR) requirement. We may need to assess again how free the banks are to act in their own best interests and will report back.